While the SCOOP and the STACK have launched into the spotlight and are expected to drive much of the growth from Oklahoma over the next five years, out of favor areas like the Granite Wash in the Anadarko Basin continue to provide opportunities for companies to consolidate acreage in anticipation of future drilling programs.

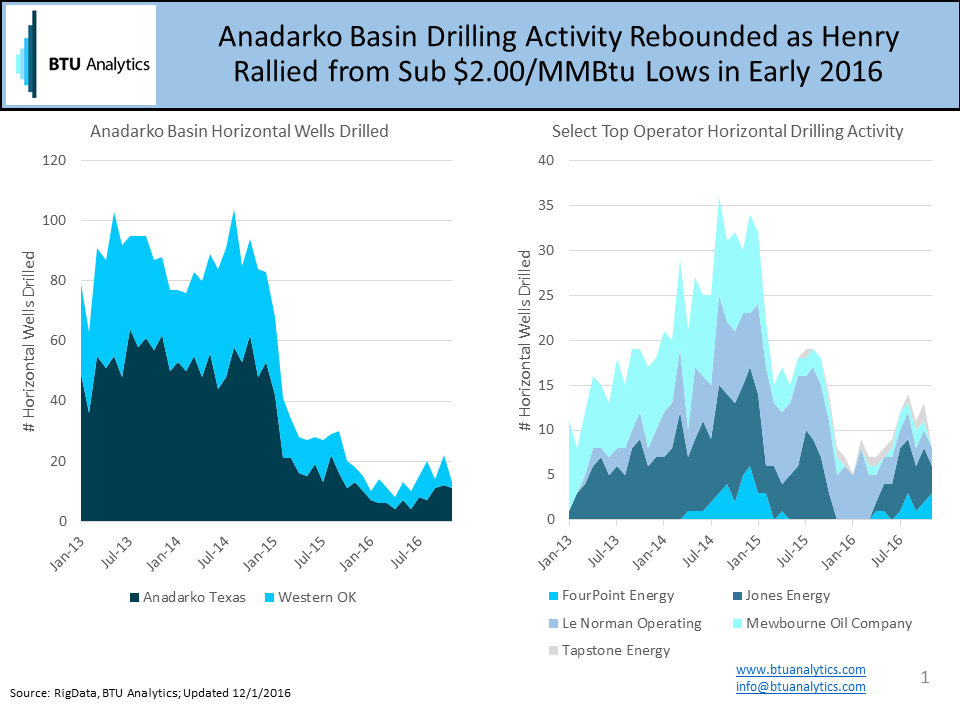

After gas prices collapsed in 2012, acreage prospective for the Granite Wash/Cleveland started to shift hands as many producers looked to make the shift from gassier plays to plays producing more crude like the Bakken and Eagle Ford. When both oil and gas prices experienced significant weakness in 2015 and 2016, regional consolidation continued and major players like Chesapeake sold out of the Western Anadarko Basin. Now that natural gas prices have started recovering, companies like Jones Energy, Le Norman Operating, FourPoint Energy, Mewbourne Oil, and Tapstone Energy have capitalized on their consolidation efforts and restarted or increased drilling in the area.

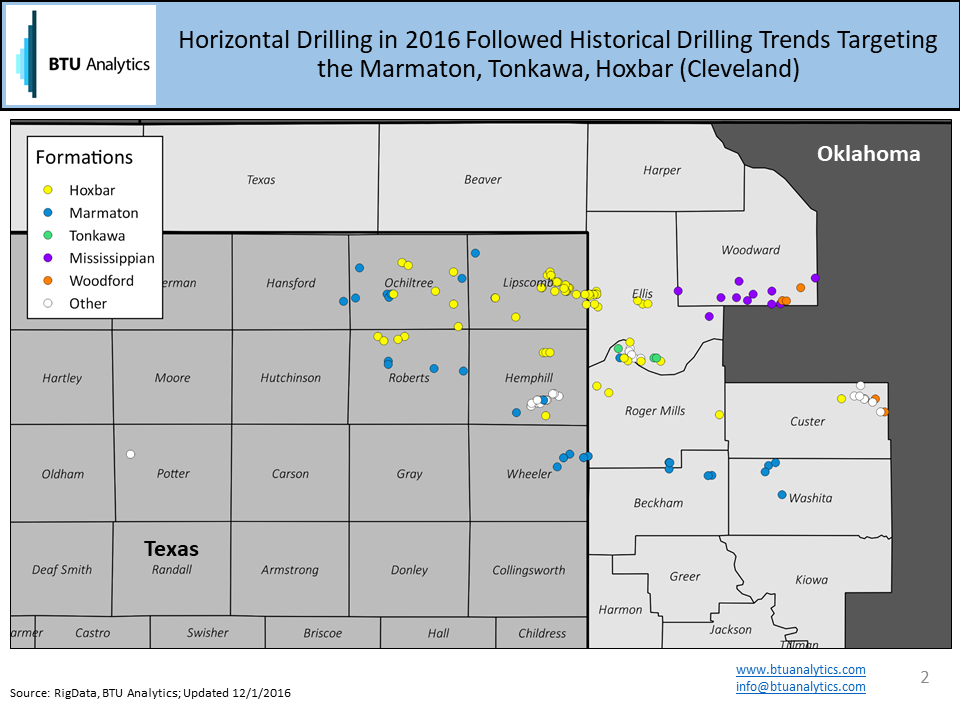

With the exception of Jones Energy, all of these companies are privately held, limiting the amount of publicly available information about the region. However, if we look at drilling and initial production rates which are available, we see that horizontal drilling in 2016 has followed historical basin trends as producers continue to target the Hoxbar, Tonkawa, and Marmaton groups which contain the well-known Granite Wash and other washes like Hogshooter, Checkerboard, Cleveland, and Cottage Grove.

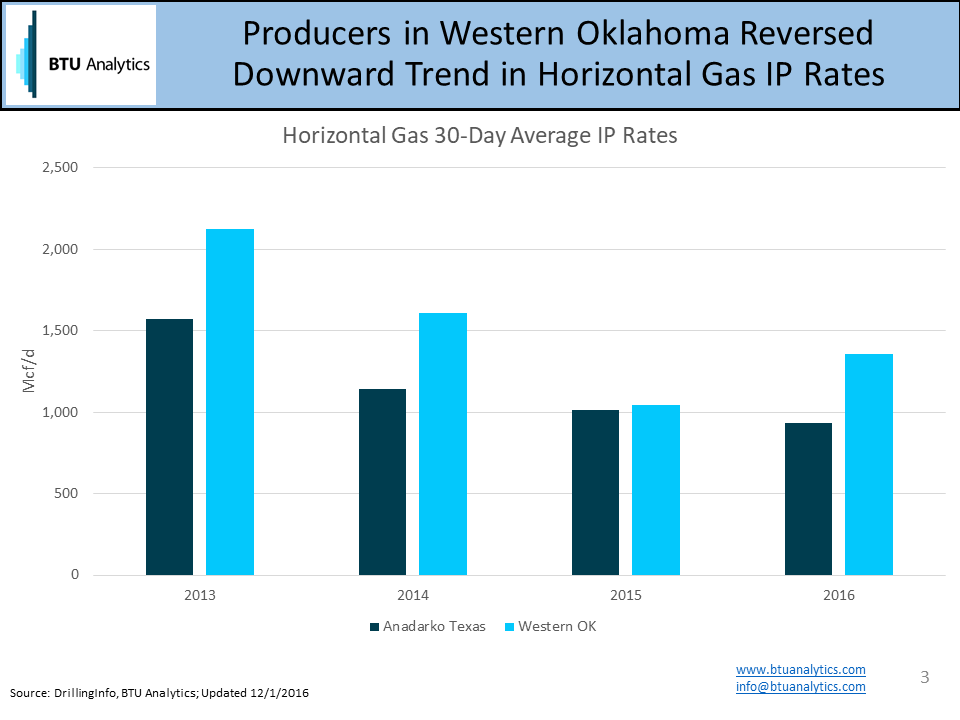

While 2016 data is still incomplete, examining initial production rates for gas for the Texas side of the play compared to the Oklahoma side reveals interesting trends. In Oklahoma, preliminary data suggests that operators have been able to reverse the downward trend in average gas IP rates experienced over the past few years. The Texas side of the play does not show the same trend.

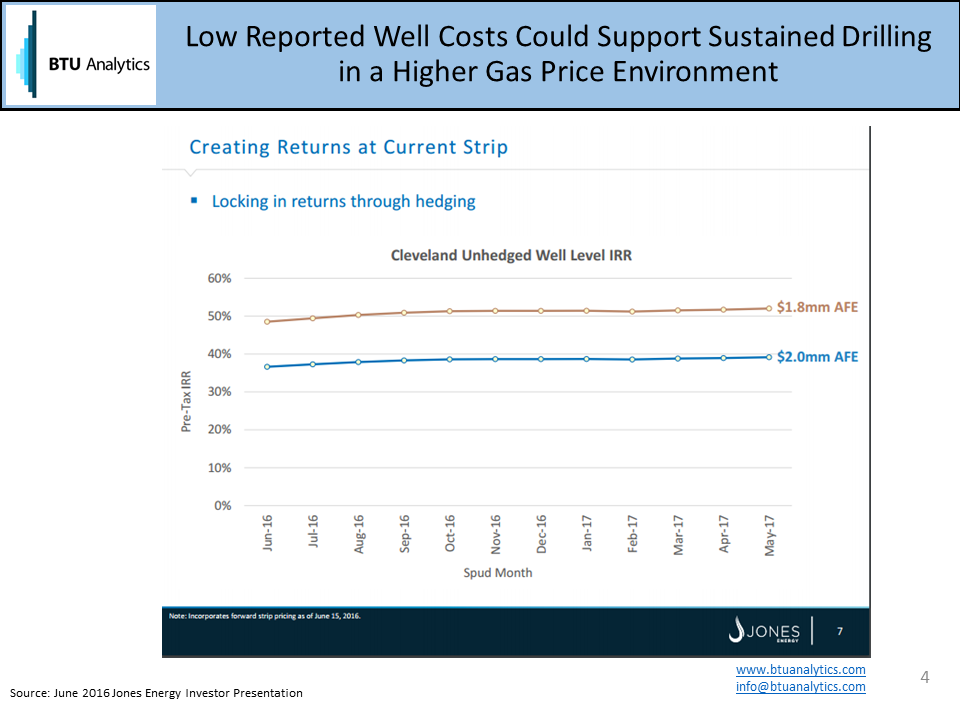

Furthermore, while this area does not boast the 10+ MMcf/d IP rates that many other gas areas are reporting, well costs being reported by Jones Energy show significantly lower D&C costs than are reported in other major shale basins, at less than$2.0 MM per well. Jones Energy, the lone public operator, reported in their June 2016 investor presentation that expected pre-tax IRRs are favorable and support continued investment based on the June 15, 2016 gas strip which averaged $3.48/MMBtu. If this is an indication of regional wellhead economics, then the Western Anadarko Basin could see an additional ramp up in activity if prices move above or stabilize near $3.50/MMBtu.