With so much bad news in the energy press these days – and I can go on about CFOs ‘leaving for personal reasons’, debt redeterminations, equity dilutions, stock exchange delistings, forced asset sales and lay-offs – it is refreshing to see some areas of the energy complex continue plugging along, such is the case in the SCOOP and STACK plays in Oklahoma.

Low commodity prices be damned, in 2015 there has been a stream of infrastructure development announcements for oil and gas, including this week as Velocity Midstream plans to build an oil gathering project in the SCOOP and STACK connecting to CVR’s refineries in Oklahoma and Kansas. The pipe will allow producers to segregate different grades of crude being produced across the area. This follows Southern Star’s and NextEra’s August announcement of the 1.2 Bcf/d Sooner Trails pipeline to Bennington, OK, and Tall Oak Midstream announced it would expand their gas processing plant in the STACK by 200 MMcf/d. In addition, in September, ARM Midstream proposed gas and crude gathering systems in the STACK as well.

The question is, if we look at recent state well level production data, EIA 914 estimates and producer investor decks, do we see a sharp uptick in producer results in 2015 over 2014 to support all of this development?

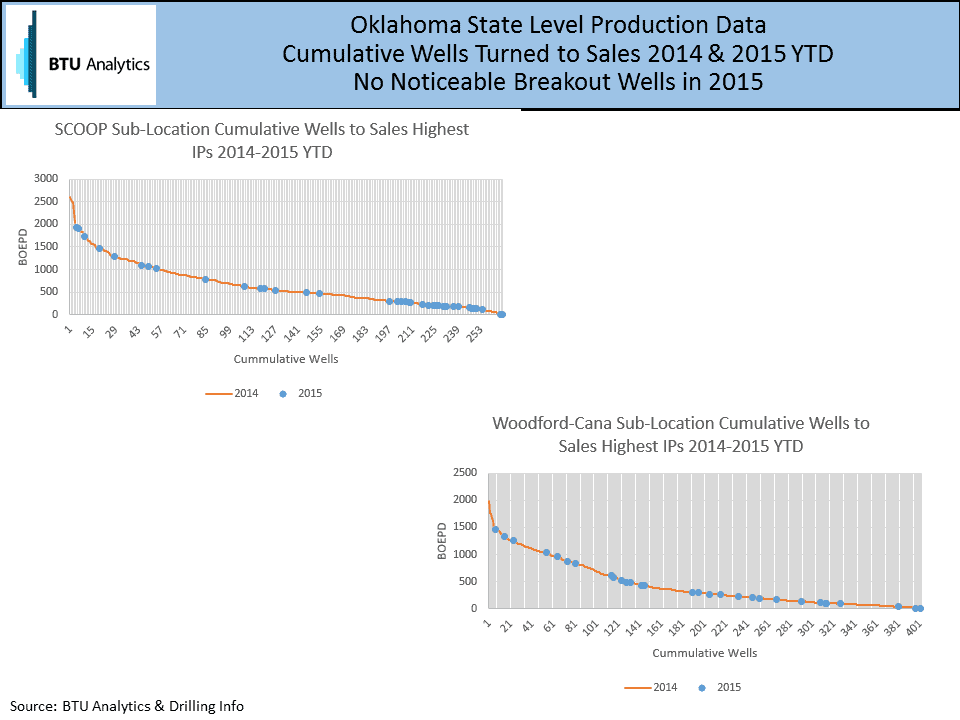

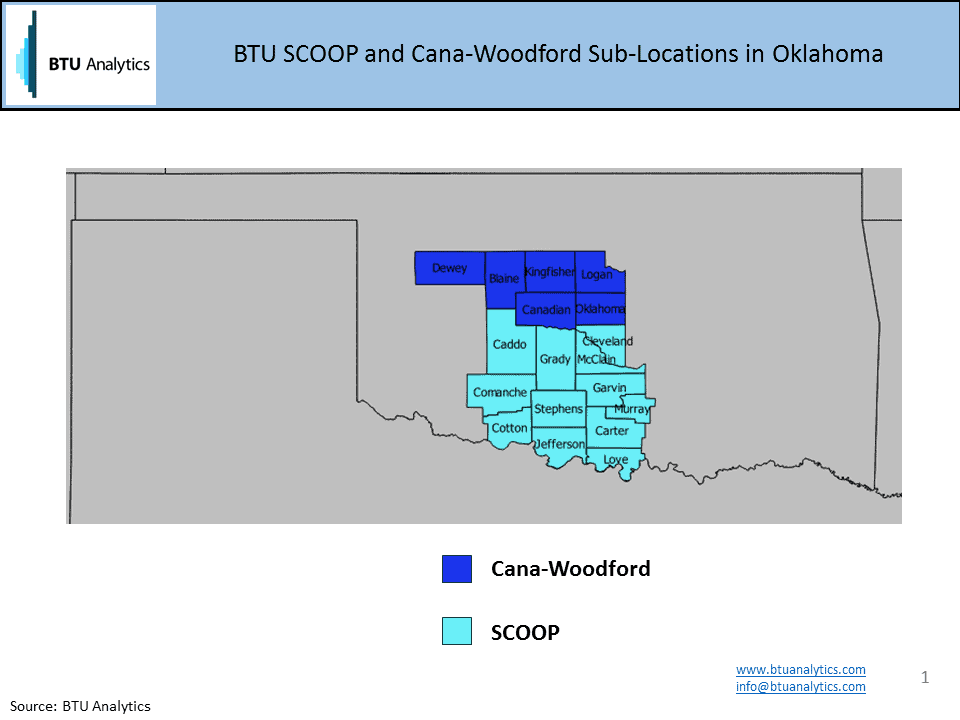

First, the following is how BTU Analytics looks at production in the areas of the SCOOP and STACK. BTU uses aggregated counties to designate sub-locations and in this case, we call the SCOOP area SCOOP and the STACK is labeled Cana-Woodford. As a result, different production horizons within sub-locations are commingled.

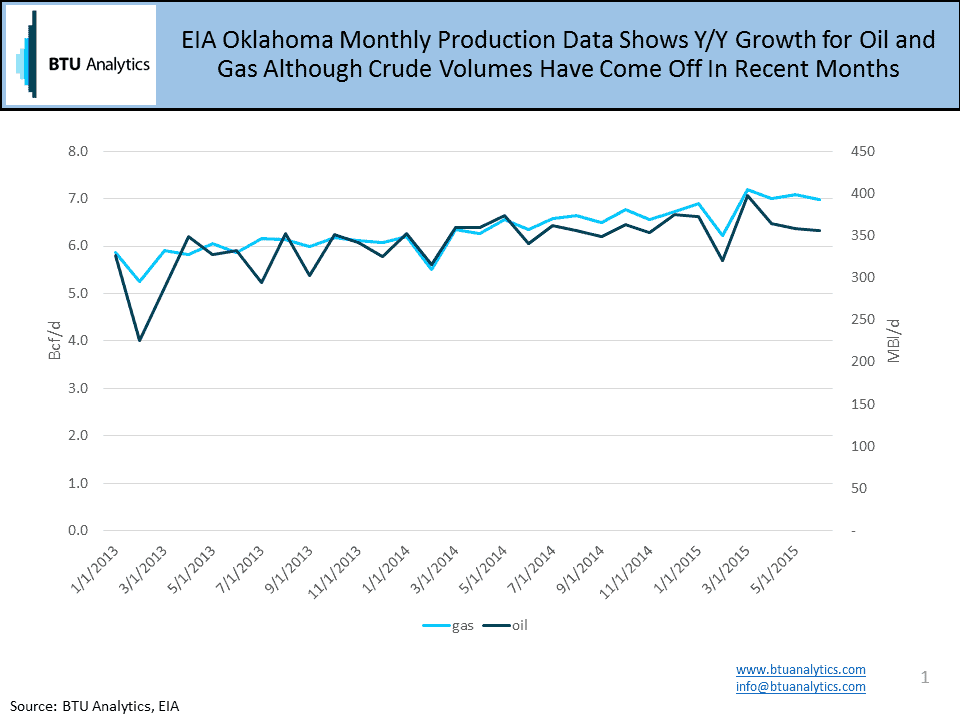

EIA 914 monthly Oklahoma production data shows year over year growth in both oil and gas although production has fallen off more recently.

If we look at lagged state level production data we see no exceptional breakouts in well performance when comparing 2014 vs. 2015 YTD results (through March) although note generally the SCOOP sub-location is on average showing higher initial production rates on a BOE basis than the STACK area (the Cana-Woodford sub-location). Several producers that specialize in these two plays show wells in their investor decks that are at the top range but do not exceed 2014 levels.

According to BTU Analytics’ Upstream Outlook, gross gas production is expected to grow 37 MMcf/d to 1.2 Bcf/d in the STACK (the Cana-Woodford sub-location) and grow 676 MMcf/d to 1.6 Bcf/d in the SCOOP sub-location by 2020. Our oil forecast calls for the STACK area, as measured by the Cana-Woodford sub-location, to grow by 2,700 Bl/d to 42,000 Bl/d and for SCOOP to grow by 9,900 Bl/d to 89,000 Bl/d by 2020.

While current lagged data does not suggest a breakout in the SCOOP and the STACK, the recent pace of infrastructure development suggest some strong results are yet to come from these plays. Track SCOOP and STACK wells to sales, production and infrastructure development in the BTU Analytics’ Upstream Outlook.