Yesterday’s announcement that Range Resources (NYSE: RRC, $RRC) is acquiring Memorial Resource Development (NASDAQ: MRD, $MRD) caught many in the market by surprise. Why would a large Appalachian gas-weighted producer with many years of drilling inventory and significant pipeline commitments look to purchase another gas-weighted producer outside of its footprint?

While the transaction will allow Range to reduce some leverage ratios in the near term, it may also be a signal that being an Appalachian pure play is becoming riskier in the face of infrastructure delays and cancellations.

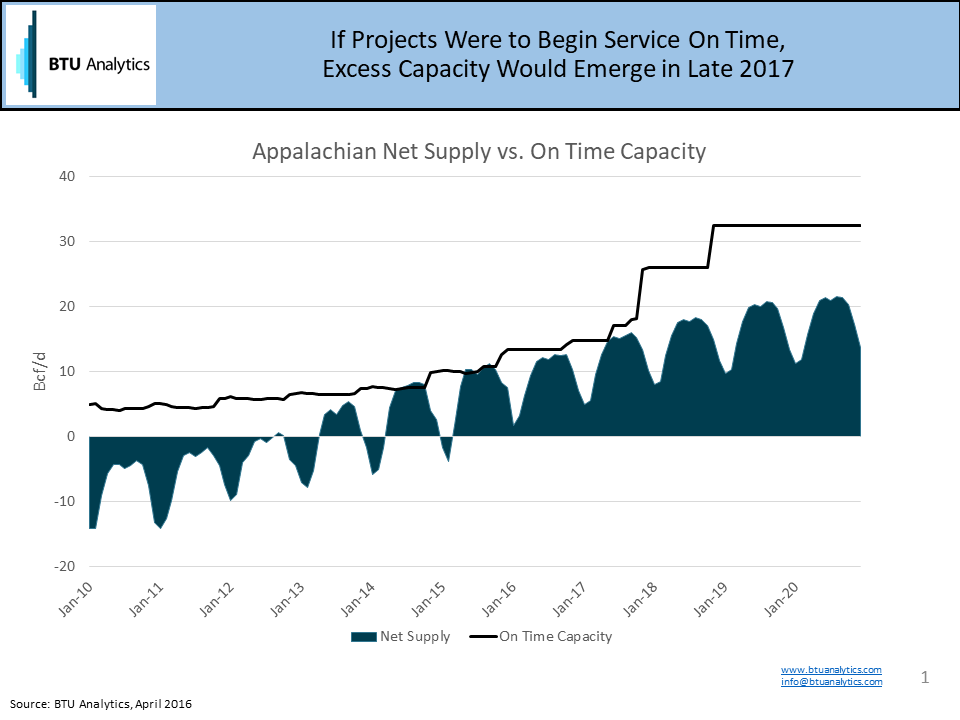

In the past we’ve highlighted the impact that all the proposed pipeline projects could have on the North American market should they all come on as proposed. In that scenario, pipeline capacity out of the region would go from being fully utilized to having more than 10 Bcf/d of open capacity, shrinking regional differentials and allowing producers who did not enter into firm takeaway agreements to produce into open pipe.

More recently, we’ve committed considerable space in our commentary to the growing risk that many of the major projects could be delayed or even cancelled. It’s a major factor behind the bullish gas thesis we first highlighted in February and has since become market consensus. What is the most likely scenario is that some, but not all, projects will make their way to market, and a sub-section of those projects will be delayed. This presents a real risk to producers in the region. If only a select number of projects make their way to market, the producers with firm transport on those projects will have a golden ticket to higher gas prices, while everyone else in the basin will be stuck with netbacks that stifle production growth and slowly bleed out balance sheets.

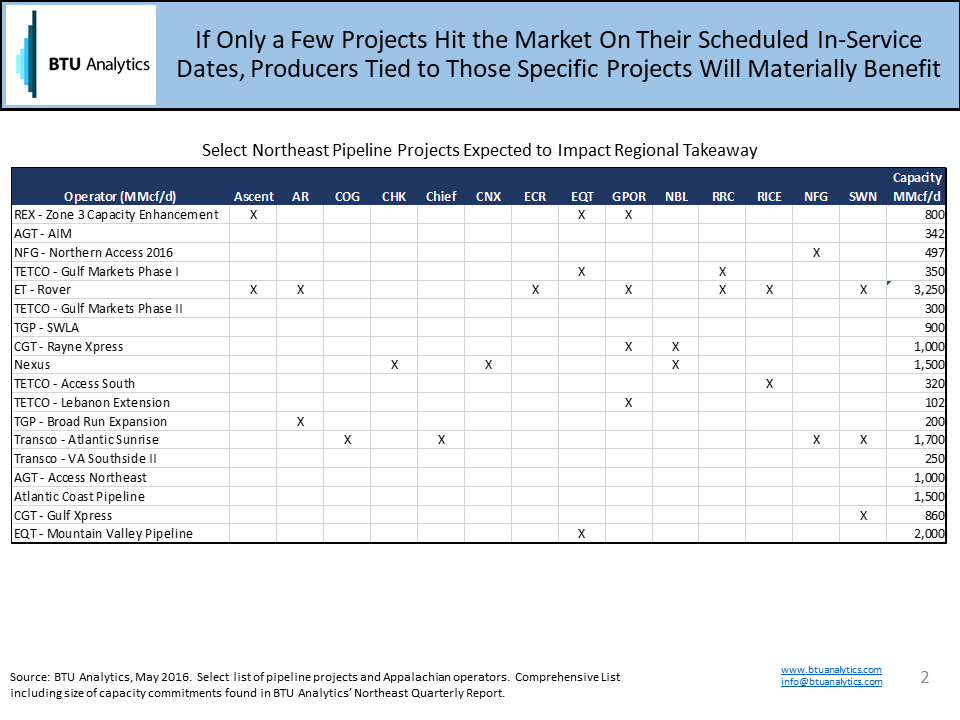

The table below illustrates the playing field of which producers have made commitments to which pipeline projects. Range has made pipeline commitments on at least three new projects coming out of the Northeast — Rover, Rayne/Leach Xpress and Adair SW, all due to market in 2017. The Memorial transaction provides optionality for capital investment should any of those projects not move forward as scheduled, particularly because delays would likely mean higher prices outside the Northeast, which MRD production would benefit from. Is this transaction a signal that the Appalachian pure-play strategy is worrisome to the folks with the best information on project timing outside of the pipeline companies themselves?

For more granular data on pipeline projects, announced in-service dates, producer commitments, markets impacted and thoughtful market commentary, request a copy of our Northeast Quarterly.