Associated gas out of the Permian has been a popular topic and with natural gas pipelines filling up, it’s no surprise that the Waha differential to Henry Hub has widened in 2018. In fact, Waha basis to Henry Hub in April averaged about 72 cents weaker than the same period last year. But with eastbound pipelines to attractive Gulf Coast markets fully utilized, Permian gas is being forced into demand constrained markets like the Southwest and Midcontinent. Permian gas can also flow south to Mexico, but today we’ll focus on US markets. As we have previously touched on, these markets are typically supplied by the Rockies, Oklahoma, and Canada, creating heavy gas on gas competition west of the Mississippi. Let’s take a look at how extensive the influence of Permian associated gas is.

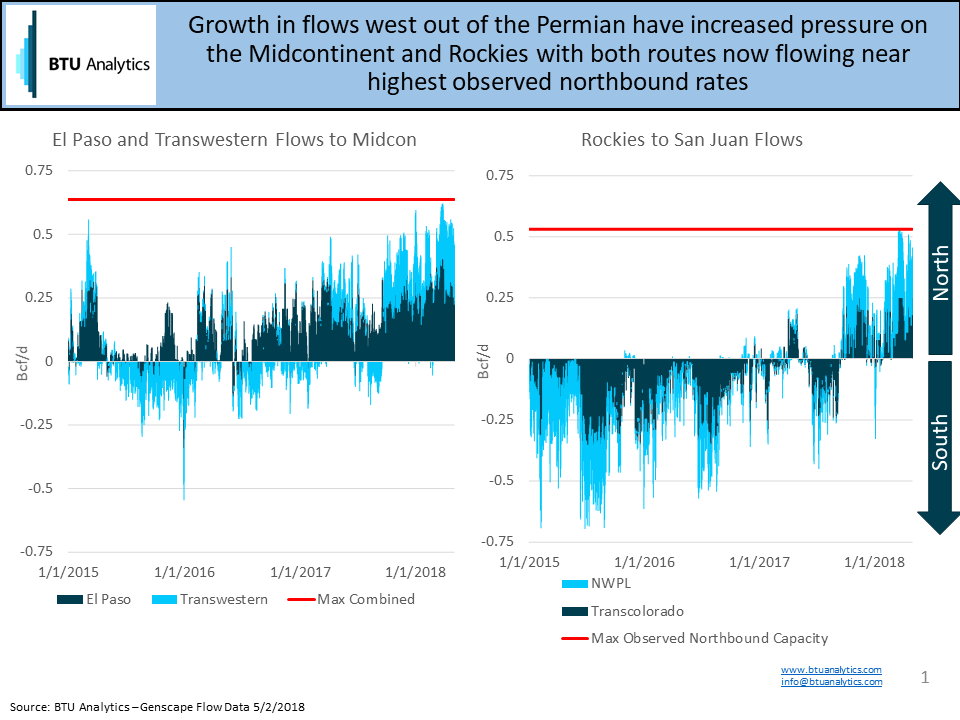

The pressure created by Permian associated gas can first be seen in the Rockies and Midcontinent, two regions directly adjacent to the Permian. The chart below shows the trend of growing northbound flows out of the Rockies (left) and Midcontinent (right). Permian gas is being increasingly pushed northbound on NNG and NGPL, as well as into the Midcon on El Paso and Transwestern, and has forced those regions to find new markets for their displaced gas.

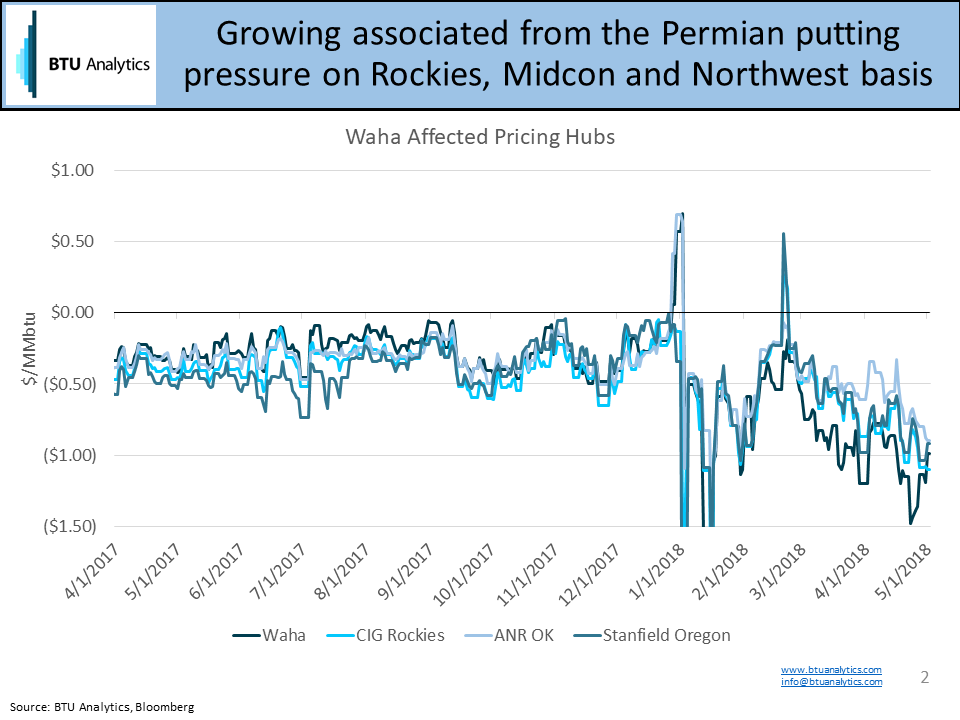

The influx of new gas in Middle America has shown up in pricing dynamics at various hubs across the Western US, as shown by the chart below. As Waha basis to Henry hub has weakened by 45 cents since the end of February, CIG and ANR Oklahoma have followed suit, with basis widening by 61 and 43 cents, respectively. With Rockies and Midcon pricing weakness driven directly by gas on gas competition out of the Permian, there is little respite in the demand constrained Pacific Northwest. Stanfield Oregon basis to Henry Hub has widened by 51 cents since the end of February, pressured not only by Permian gas pushing more Rockies gas into that market but also by continuing production from the Montney and Duvernay in Canada.

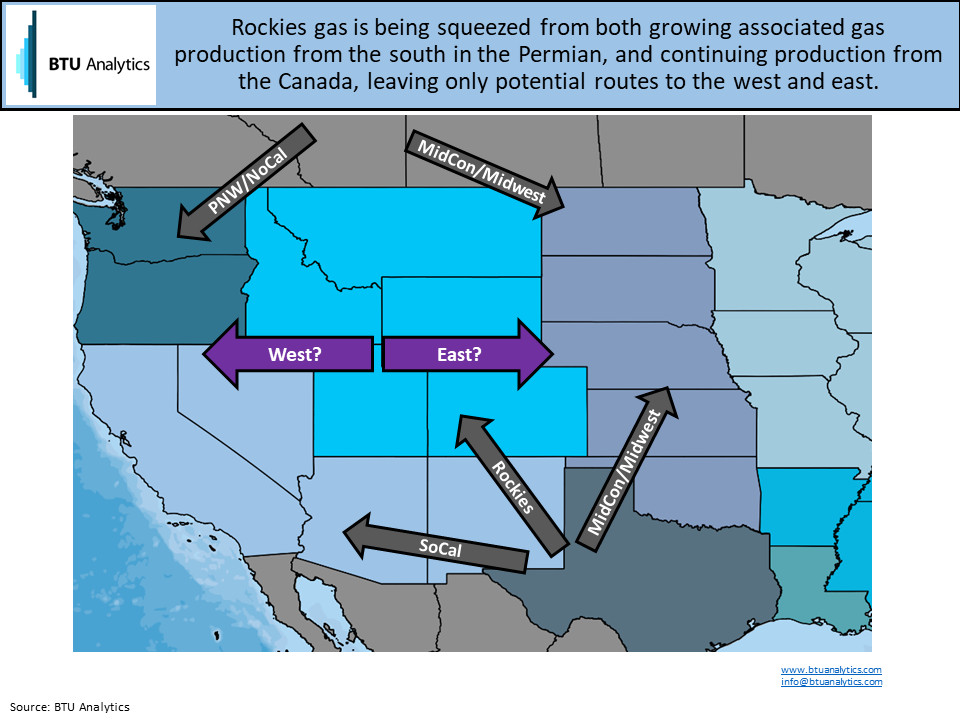

This leaves few options for Rockies gas to escape low pricing environments, as shown by the map below. Pressured both from the Permian to the south and Canada to the north, Rockies gas can only flow east or west. But with flows out of the Rockies on Kern full (combined with declining demand) and Ruby/NWPL pipelines headed to the similarly weak pricing environment in the Pacific Northwest, West Coast markets don’t look much better.

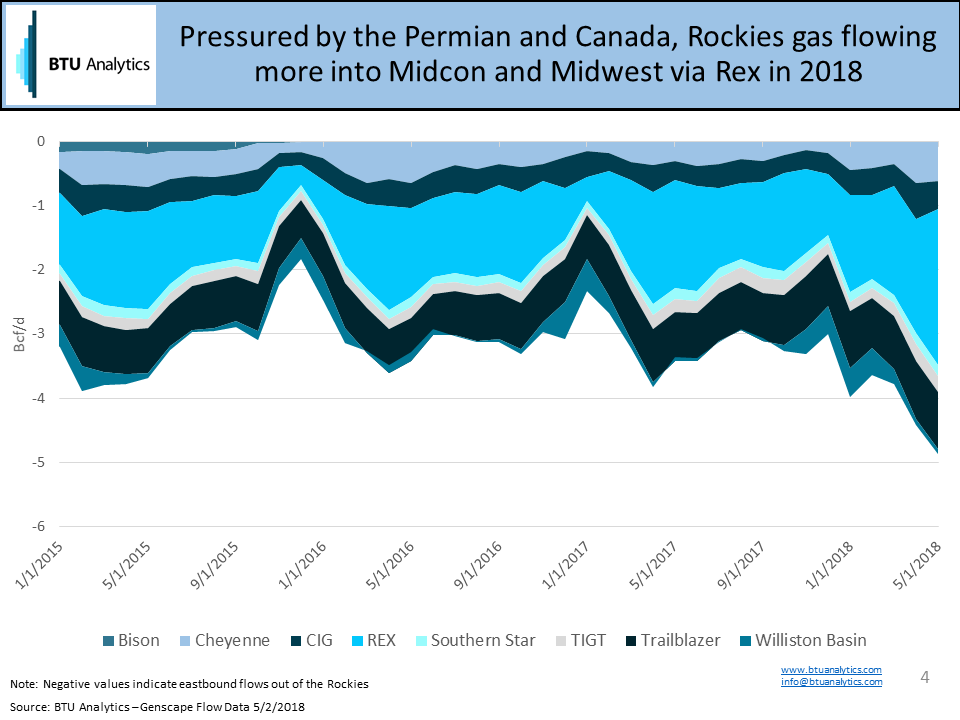

For this reason, Rockies flows east into the Midcon and further into the Midwest have increased in recent months. The chart below shows the flows out of the Rockies into the Midcon. Negative values indicate flows headed east. The increase in flows east out of the Rockies is driven mostly by growth on REX, which reaches even further into the Midwest, increasing competition in a market with little incremental demand growth compared to the amount of natural gas coming online.

Flows on REX are also filling up, though, which limits the extent to which it can serve as a release valve for gas in the Rockies and Midcon. How far east can the Permian’s sphere of influence reach, and when will eastbound capacity out of the region be alleviated? These questions and more are answered in our monthly Henry Hub Outlook.