As we enter the first weeks of 2019, one topic to watch this year is the US LNG export facility build out. The momentum of the first wave of US LNG is a hot topic for January. But what about the second wave of US LNG projects (those which are expected to come online in 2022 and beyond)? What is the trajectory for build out of Wave 2 and when might these projects be online? Is it the regulatory approval process that determines when a project can make a final investment decision (FID) and start construction or is it volume of offtake agreements?

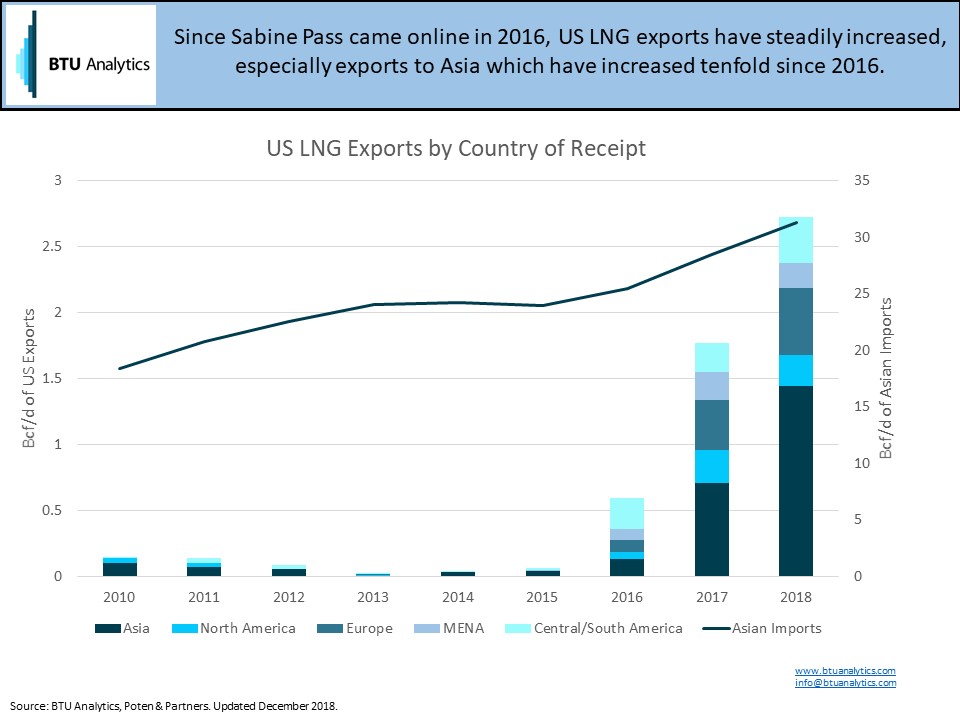

US exports of LNG have increased from less than 1 Bcf/d in 2016 to almost 3 Bcf/d in 2018. With Asian LNG demand expected to dominate the LNG market in coming years, many US LNG exporters are focusing on Asian customers for Wave 2 of LNG. In 2018, over half of total US LNG exports were to Asian countries; the next highest area of export was other North American countries, to which the US exported less than a fifth of total exports. The chart below shows the breakout of US LNG exports since 2010 by region of receipt, as well as total Asian imports since 2010. Asian imports from all countries have increased by over 10 Bcf/d since 2010. We can see from this chart why acquiring Asian customers is a focus for US LNG projects.

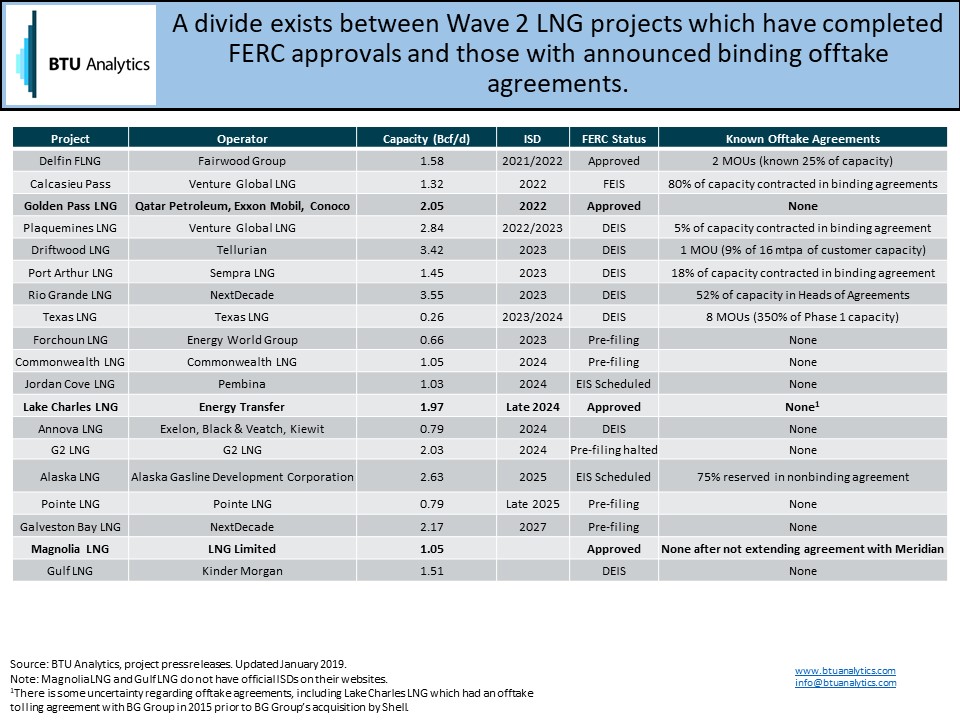

Here at BTU Analytics, we discuss Wave 2 LNG as the next round of LNG projects seeking to make FID in 2019, with operations expected to commence sometime between 2022 and 2025. The table below presents the most recently available regulatory and offtake agreement information for US Wave 2 LNG projects with an export capacity of greater than 1 million tons per year. This table includes information from operator press releases regarding offtake agreements for their LNG; we can see that the projects with full FERC approval (those in bold) do not have binding offtake agreements that have been announced publicly through press releases.

Backers have indicated that most of these projects expect to make FID in 2019, and based on operator timelines, it appears that operators will wait until full FERC approval is received before making FID. However, even Wave 2 projects that have been fully approved by FERC have not yet reached FID, indicating that it may not be FERC approval that is holding these projects back, but rather a lack of subscribed offtake capacity. Only three of the US Wave 2 projects listed have announced binding offtake agreements, none of which have full FERC approval. Conversely, none of the projects with full FERC approval have binding offtake agreements. It is important to clarify that many of the projects listed state that they anticipate making FID on fewer trains than the planned full capacity.

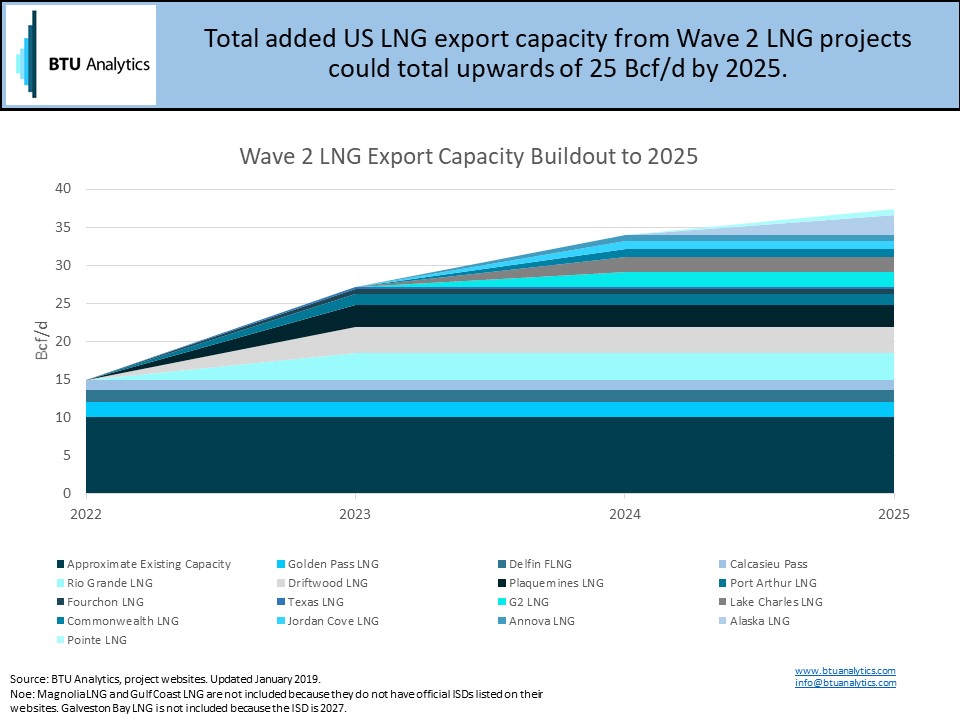

The juxtaposition between Wave 2 projects with full FERC approval and those with binding offtake agreements provides an excellent focus for what to watch in LNG in 2019: at what level of binding contracts will projects with FERC approval make FID, and how soon after FERC approval will projects with binding agreements make FID? The six projects that fall into either category will help inform predictions about the rest of Wave 2 LNG and how quickly the anticipated full capacity build out will occur. The chart below shows the capacity build out of selected US Wave 2 LNG projects through 2025, should all these projects be fully approved by FERC, make FID, and come online in accordance with their stated timelines.

If all the projects listed above can receive FERC approval, secure binding offtake agreements, and come online as anticipated, export capacity added would be upwards of 25 Bcf/d. A threefold increase in LNG export capacity from 2022 to 2025 is a tall order, and global demand remains a key driver in whether all Wave 2 projects will come to fruition. Keep up-to-date with BTU Analytics’ views of Wave 1 and Wave 2 LNG (and beyond) with the Henry Hub Outlook and the Long Term Gas Outlook.