The start of 2019 looks arduous for producers of crude and natural gas which are both off significantly after hitting 2018 highs in October and November, respectively. WTI is down more than 35% from October levels and natural gas is down nearly 24% from November. While nearly all outright prices are down across the board, not all regional prices are down by the same amount.

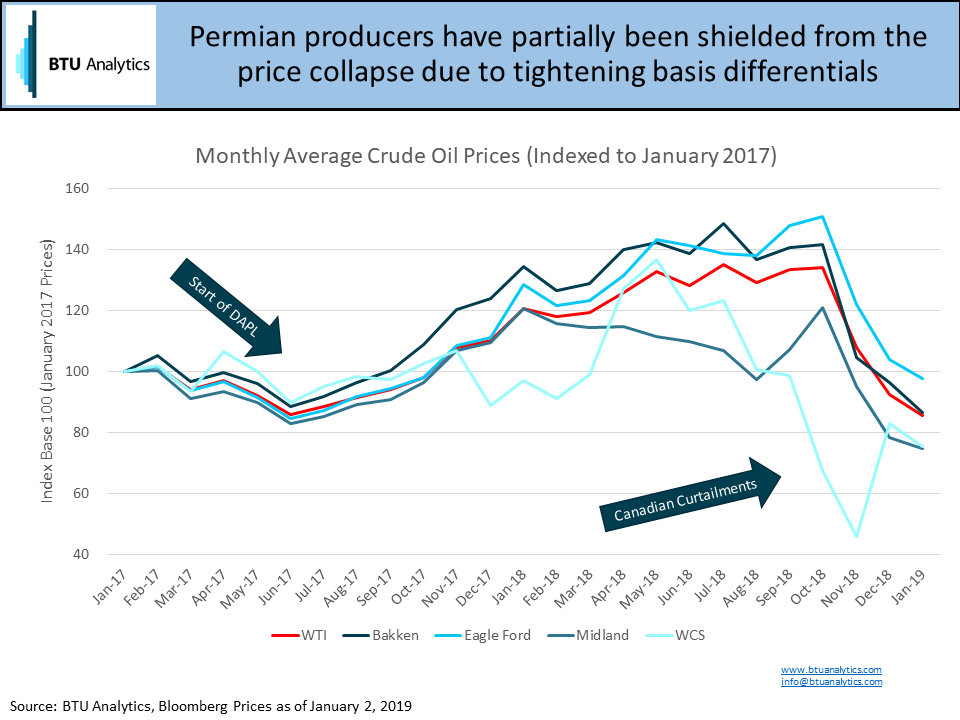

When looking at the crude market, the chart below shows crude differentials for Bakken, Eagle Ford, Permian, and Western Canadian Select (WCS) indexed to January 2017 average prices and normalized to a scale of 100. Throughout the first half of 2017, all prices moved in lock-step with each other, both up and down. Transportation out of each play was not constrained in the early part of 2017 allowing prices to fluctuate with the overall change in crude prices as can be seen with the correlation to WTI prices (red line in chart below).

The startup of DAPL in April 2017 tightened crude differentials for Bakken producers significantly, allowing them to capture tighter differentials to WTI and drive faster price appreciation relative to January 2017 compared to other basins. By early 2018 though, the Eagle Ford, Bakken, and Western Canadian Select (WCS) began to diverge from WTI. Capacity constraints in the Permian Basin resulted in Midland prices discounting significantly throughout the summer of 2018. While outright WTI prices were reaching a peak, producers in the Permian without firm transport or hedges were not seeing much improvement in price relative to early 2017. Correspondingly, new firm transport out of the Permian has coincided with the drop in WTI and Brent crude prices in Q4 2018. The new transport capacity has helped ease differentials in the Permian Basin, cushioning the fall in crude prices relative to their peers in the Eagle Ford and Bakken that were not experiencing the same significant discounts throughout summer 2018.

WCS prices have also rebounded since November as the Alberta government announced production curtailments (Check out the December Upstream Outlook for a full review and expected impacts). The production curtailments have resulted in a significant tightening of differentials in the region, also helping to cushion the fall in WTI and Brent prices, but prices still remain nearly 20% below where they started in January 2017.

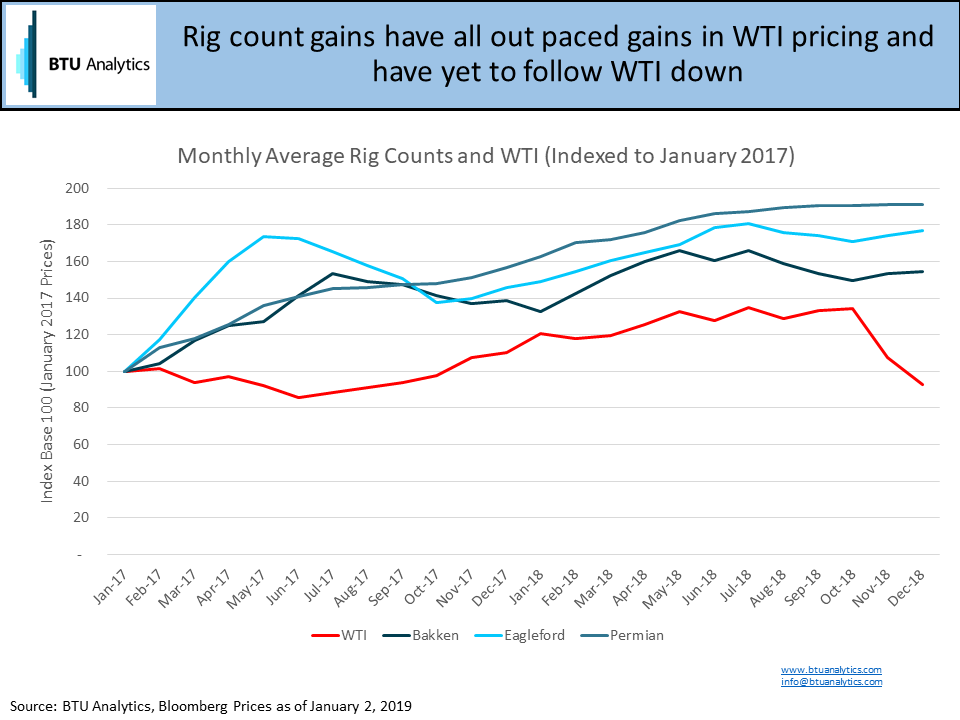

In the summer of 2018, producers in the Bakken and Eagle Ford were seeing prices nearly 40% higher than the start of 2017, but Permian producers were only realizing prices on par with early 2017 prices. Rig counts generally lag pricing dynamics, but not in 2017 and 2018. While the gains in pricing in many regions did not occur until late in 2017, the rig count in many of these basins was already heating up early in 2017. In percentage terms, the Eagle Ford saw the fastest rise in early 2017 growing from 53 rigs in January 2017 to over 90 rigs by May. The slump in crude prices in mid-2017 saw producers cut activity quickly back to just 72 rigs by October as highlighted in the chart below

The Bakken and Permian added activity throughout that time frame with the Bakken leveling off for most of 2017 and 2018 as natural gas processing constraints, asset turnover, and higher breakeven costs stemmed additional investment. However, the Permian continued to add activity despite overall pricing remaining relatively unchanged at +12% on average from January 2018 to October 2018 compared to January 2017. Comparatively, realized pricing in the Eagle Ford was up 36% and the Bakken was up 38%. Permian activity by year-end 2018 is up almost 200% from January 2017 levels.

Waves of new infrastructure being developed in the Permian should significantly tighten crude differentials at Midland by the end of 2019. Permian producers electing to hold out for improving differentials could see outright prices improve even if the overall price of WTI does not rise from today’s levels of $47.

While some producers have started announcing small CAPEX cuts for 2019, the likelihood of significant scale backs in activity seems muted compared to 2015. In 2015, producer balance sheets were already stretched thin by years of outspending cash flow. But in 2017 and 2018 producers have been focused on spending within cash flow and many Permian producers have already begun to return cash to shareholders via share buybacks and dividends. As OPEC cuts begin to take supply out of the market and new infrastructure allows crude to reach higher priced Gulf Coast and international markets, producers in the Permian and other plays will likely see upticks in realized prices allowing them to continue ahead, though maybe at a more tempered pace. For more information, check out our monthly, Oil Market Outlook.