In discussions with clients, a frequent topic for debate is the appropriate level of US LNG exports. With the growth in estimated recoverable resources in North America driven by shale development over the last 15 years, the US natural gas market has flipped from building LNG import terminals to developing LNG exporting facilities. Development of liquefaction capacity in the US is unique in that the US is the largest consumer and producer of natural gas in the world. Thus, the development of LNG will require walking a fine line between meeting domestic consumption at competitive prices while taking advantage of arbitrage against higher priced, global LNG markets. This Energy Market Commentary will compare the US LNG exports as a percentage of production and consumption to other global LNG exporters.

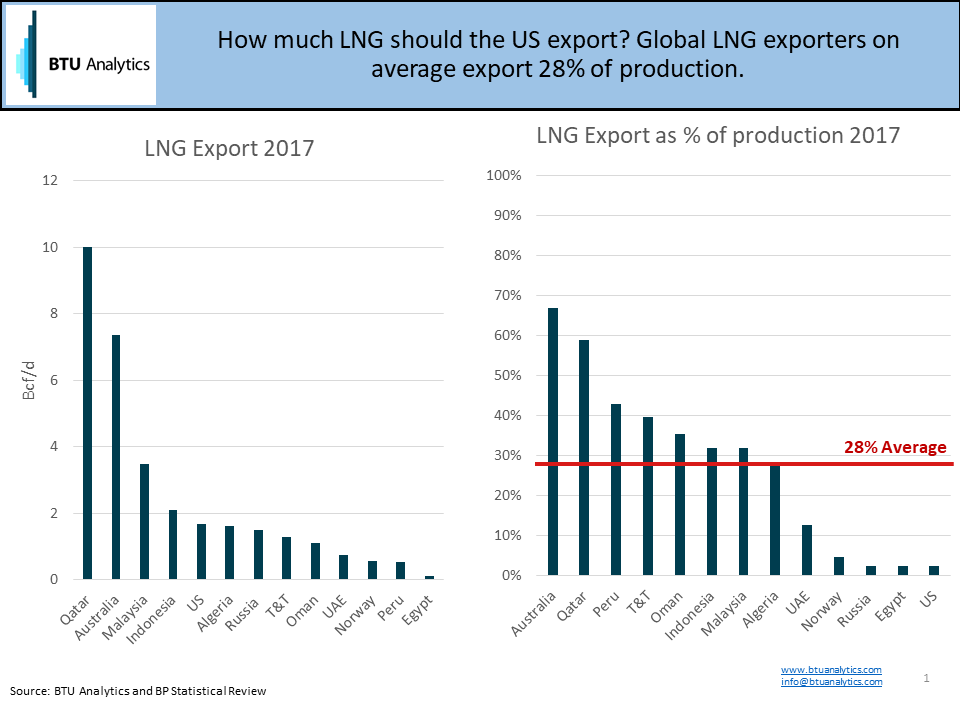

As shown above, left, based on 2017 LNG exports, Qatar still holds the position of being the largest LNG exporter at 10 Bcf/d compared to 1.7 Bcf/d for the US. However, the United States exported an average of 3.2 Bcf/d in 2018 year to date and will develop 10 Bcf/d of LNG export capacity by the 4th quarter of 2019. The chart to the above and right compares LNG exports as a percentage of each countries’ total production. Australia and Qatar export over 50% of their production while Russia, the second largest producer of natural gas in the world, exports a tiny fraction of supply via LNG, but a larger volume than shown above is exported via pipeline. Similarly, the US only exported a fraction of natural gas production as LNG in 2017. On average, the major producers of global LNG supply export 28% of production to global markets. Production in the US is on track to exceed 100 Bcf/d over the next five years, which if LNG exports were to develop to hit the global average then US LNG exports would need to be nearly 30 Bcf/d.

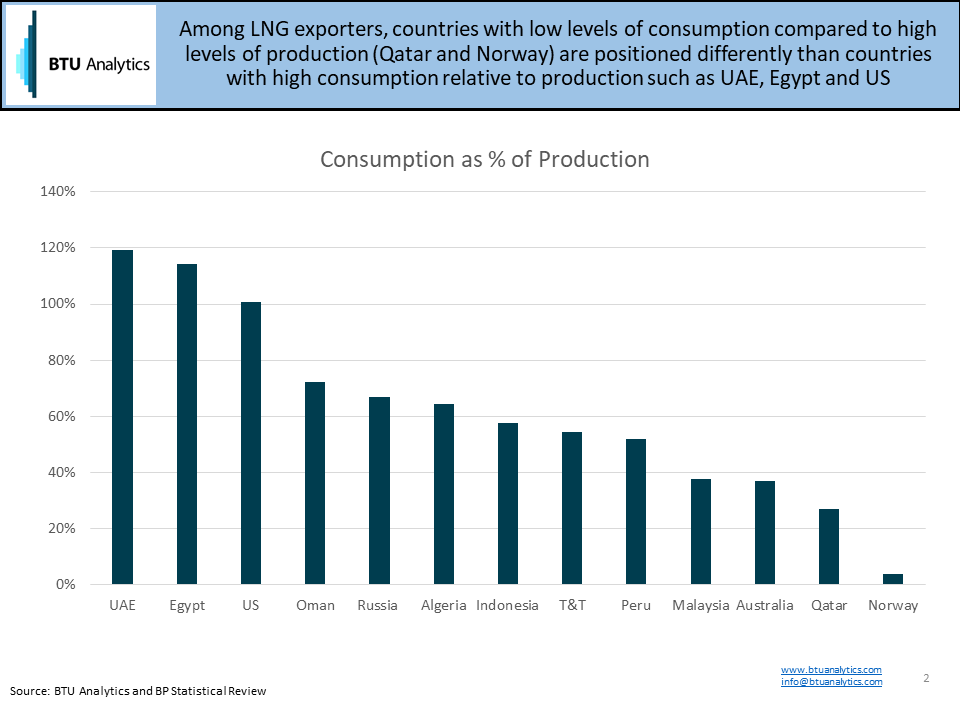

However, if we look at LNG export country’s consumption levels, the US is in a league of its own as the largest consumer of natural gas in the world as shown above. For domestic consumers of natural gas in the US, the optimal LNG export level is zero to keep prices low, while E&Ps want as much demand in the form of LNG export as possible to boost prices and accelerate development of acreage. Currently, US natural gas producers are growing supply to meet ramping export demand (round 1 LNG and Mexico) while the growth in domestic demand (rescom, industrial, and power) has slowed.

So what is the appropriate US LNG export level? While the US is waiting for potential round 2 of LNG FIDs along the Gulf Coast and potentially the West Coast, the previously mentioned 30 Bcf/d (the global LNG export vs. production average) is probably too high as compared to the currently announced 10 Bcf/d online by Q4 2019. The answer likely lies somewhere in between.