As Rover pipeline is now largely complete, focus can shift to the progress of other greenfield projects out of Southwest Appalachia, with Mountain Valley Pipeline one of the next key greenfield projects officially slated to come online by the end of this year. If Rover has taught us anything, it’s that progress on these large pipeline projects can be materially impacted by unforeseen construction and regulatory challenges, providing continued risk to the startup date; the project is not done until it’s done.

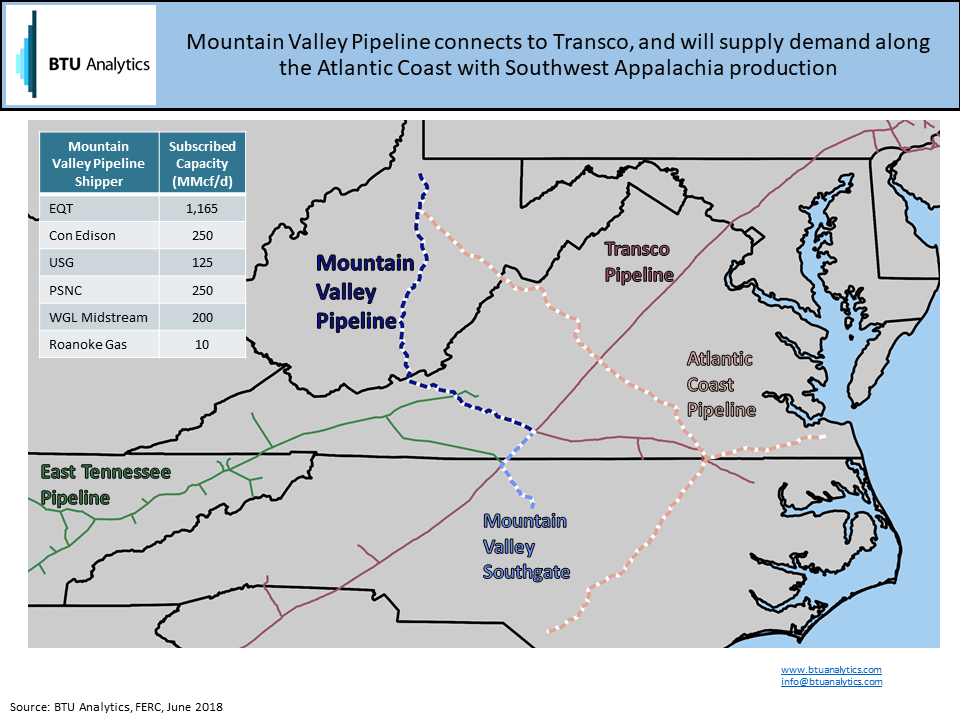

Mountain Valley is one of two major greenfield pipelines that will transport gas produced in Southwest Appalachia to the Atlantic Seaboard, as seen in the map below. The other project, Atlantic Coast Pipeline, is due to come online at the end of 2019. In Northeast Appalachia, Atlantic Sunrise is nearing completion and expected to be operational in the next few months. The Atlantic Seaboard is a region undergoing transformation, with demand for natural gas growing, and traditional supply from Gulf Coast on Transco being displaced by production from Appalachia.

The 2 Bcf/d of capacity on Mountain Valley is fully subscribed, with about half of the capacity from EQT at over 1.1 Bcf/d, and the rest by utilities, including Con Edison, USG, WGL, and Roanoke Gas. The pipeline is thus functioning as both a ‘supply push’ as well as a ‘demand pull’ project, versus Atlantic Coast Pipeline which is entirely subscribed to by utilities. Mountain Valley also recently announced the Southgate extension into North Carolina, set to become operational in 2020, which is backed by the LDC PSNC Energy, and further capitalizes on the ‘demand pull’ into the region.

While construction on Mountain Valley is progressing, risk remains to meet an end of 2018 startup. Mountain Valley is facing continuous and open challenges from environmental protestors, including people sitting in trees and chaining themselves to equipment to halt construction. These efforts have not been successful to date, though this does provide a layer of difficulty for the project. On the regulatory side, there has recently been a small hiccup with the water permit in West Virginia: the Army Corps of Engineers in May halted work on the Mountain Valley Pipeline in 10 West Virginia counties until it can determine whether its permit allowing work there is in compliance with West Virginia environmental rules. This is for a small section of the pipe, so it is not anticipated to provide material delays to the schedule at this point. Meeting an end of 2018 in-service date is achievable for the project, though essentially requires things to go relatively smoothly during construction throughout the rest of the year.

Given uncertainty to the in-service date, what are the implications to production and pricing if the project meets its target in-service date at the end of this year? What if there is an unforeseen setback (as we saw multiple times on Rover), and the full startup is delayed until the middle of next year?

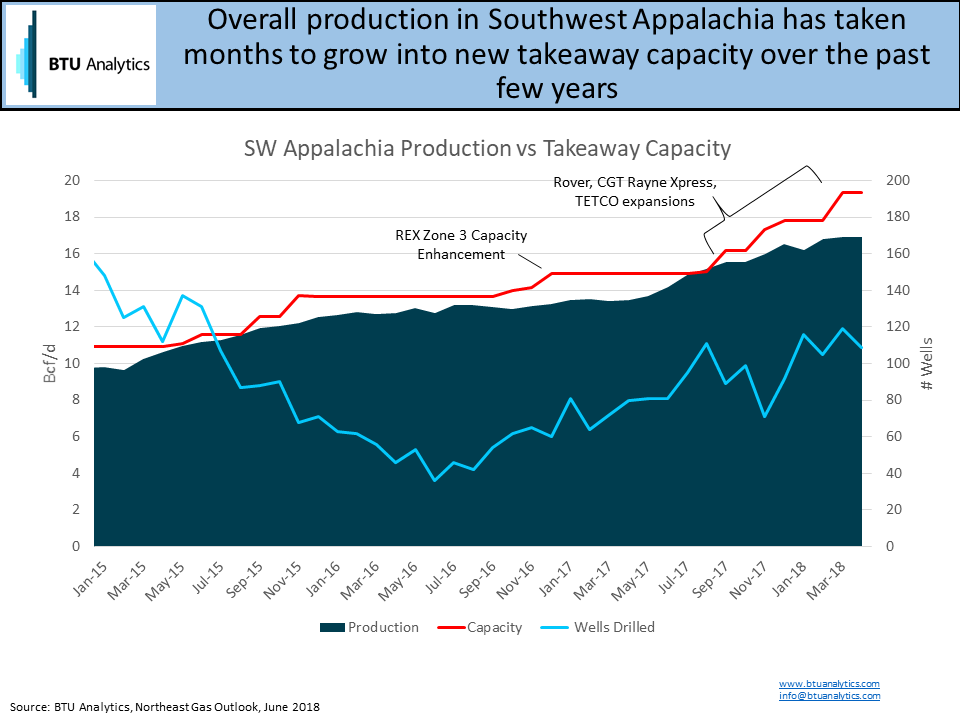

On the production side of things, we do not anticipate production in Southwest Appalachia to immediately rise to the level of new takeaway capacity, and instead anticipate gradual growth over the next 18 months, after which we expect the US to become demand constrained. Beyond Mountain Valley Pipeline, an additional 2.4 Bcf/d of takeaway capacity from Southwest Appalachia is slated to come online at the end of this year, from the TCO Mountaineer/CGT Gulf Xpress and Nexus projects. Looking back over the past few years, as new projects have come online, production has not immediately increased to the level of new takeaway, instead growing more gradually over several months, as seen in the figure below. There has been a gradual increase in the number of wells drilled since the beginning of the year. With an average spud-to-sales time of about 8 months, and without a backlog of DUCS to draw upon, current drilling activity will largely set production for the end of the year. Unless there is a significant increase in drilling activity in the region in the coming months, we don’t expect material change to our production outlook over the next year, regardless of if Mountain Valley comes online in late 2018 or in mid-2019.

However, the timing of Mountain Valley will likely impact basis pricing in the region. The project provides an outlet to a premium demand market on the Atlantic Seaboard, represented by Transco Zone 5 pricing. Transco Zone 5 is a premium to MichCon pricing in the Midwest, meaning when Mountain Valley becomes operational, flows will likely preferentially head to the Atlantic Seaboard that would have otherwise gone to the Midwest market.

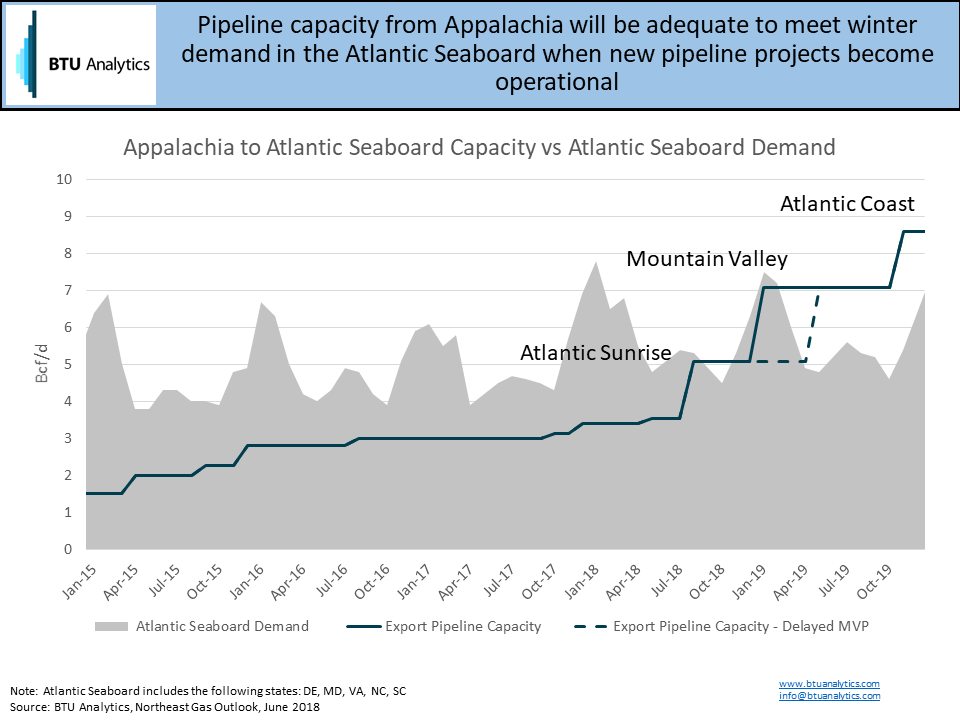

We also expect upward pressure on Dominion South basis when Mountain Valley comes online, particularly since we are anticipating more gradual production growth in the region through 2019. Further, whether it comes online this winter versus next summer has implications for seasonal pricing. Demand along the Atlantic Seaboard of course peaks in the winter, as shown below. With the completion of both Atlantic Sunrise and Mountain Valley, there will be enough capacity out of Appalachia to supply nearly all the Atlantic Seaboard demand in the winter. If Mountain Valley is able to come online this winter, this will strengthen Dominion South basis. However, if startup slips into spring or summer of next year, that could mute Dominion South basis pricing impacts this winter.

The specific timing of when Mountain Valley and other major pipeline projects become operational will impact the pricing dynamics in the region over the next 18 months. To keep up to date on how these projects are progressing as well as how our views on the region evolve, check out the latest edition of the Northeast Gas Outlook.