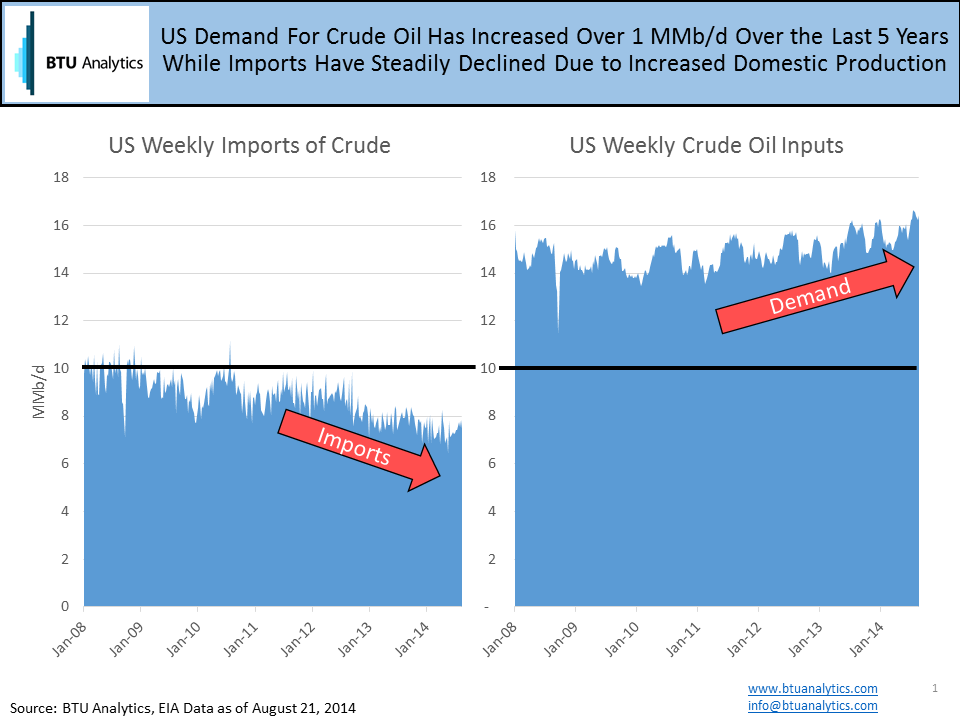

US imports of crude oil continue to set new record lows as producers across the US and Canada set new oil production highs. According to the latest EIA weekly statistics, crude oil imports averaged just 7.6 MMb/d over the last 4 weeks compared to 10.2 MMb/d for the same period in 2008 despite crude oil inputs to refineries increasing 1.4 MMB/d over the same period.

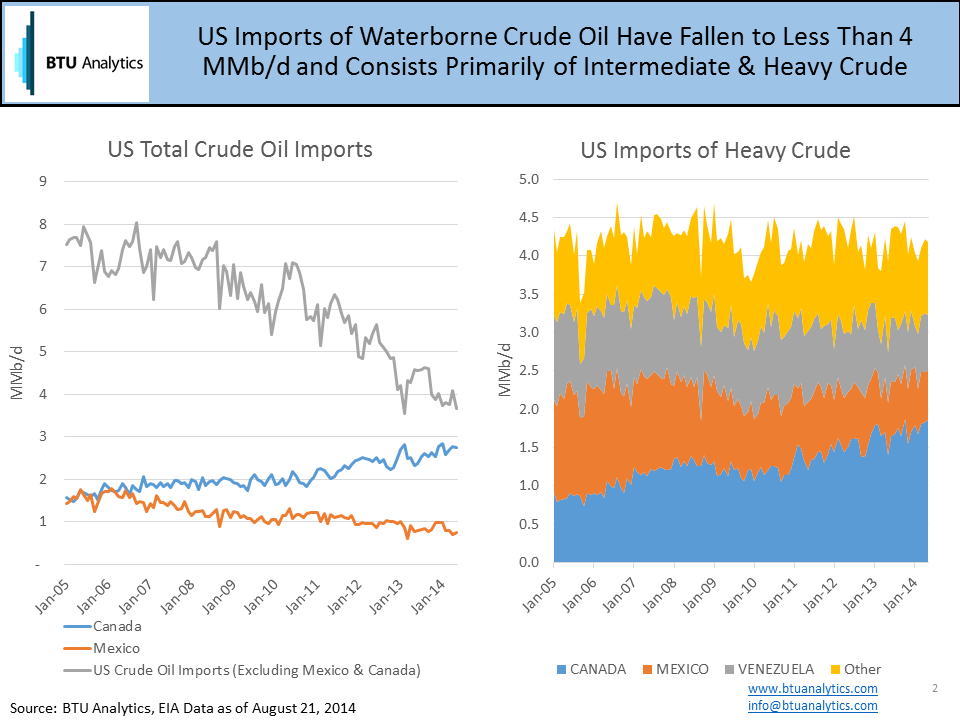

The displacement effect has had a varying impact on the countries sending crude oil to the US. Canada has become an increasingly important import partner over time as Canadian imports of Syncrude and heavy crude have increased from 1.56 MMb/d in the first half of 2008 to over 2.73 MMb/d through May of 2014. Growth in those years was driven primarily by the expansion of Enbridge (0.8 MMb/d) and Keystone Pipeline (0.6 MMb/d), which provided the Chicago and Cushing markets access to highly discounted Canadian supply. Mexico has lost market share in the US as declining production combined with higher global prices have pressured Maya to find new markets in Europe and Asia. Crude imports of heavy oil have been a zero sum game over the last 5 years averaging around 4.2 MMb/d and each incremental barrel of Canadian Heavy has displaced its waterborne competitor to the international market.

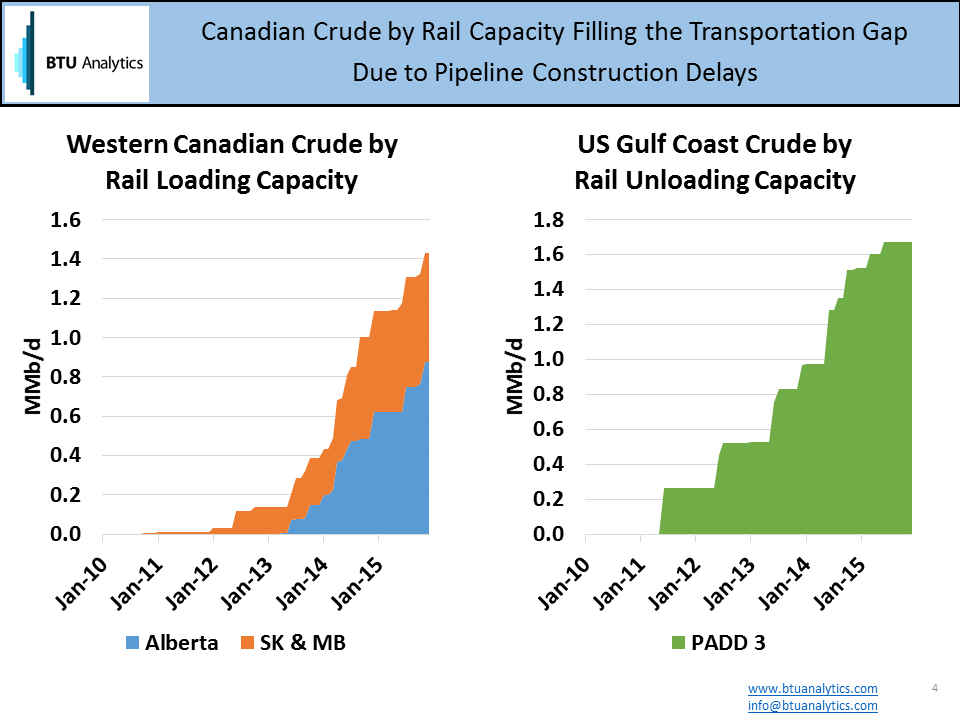

With the increasing unrest and political turmoil in Venezuela and the potential sale of the CITGO refineries, the gulf coast may soon be looking for new sources of heavy crude oil supply. Imports of heavy crude oil from Venezuela have averaged 0.7 MMb/d YTD which accounts for approximately 28% of the country’s production. Should inflation and proposed changes to gasoline subsidies destabilize the government, resulting in production curtailments or other disruptions, Gulf coast refiners will have to look to the land of the North for incremental supply. With the prolonged regulatory delays in Keystone XL pipeline (O.8 MMb/d), which was originally slated for commercial operation in late 2014, Gulf Coast refiners will turn to crude by rail (CBR) to meet incremental supply needs of heavy crude oil.

Crude by rail loading and unloading capacities have ramped up significantly in the last two years as producers, refiners, and marketers have looked to capture North American crude oil spreads. Data compiled by BTU Analytics indicates over 40 terminals with 1.4 MMb/d of capacity are under development in Canada and over 30 terminals in the Gulf Coast with capacity of 1.6 MMb/d. Canadian crude oil shipments by rail are currently estimated at 200,000 B/d utilizing AAR data for Canadian crude and refined product shipments but are expected to grow to over 500,000 B/d in the next several years as heavy oil production from the oil sands increases.

Can crude by rail support enough growth in Canadian crude imports to fill in the gap, should Venezuelan supplies be disrupted? It will depend on the timing. But we will be watching and waiting.