Coal company bankruptcies have been a recurring theme in 2019. This was reinforced this week by the chapter 11 filing of Murray Energy, which is the US’s largest private coal mining company. Over the last decade, low-cost shale gas in combination with environmental pressure targeting coal emissions has had a massive impact on US thermal coal demand. During this time, natural gas power generation has consistently taken market share from coal-fired generation. However, the major impact of low-cost natural gas on coal generation is likely largely over. This Energy Market Commentary will look at the conditions that have lead to coal bankruptcies and look to the future as coal and gas now face a new formidable opponent in the form of wind and solar generation.

**BTU Analytics is releasing new analytic coverage with the forthcoming Gas-Renewables Outlook – to be put on an early release list of the report, email contact information to info@btuanalytics.com with GRO in the subject line.**

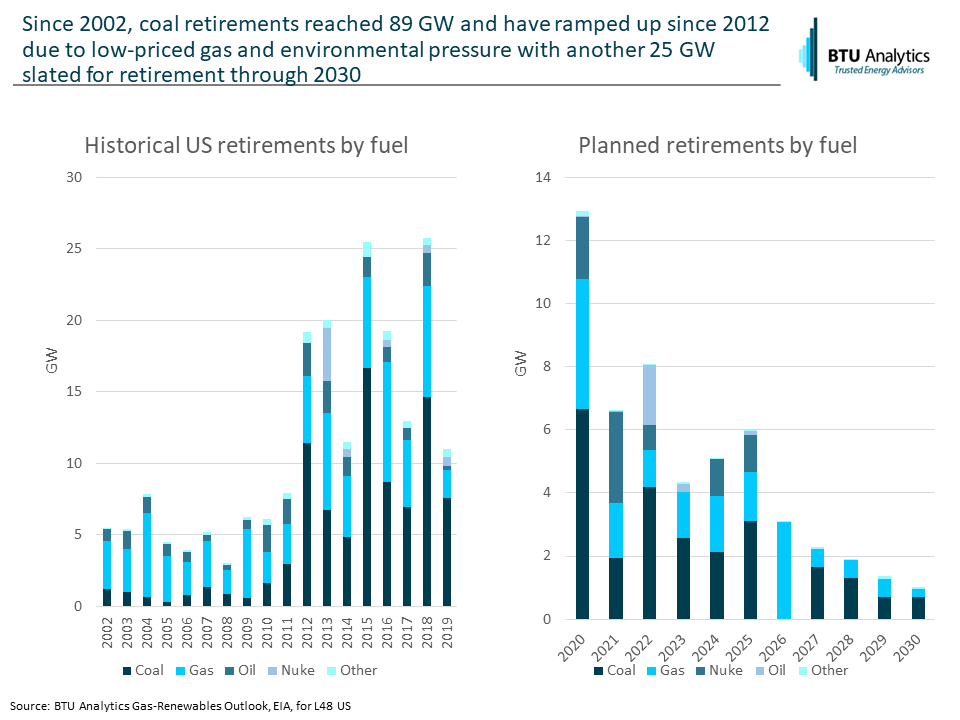

As shown above, since 2002 there have been 89 GW of coal retirements with over 77 GW of retirements happening since 2012. Although shale gas volumes began growing significantly in 2008, by 2012 the economics of multiple years of low-cost shale gas began to take a toll on coal-fired generation and resulted in coal retirements. The Clean Power Plan starting in 2015 provided further tailwind to retirements. Looking forward, there are another 25 GW of announced coal retirements through 2030.

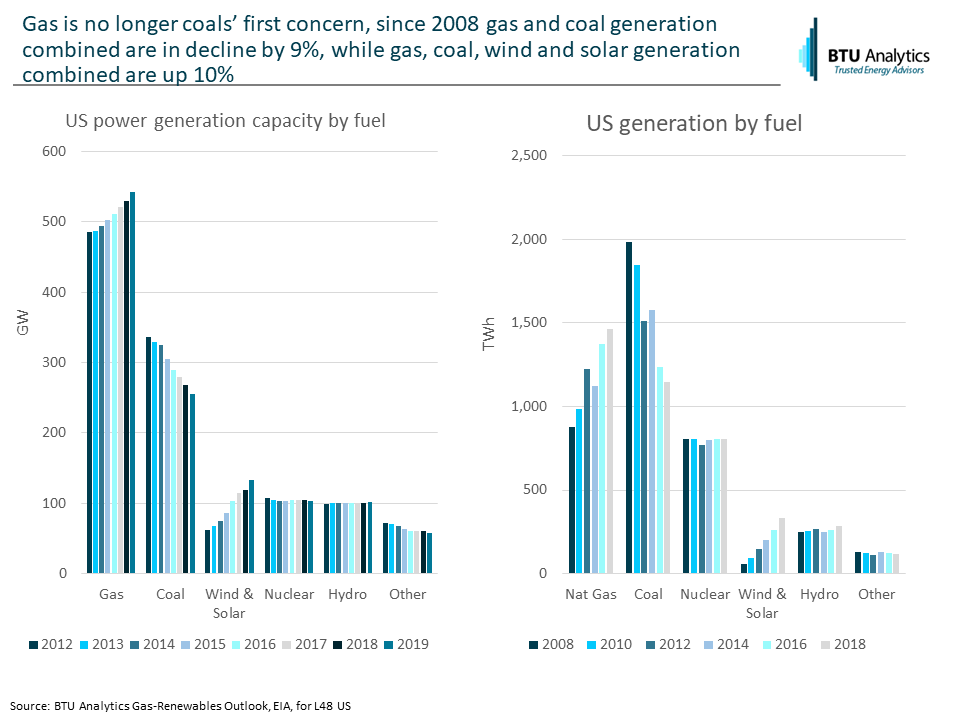

Looking at electric capacity and generation by fuel type, as shown above, we can see generally gas and wind & solar capacity and generation are increasing while coal has been decreasing. Coal generation is down 42% since 2008, while gas is up 67% and wind & solar are up 500%. It is interesting to note that as a pair, coal and gas generation are down 9% since 2008. This highlights the key role that increasing wind & solar are playing in the generation markets.

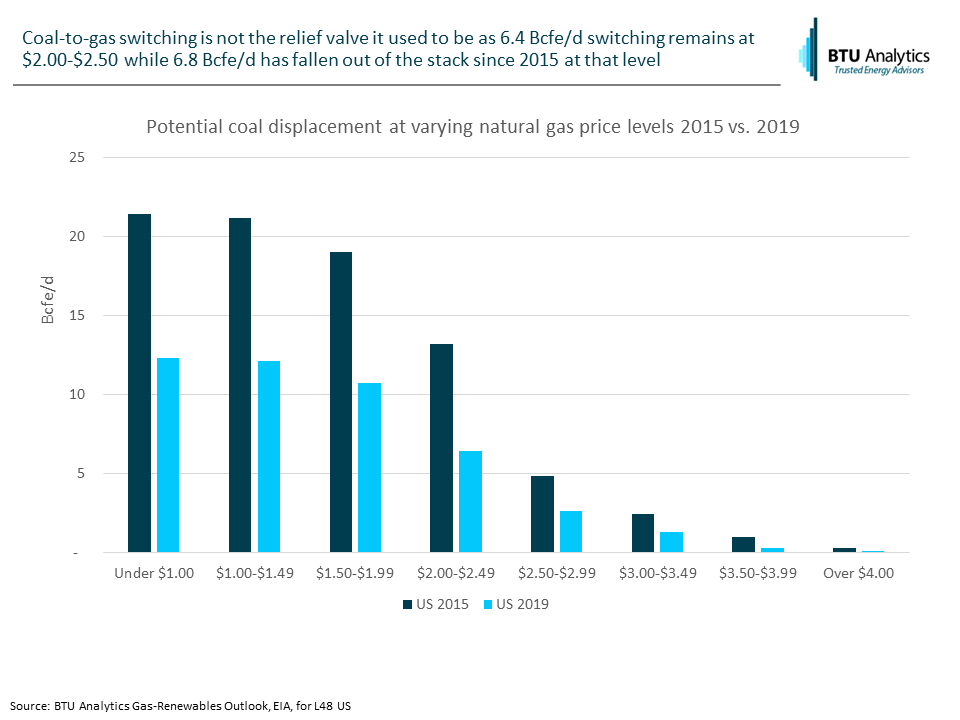

For many years, coal-to-gas switching was a lever that balanced the gas and coal markets based on respective commodity price levels. In periods of elevated gas prices and low coal prices, coal generation would climb, reducing gas-fired generation and vice versa. This fuel switching used to account for (as measured at the $2.00-$2.50 per Bcfe/d level) 13.2 Bcf/d in 2015 of incremental gas demand that could come in or out of the market based on price. However, as more coal retirements have occurred, in 2019 this number has declined to 6.4 Bcfe/d. None of this is good news for coal producers.

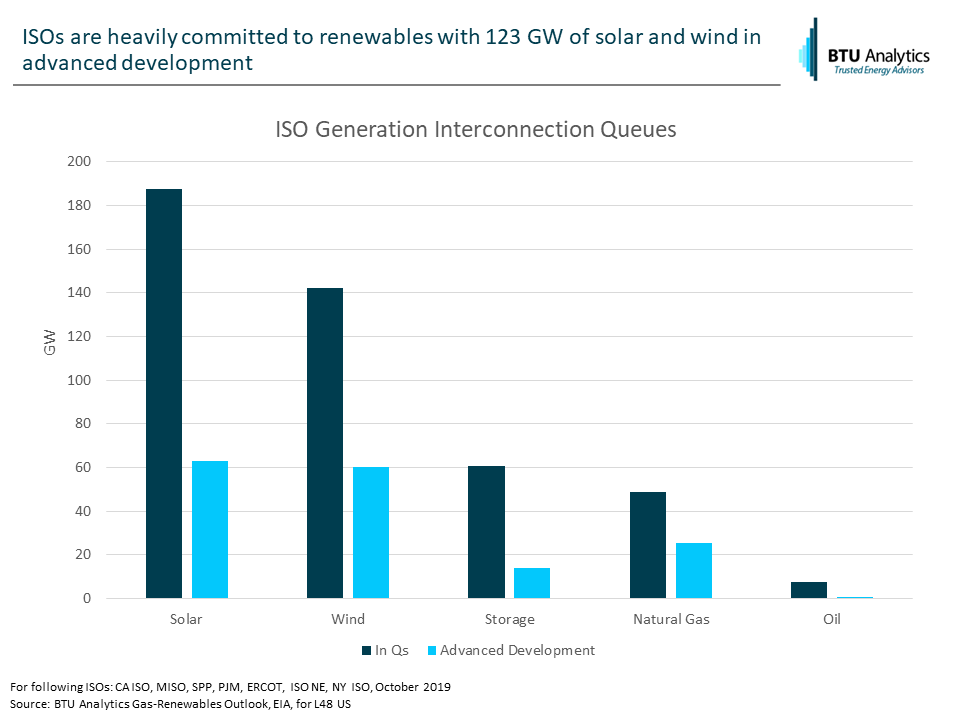

Looking forward at what generation is under development at the seven ISOs, as shown above, solar and wind hold the top spots. Solar and wind account for 329 GW of generation that are in the queues, considering all stages of development. When looking at the advanced stage development, as measured by projects close to or having received their interconnection agreements, solar and wind represent 123 GW of development. The next largest tranches of development by fuel type are natural gas plants (mostly in PJM) at 25 GW followed by battery storage at 14 GW (mostly in CA ISO). Gas is no longer coals’ number one foe, as both coal and gas now face a competitive future with wind, solar, and batteries. BTU Analytics is releasing new analytic coverage with the forthcoming Gas-Renewables Outlook – to be put on an early release list of the report, email contact information to info@btuanalytics.com with GRO in the subject line.