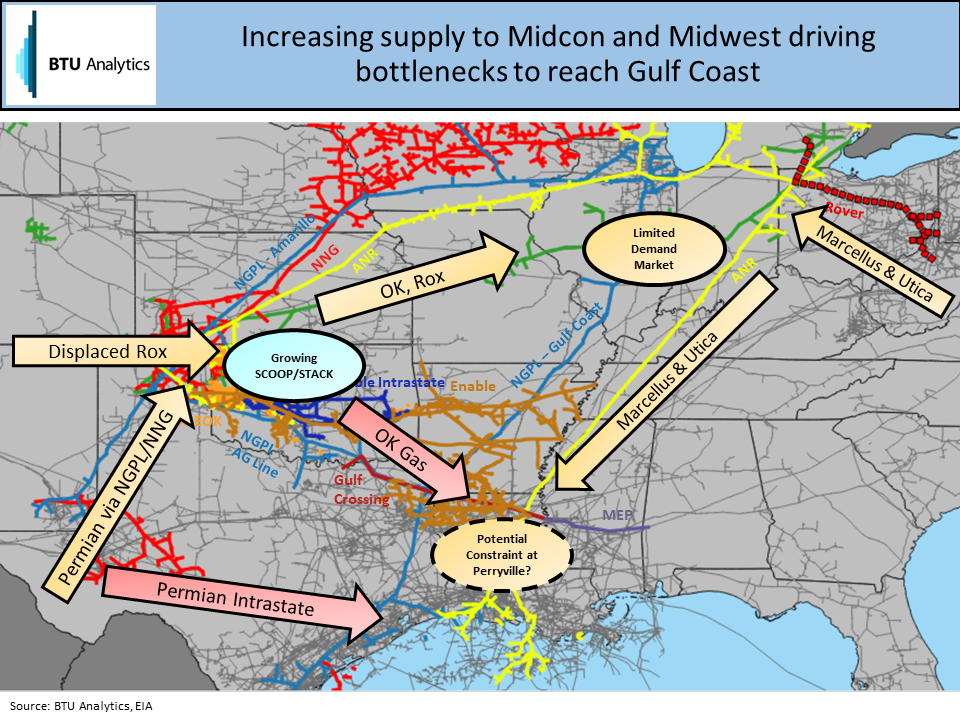

Congestion on the natural gas pipeline grid continues to progress further south as volumes from the Marcellus, Utica, STACK, SCOOP, and Canada fight for limited markets in the Midwest. The result of new pipeline capacity out of Appalachia has been a tightening in Dominion South basis in 2018, but the growth in outflows from the region has begun to weigh on downstream markets as well. In our June 2018 Upstream Outlook, we outlined how the growth in supply from both the Marcellus/Utica, Permian, and STACK/SCOOP would put further pressure on Carthage and Perryville pricing as highlighted in the diagram below.

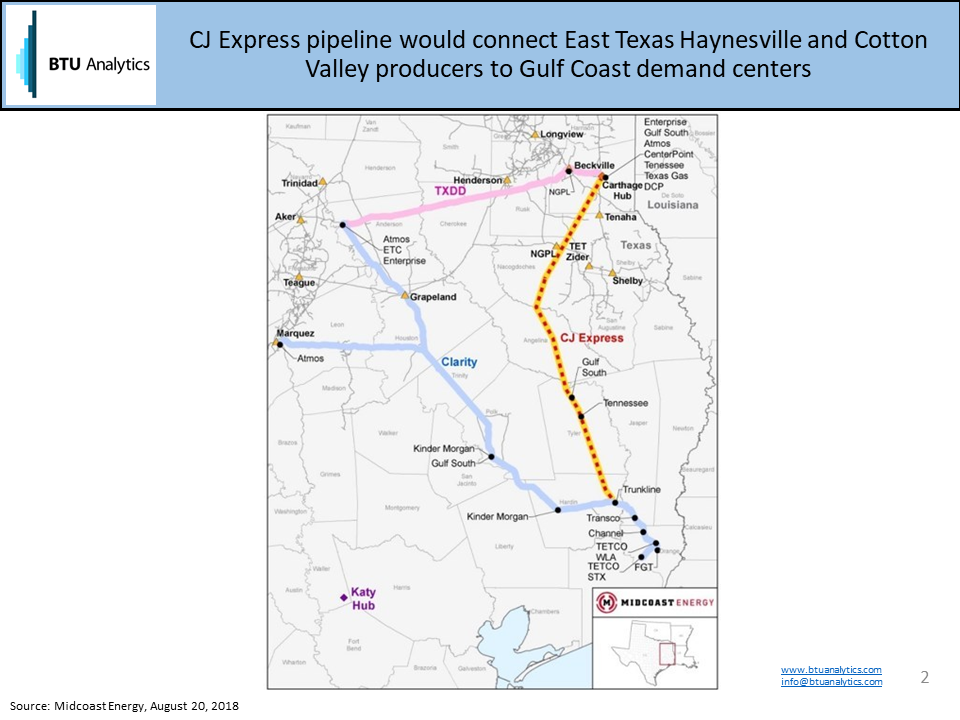

On August 20, 2018, Midcoast Energy announced a new potential solution for Haynesville producers feeling the pressure to move their molecules further south. The CJ Express pipeline would consist of 150 miles of 36” or 42” pipeline, which would provide between 1 and 2 Bcf/d of new takeaway capacity from the Carthage Hub to the Gulf Coast. The project is currently offering a non-binding open season, indicating that it is still testing the waters for the project but could potentially be in-service by mid-2020.

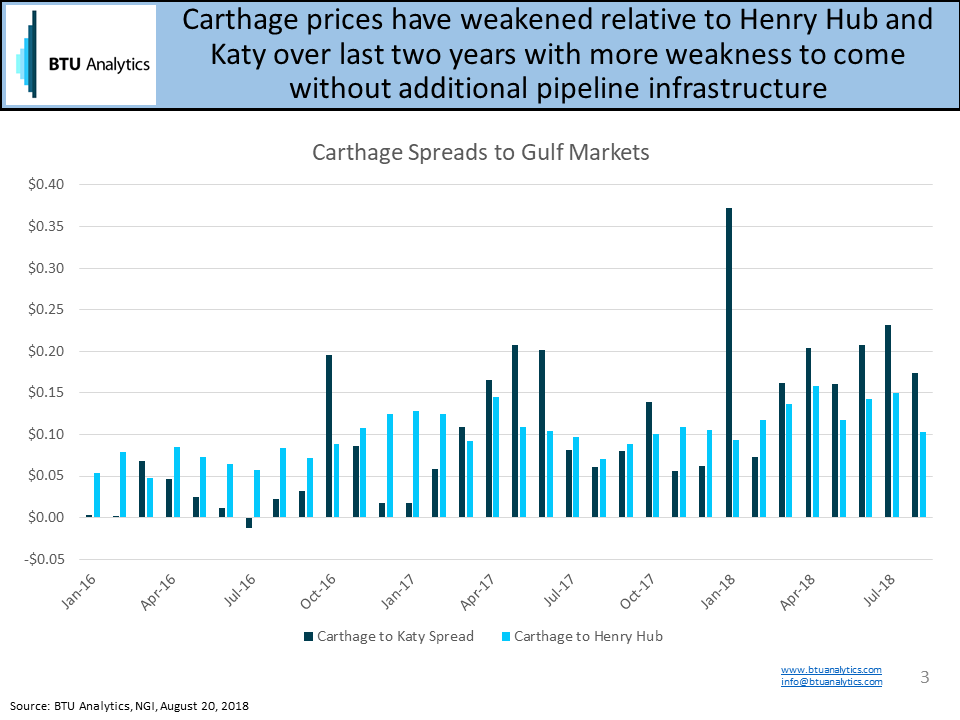

The growing need for this project or another like it is highlighted by the growing divergence between Carthage pricing and Gulf Coast pricing (Katy and Henry Hub). Over the last two years, Carthage prices have weakened to a $0.13 discount to Henry Hub YTD in 2018 compared to an $0.08 discount in 2016. However, the trend has been an increasing discount and more supply is expected to come from a combination of growth in the Haynesville and Cotton Valley, in addition to the impact of new pipeline capacity (Rover, Midship). However, when compared to the Katy market a little further west, the spread has widened even more as growth in demand has put upward pressure on Katy and Houston Ship Channel (HSC) pricing.

The spread between Carthage and Katy averaged just $0.04 in 2016 and has now grown to $0.16 YTD and reached nearly $0.35 in January 2018 when cold and snow reached as far south as Houston. Even excluding the cold snap in January, the spread has continued to widen for much of the summer as additional LNG export capacity at Cheniere’s Sabine Pass has come online.

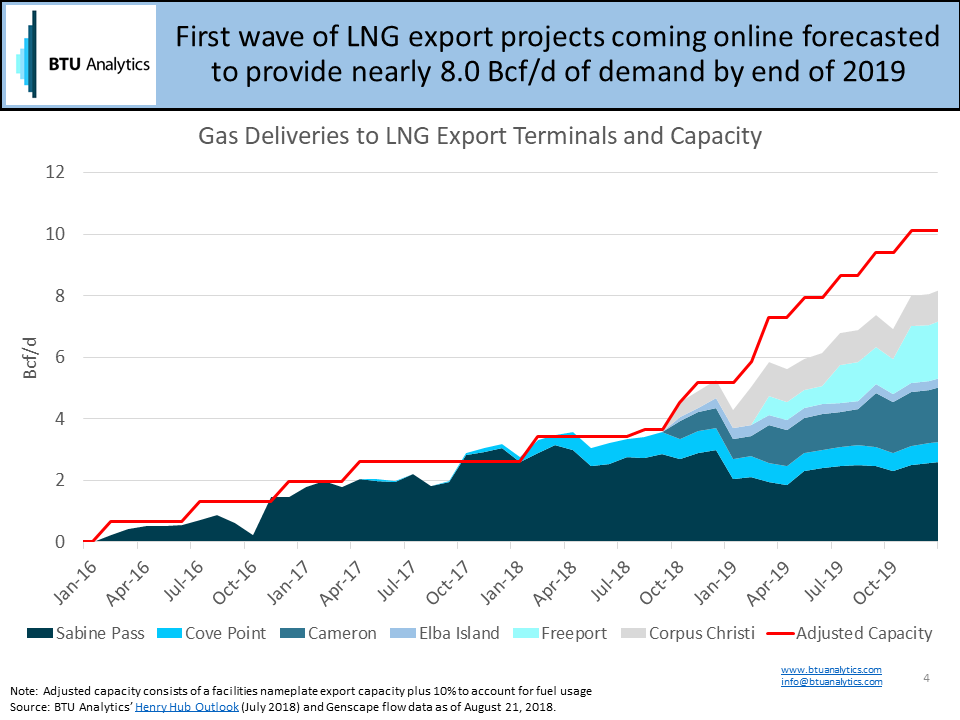

Over the next twelve months, additional trains at Corpus, Cameron, Elba and Freeport will begin to liquefy natural gas adding new demand along the Gulf Coast. While BTU Analytics expects there to be sufficient supply to meet this demand, new pipeline infrastructure to bridge the gaps will be critical. For timely insight on the latest impacts of infrastructure and production, request more information on BTU’s Upstream Outlook.