The front months of the futures curve gets all the attention. Yes, the crude oil price sell-off has been relentless with WTI down $59/bbl or 56% since June 2014. Meanwhile, the 2018 WTI strip is down $20/bbl or 23% to $64 during the same time frame.

Some in the press like to frame up the sell-off as ‘The Frackers’ vs Saudi Arabia. Aggressive North American unconventional oil producers armed with technology and capital and lack of OPEC accord are a big part of the story. However, what seems to get lost in the daily news is the reshuffling of the supply stack in 2018 and beyond as long-lead capex-heavy projects (think Canadian oil sands, anything Arctic, offshore, etc.) are getting slashed or delayed. This void creates fertile ground for nimble North American unconventional oil producers that can more quickly react with flexible drilling programs as WTI recovers once the global and North American overhangs have been worked off in coming years.

Here are a few examples of long-lead capex-heavy cuts:

– In December Cenovus announced it would slow spending on longer dated oil sands projects with in-service dates of 2017 and beyond.

– Earlier this month Suncor announced projects that have not yet been approved like the MacKay River 2 oil sands project at 20,000 bbls/day and the White Rose offshore project in Newfoundland have been deferred. Both had in-service dates in 2017.

– Earlier this month Statoil said it may further delay its arctic Castberg project in the Barents Sea with a target of 2.5 million Boe production by 2020.

In many ways, the North American unconventional oil players that are good stewards of capital are geared for this new oil market. They sit in the biggest crude oil market in the world and are armed with a quiver of production tranches at various economic breakevens.

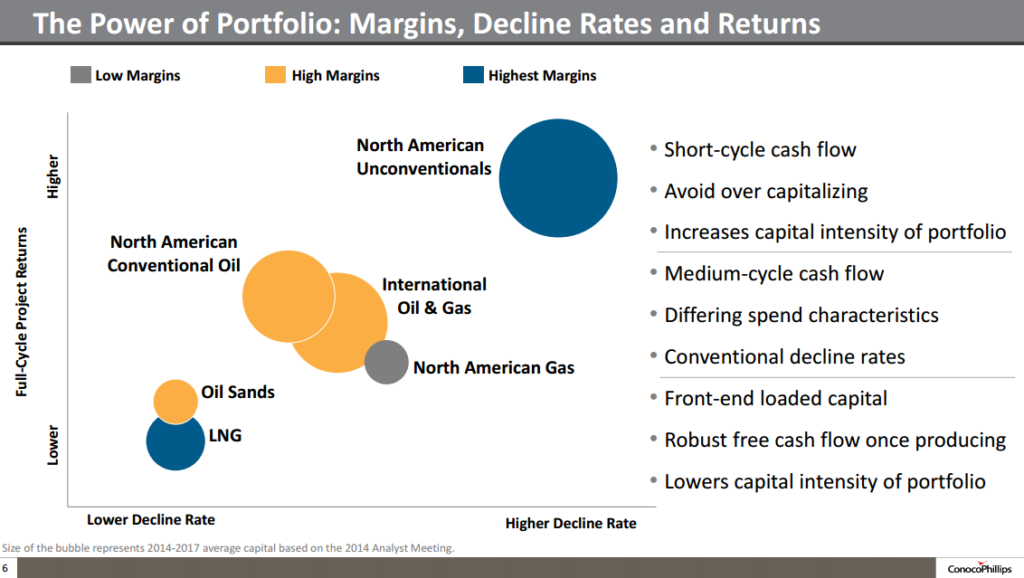

If we use a slide from a recent ConocoPhillips IR deck we can see the portfolio of options out there for larger E&P companies. North American unconventional oil has high returns and high decline rates. High decline rates are exactly what the North American crude market needs – that impact is coming once we work through the remaining momentum of record 2014 drilling and announced capex cuts start to materialize in the field. Notice below, the lower return and lower decline rate options such as offshore, arctic and oil sands all represent big, long-lead capital intensive projects. The more of these projects that get scrubbed, the more opportunity that exists for fleet-footed unconventional onshore oil players to capture that supply curve in 2018 and beyond.

Source: ConocoPhillips Investor Presentation

So back to the front of the curve – everyone knows not much new drilling is economic at current realized wellhead pricing. However, the more long-lead capex-heavy projects that get cut, the more overdone the $64 WTI 2018 strip looks. The question is who and what projects will actually create the supply to meet that demand in 2018 and beyond.