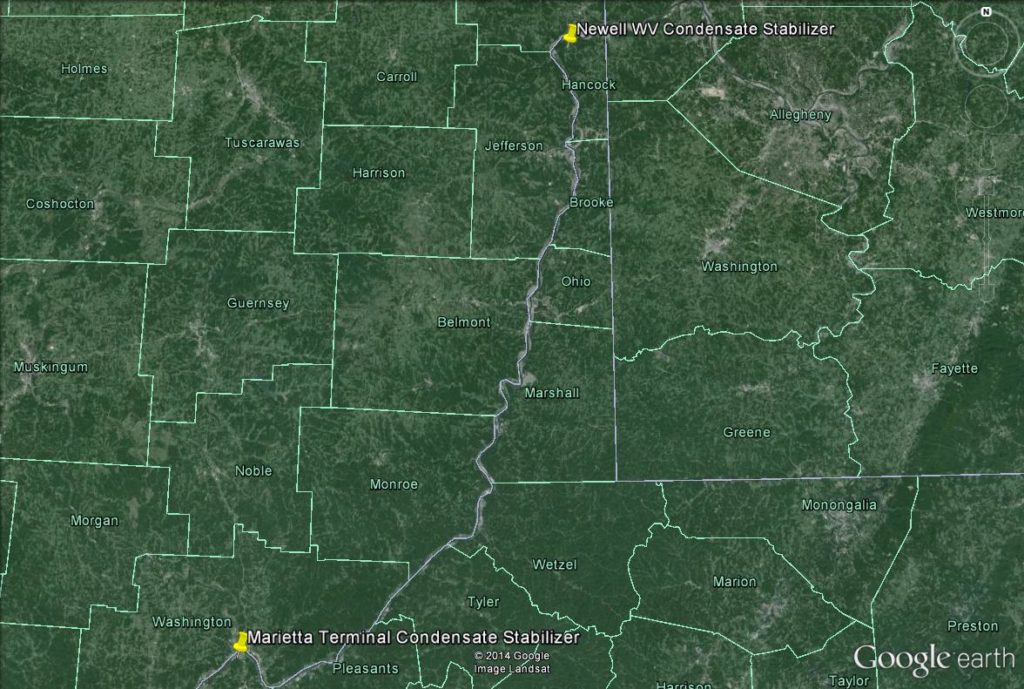

Ergon, Inc announced plans yesterday to develop 10,000 B/d of condensate stabilization at its Marietta, OH river terminal with operations beginning in 4Q2014. In addition to the Marietta terminal, Ergon intends to add another 10,000 B/d of stabilization capacity in Newell, WV in 2015.

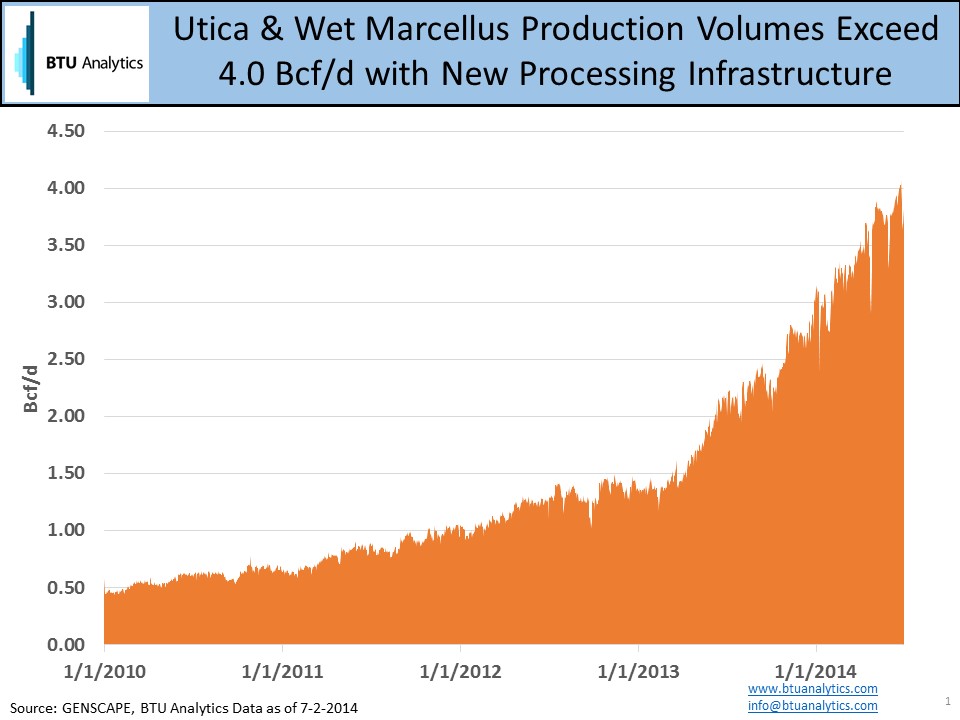

These two facilities straddle the prolific developments in the Wet Marcellus & Utica where natural gas production has ramped up to over 4 Bcf/d according to the latest pipeline flow data from Genscape.

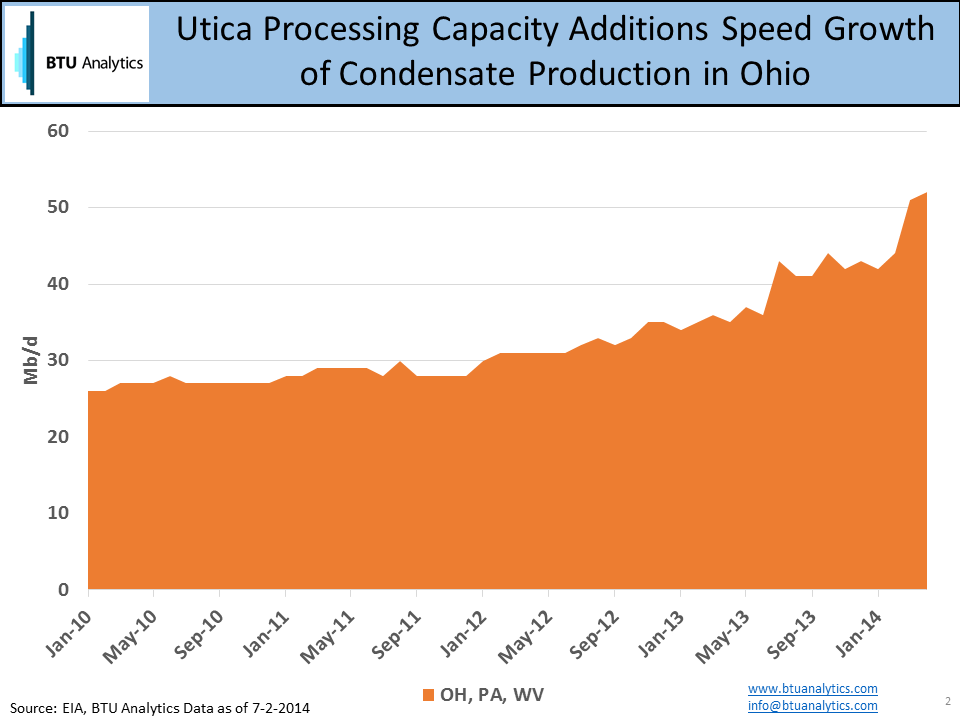

The rapid ramp up in natural gas production over the last several months has also sent natural gas liquids & condensate production soaring higher. The latest statistics from the EIA show that OH, WV, & PA oil & condensate production has increased from 27 Mb/d in Jan. 2010 to over 50 Mb/d in April 2014.

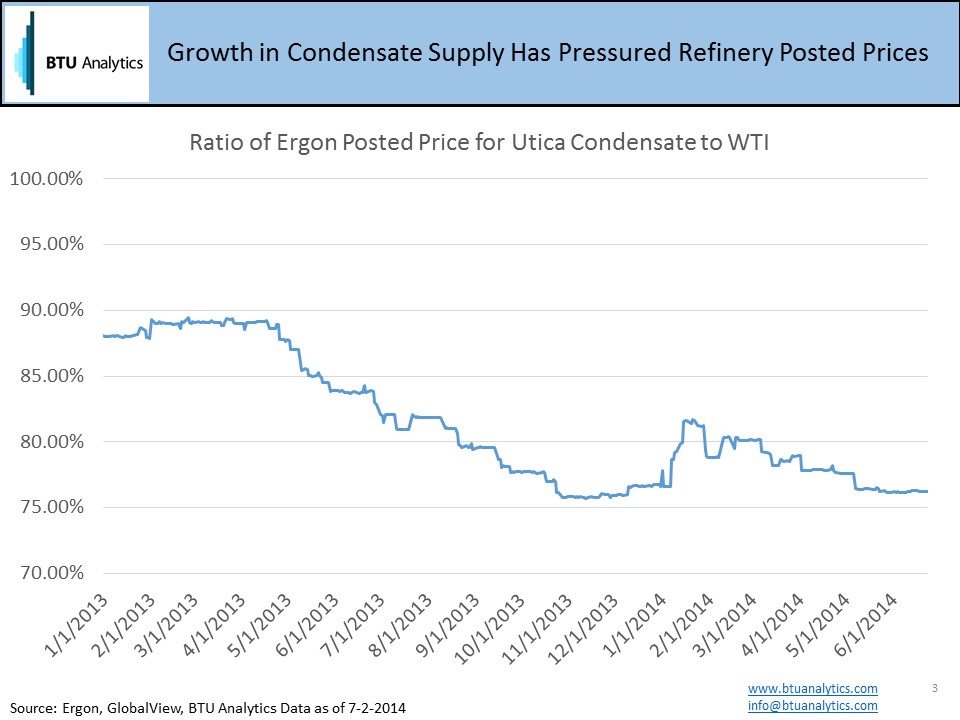

The growth in supply of Utica condensate (60+ API) has pressured the prices refineries in the area are willing to pay for condensate. Ergon, also, has existing refining assets in the area and provides prices that it is willing to pay for Marcellus & Utica Condensate with an API of 60 or more. As a percentage of WTI, the posted price for Marcellus/Utica Condensate has fallen from 90% of WTI in 2013 to nearly 75% of WTI in June of 2014.

This represents a $16/barrel increase in the differential for Utica condensate producers. Could the loosening of the crude export ban provide a floor for stabilized Utica condensate pricing or will growth in the US continue to outpace infrastructure construction?