When it rains, it pours, and in Pennsylvania, it is pouring. The Northeast has been under consistent pressure with weak natural gas prices and if that wasn’t enough, most recently, Tallgrass announced that REX’s Zone 3 East-to-West Project would not make its previously announced ISD of June. To prove the above saying true, legislatures in both Pennsylvania and Ohio, are considering an increase or implementation of a severance tax, a tax levied when resources are “severed” from the ground. The industry is out in full force airing television ads and making robo-calls to residents, arguing the case that any new tax will hurt their respective economies. Ignoring the political hyperbole on both sides, what will be the real impact of a severance tax on northeast well economics?

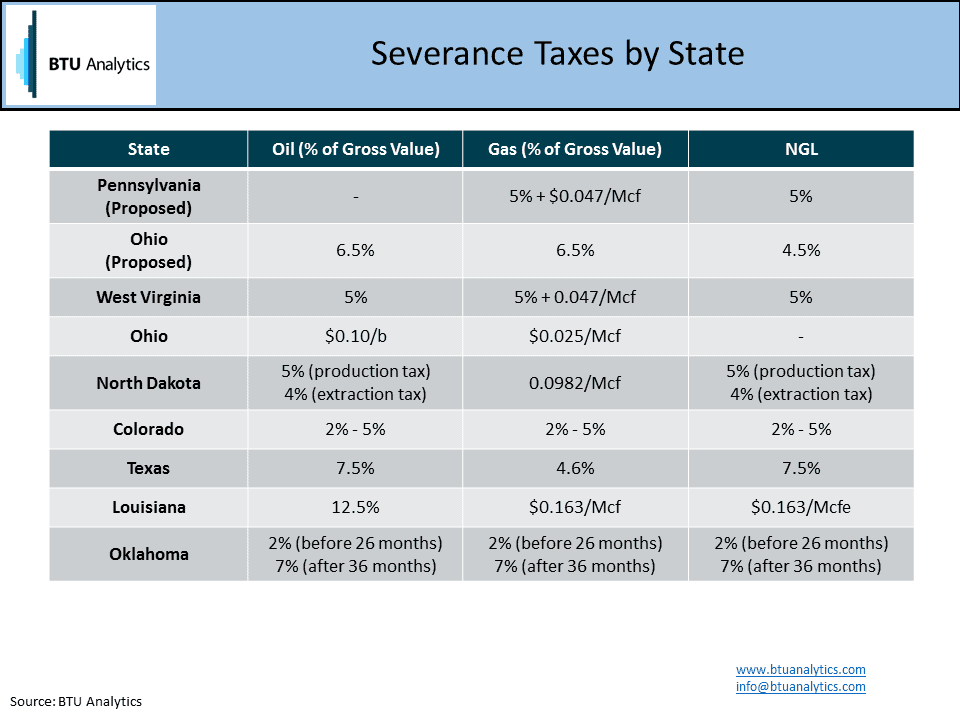

Currently, Ohio has severance taxes of $0.10/Bbl of oil and $0.025/Mcf, while Pennsylvania does not have a severance tax, instead they have what they call an impact tax, which amounts to a flat fee imposed on every well drilled regardless of its production. Pennsylvania Governor Tom Wolf has proposed a severance tax of 5% of natural gas and NGL revenue plus a flat rate of $0.047/Mcf produced with a floor for natural gas price at $2.97, which means even if prices fall below $2.97 the taxes would be calculated using $2.97 to calculate producer revenue. If enacted, Pennsylvania would join a long list of other states with severance taxes, a selection of which is shown below.

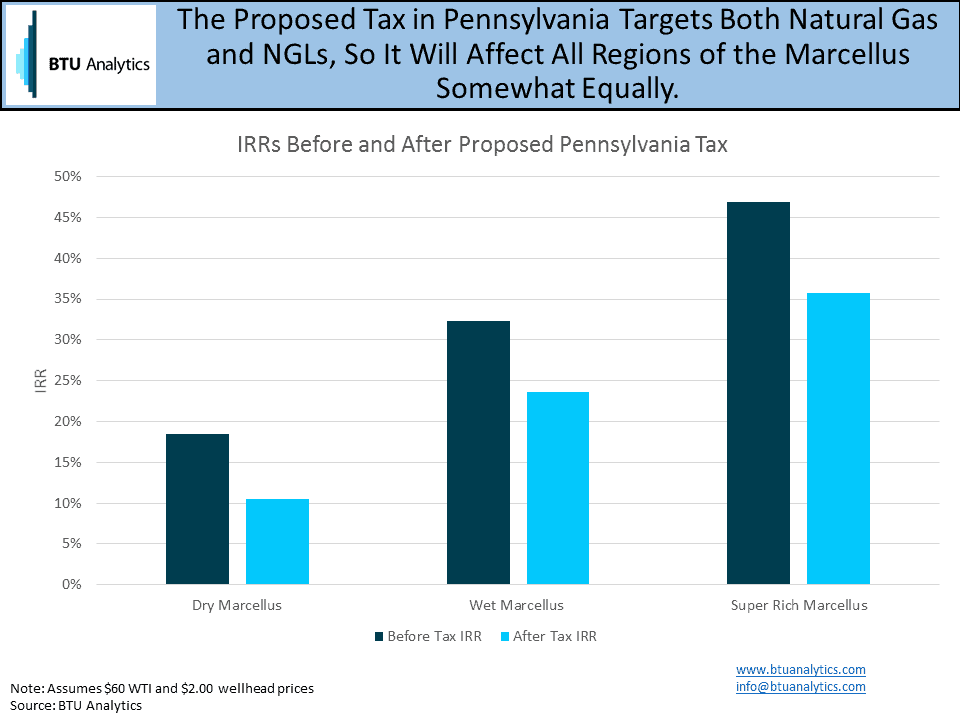

While there are a few severance tax proposals floating around in the PA legislature, let’s focus in on Gov. Wolf’s proposal in Pennsylvania, which mirrors West Virginia’s policy. The chart below shows the changes in return in the Marcellus before and after the proposed tax assuming $60 WTI and $2.00 wellhead prices. Year to date, Domion South prices have averaged $1.80/MMBTU, however, if producers hold firm transport out of the region, they will be able to push their realized higher. Since the proposed severance tax targets both natural gas and NGLs, economics fall pretty evenly throughout the different regions of the Marcellus, with drops in IRR between 8% to 11%.

Will this new tax spell the end for the Marcellus? Probably not, but it certainly doesn’t help the situation for producers. BTU Analytics expects Appalachian production to continue to grow, with gross gas production hitting an average of 31.6 Bcf/d and 33.0 Bcf/d in 2018 and 2019, respectively. This growth will be driven by a slew of expansion projects coming online that add takeaway capacity to the region.

With both Pennsylvania and Ohio expected to finalize their budgets this month, it will only be a matter of time until we find out how hard this downpour will fall.