As the market’s attention is laser focused on the latest updates from the Permian, STACK/SCOOP, Haynesville and Utica, one might occasionally wonder what happened to some of the other plays across the US that were once buzzed about. Today, we take a look back at two of the ‘has beens’, the Barnett and Mississippi Lime, to think about what made these plays interesting to the market, why that interest has waned, and what market conditions would need to manifest to make them viable and valuable yet again.

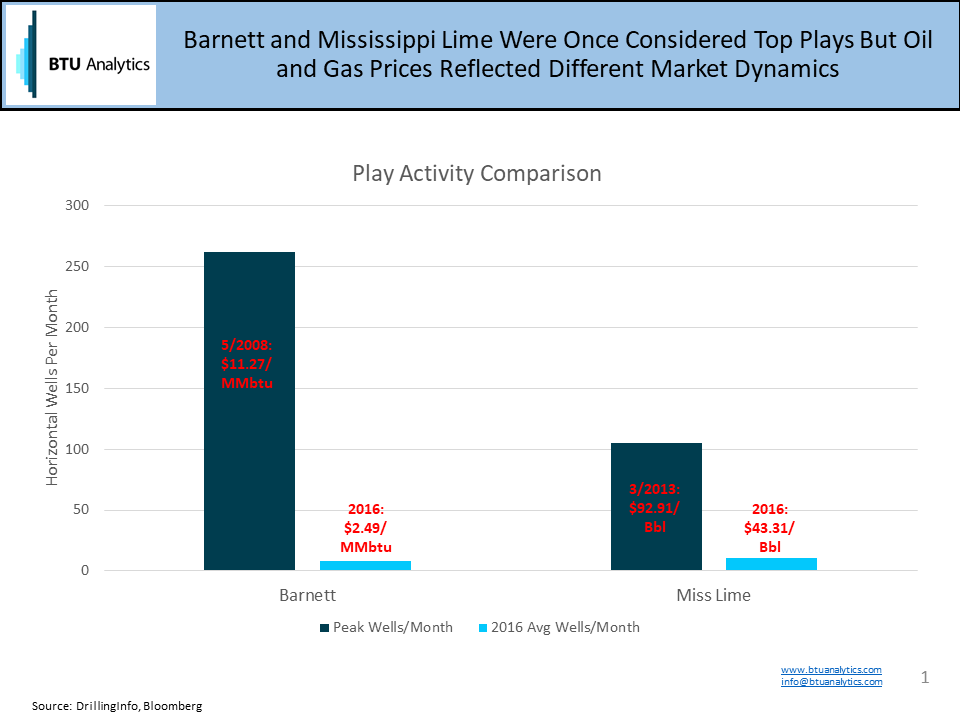

The Barnett is the granddaddy of US shale plays. It was discovered at a time when concerns about declining US production had prompted the development of LNG import terminals to the US. Supply fears had natural gas trading over $10/MMbtu, levels that are hard to fathom in today’s environment

Activity in the Barnett peaked in May of 2008 at 262 horizontal wells turned to sales that month. But the market found better rock that gave more bang per capex dollar, and soon the Fayetteville, Haynesville and Marcellus would overtake the Barnett as the plays commanding the market’s interest and investment.

The Mississippi Lime rose to prominence following the 2012 crash in natural gas pricing. The market wanted liquids growth, and while the Bakken was well established as the king of the onshore oil plays at the time, producers not in the Bakken were looking for liquids plays and to diversify away from natural gas, and the Mississippi Lime fit the bill for a number of independents.

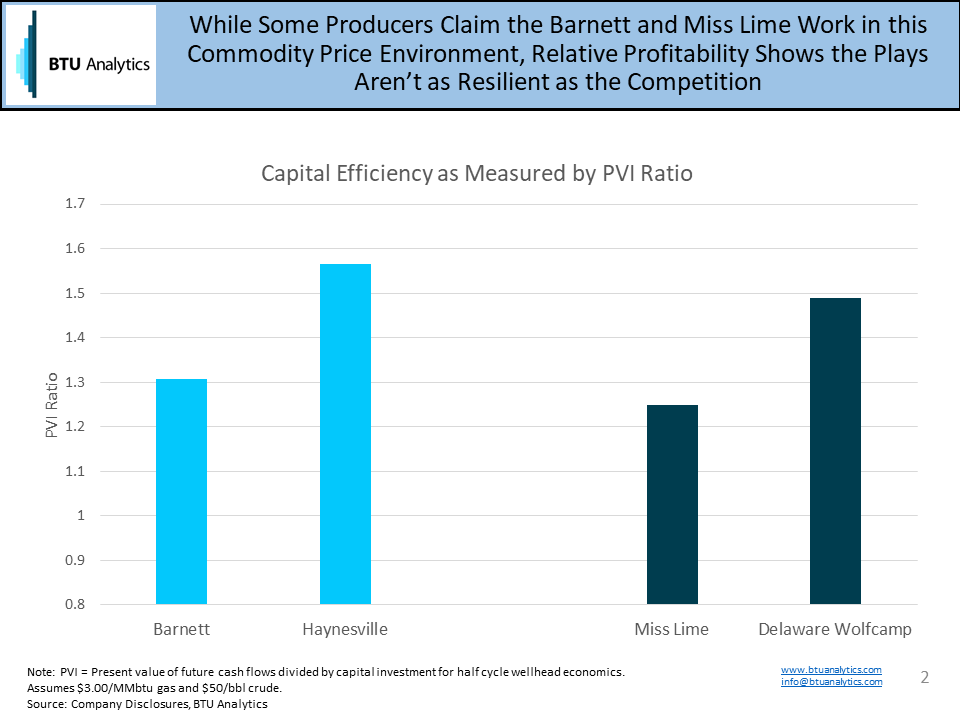

But just as the Barnett was eclipsed by other plays where faster production growth was possible with better capital efficiency, the Mississippi Lime lost status as technological improvements in other US oil shale plays lowered the marginal cost to produce and the crude price crash of 2014 forced one of the play’s largest producers into bankruptcy and caused others to retrench and focus their efforts on other plays within their portfolios with lower costs. The chart below compares the capital efficiency of the Barnett and Miss Lime to a few of today’s hot plays.

But what market conditions could emerge that would make these plays valuable once again? On a macro level, the most basic answer is significantly higher demand for natural gas or crude oil. Higher levels of demand would cause US producers to work through lower cost inventory more quickly, and bring higher cost plays back into the US supply picture. Another potential game changer would be the discovery of a new play within the same geography. Northeast producers have pointed out that Upper Devonian development doesn’t make much sense in isolation, but that in some cases co-development of that horizon in conjunction with the Marcellus and/or Utica make it feasible.

Will the Barnett and Miss Lime again find their day in the sun? Not likely anytime soon. But it’s worth remembering just how quickly changes in technology upended the US and now global markets for crude and natural gas, and how the hot plays of today might be seen in a different light a few years from now.