Over the past few years, Marcellus and Utica production has not only spurred a spate of pipeline projects (and pipeline problems) but has also pushed growth in natural gas demand within the region. The poster child of this demand growth has been natural gas-fired power plants, where capacity within the Northeast has grown by almost 50% since 2010. However, as power demand in the region has grown, dynamics around power burn in the Northeast have shifted as well. Coal-fired generation is no longer an easy target for gas plants to steal market share from. Instead, we are increasingly seeing more competition among natural gas power plants themselves.

If we were to pick winners and losers in the Shale Revolution it would be hard to put coal-fired power plants in anything, but the losers column. The proliferation of natural gas in the Northeast and around the country has driven power plant’s supply costs, and therefore power prices, down. Especially in the Northeast where natural gas-fired plants can be co-located near supply. Beyond coal plant retirements, non-retiring plants have seen their utilizations and their overall output fall as seen in the chart below, which converts coal plant generation into natural gas equivalent units. In Appalachia (defined as New York, New Jersey, Pennsylvania, Ohio, and West Virginia), generation from coal plants has fallen from about 7.5 Bcfe/d in 2010 to less than half that in 2018.

With the most uneconomic coal plants sidelined, the remaining coal generation will be more “sticky”, with many of the remaining coal plants located near coal production in West Virginia, Ohio, and Pennsylvania. So, assuming electricity demand continues to be mostly flat, as we have seen in recent history, who will natural gas plants compete with?

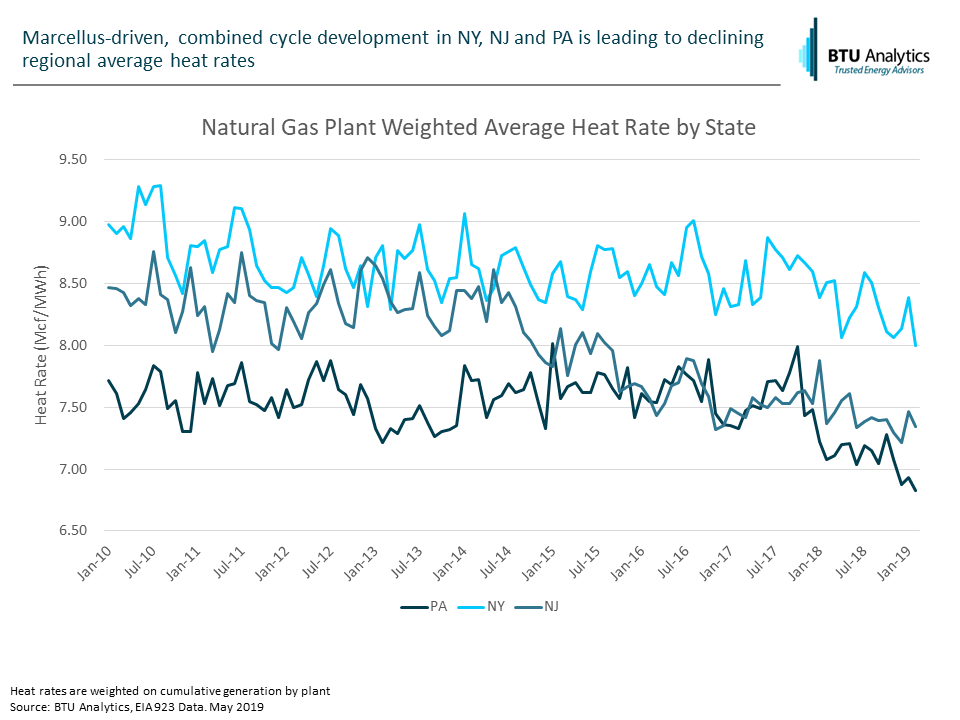

The answer to that is themselves. As new plants were built in the region, average plant efficiencies continued to increase and push new limits. The next graphic shows how natural gas power plant heat rates have evolved in the region. A power plant heat rate is a measure of how many Mcfs it takes to generate a MWh of electricity. The falling trend below means that an average plant is generating the same amount of electricity using less gas than compared to a plant five years ago.

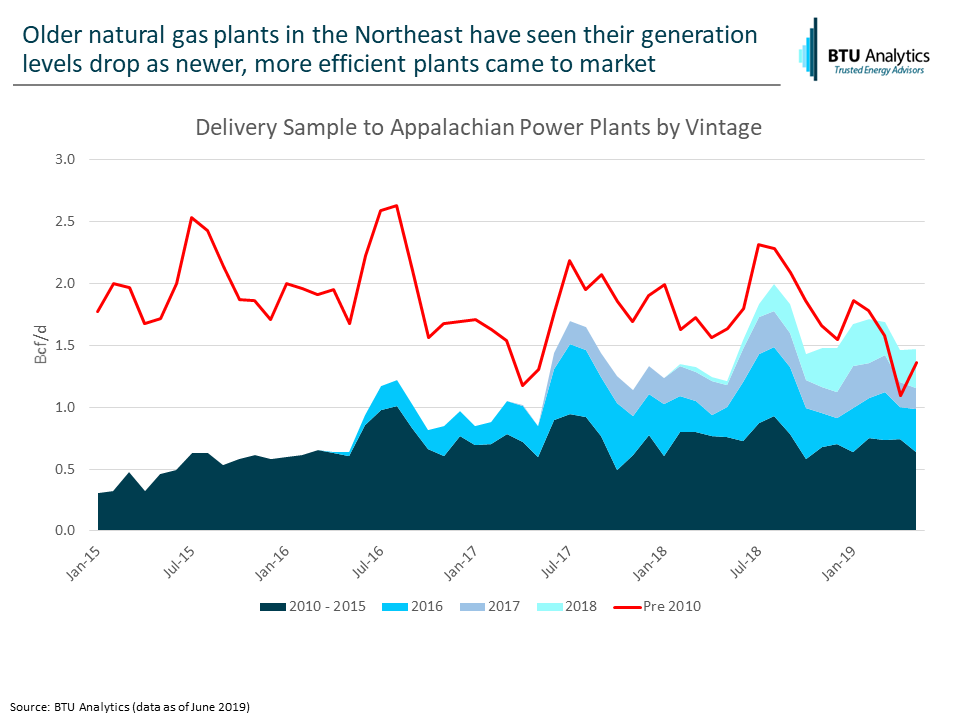

We can look at natural gas deliveries to a sample of these plants (plants connected to interstate pipelines) to see how increasingly efficient plants have shifted dynamics among gas plants. Below shows our sample of natural gas deliveries to gas plants by plant vintage. Older plants, especially those built prior to 2010, have seen their deliveries drop, as newer, more efficient gas plants have come to market.

So where do natural-gas plants go from here? There will certainly be more competition to come as the region is set to add another 13 GW of new, efficient generation to the stack. However, there are some outside players to watch for. First being, nuclear power plants. Indian Point in New York is set to retire over the course of 2020 and 2021. That will provide about a 0.4 Bcfe/d void for natural gas to step in to grow market share, instead of cannibalizing older gas plant’s utilization. On the flip side, if NIMBYism can be overcome, the prospect of offshore wind generation in the Northeast would put additional pressure on gas generation. However the market evolves going forward, one thing is certain – growing gas power plant market share won’t be as easy as it used to be.

For BTU’s take on how the market will play out in the Northeast, and around the country, check out the power section of our Henry Hub Outlook, and for natural gas, basis implications see our recently published Gas Basis Outlook.