It can be considered ironic that some of the best natural gas acreage in the country just happens to be the very same acreage that is plagued by a lack of takeaway capacity. Perhaps some would consider it more tragic than ironic. Nevertheless, we at BTU Analytics have taken quite a bit of time to analyze this region to figure out what exactly is going on up there and, more importantly, what will happen in the future. Previously, we’ve outlined some relief that will emerge from power plants in the area, as well as the challenges facing greenfield projects in the region. So where does that leave Northeast Pennsylvania? Are there other hopes to liberate Marcellus gas trapped behind the pipe? Let’s look away from the ‘usual’ suspects and look at some other potential pipes that can provide relief.

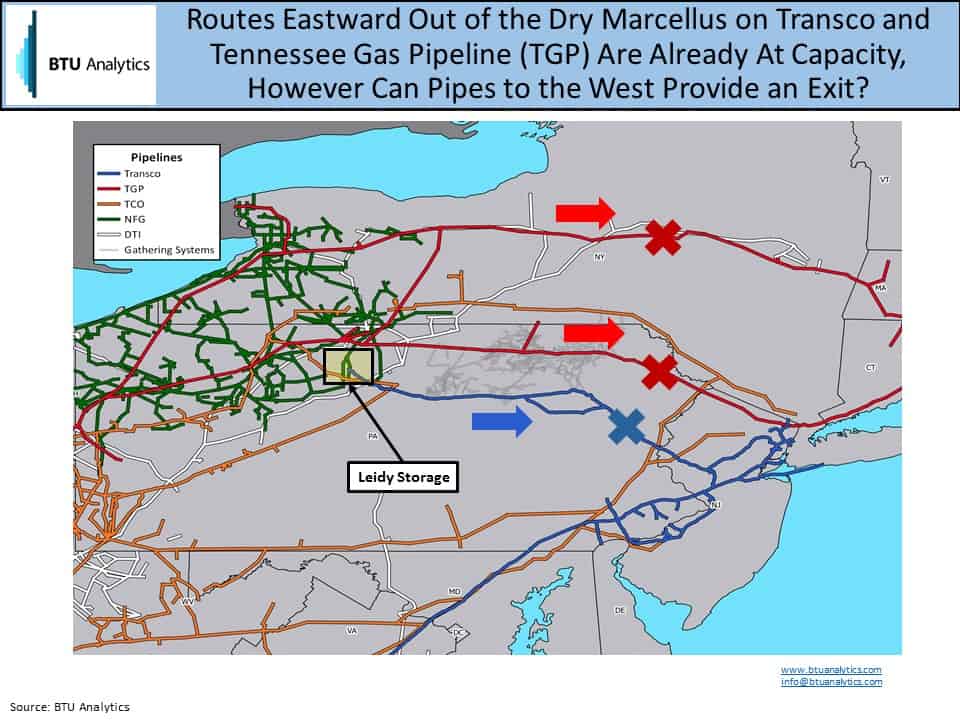

As shown below, the two major pipes in the vicinity of the Dry Marcellus’ sweet spot are Tennessee Gas Pipeline (TGP) and Transco. Unfortunately, these two routes out of the area are congested especially during peak winter demand periods. However, the question I am more interested in today is what are the prospects in moving gas west out of Northeast PA?

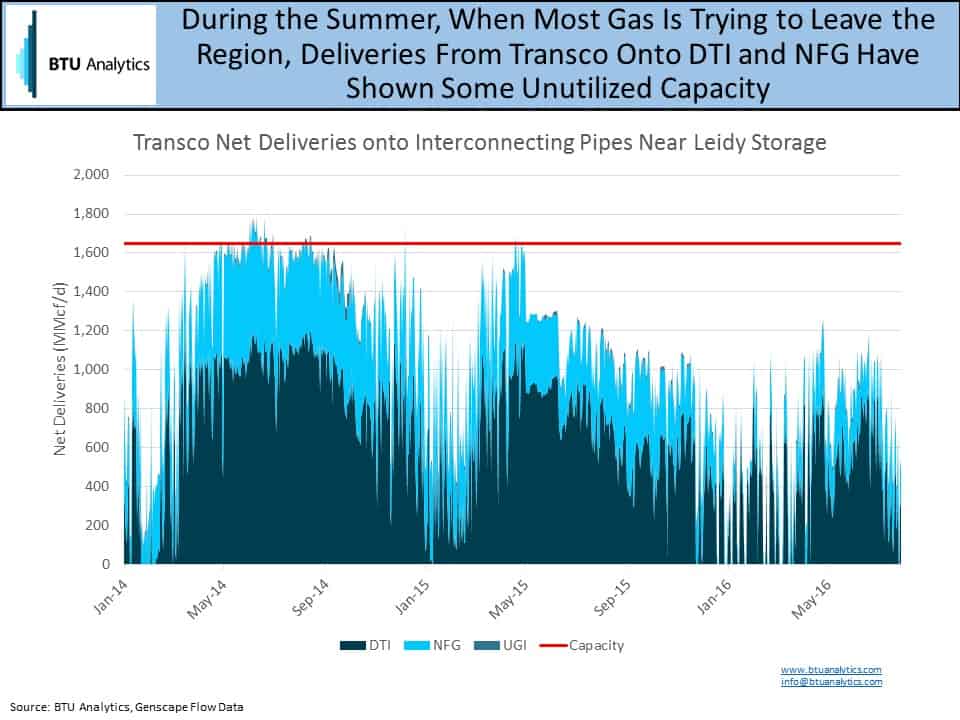

Dominion (DTI) and National Fuel Gas (NFG) pipelines, shown above, provide the best possibility to move westward out of Northeast PA via interconnections with TGP and the Leidy Storage Hub at the western end of Transco’s Leidy Line. First let’s look at these interconnections off of Transco. The graphic below shows net deliveries to interconnecting pipes from Transco.

As we can see, there was about 500 MMcf/d of unused capacity during this summer when most gas is trying to leave the region. Clearly there is some wiggle room off of Transco to push volumes to levels we have seen historically.

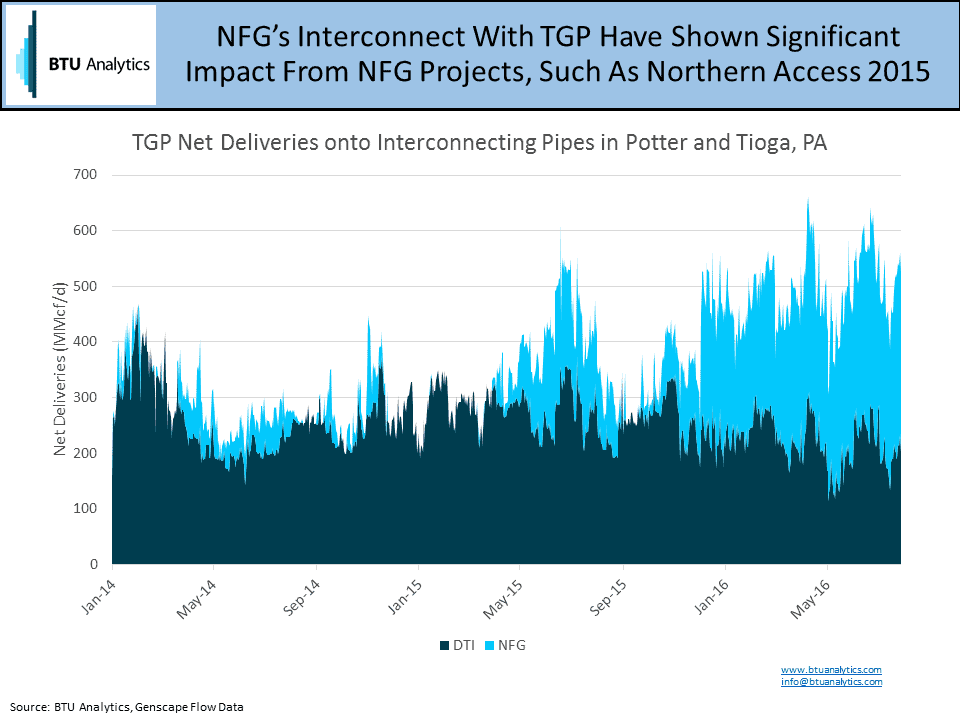

Turning to TGP and its interconnects in Northeastern PA show a bit of a different story. The graphic below shows net deliveries onto DTI and NFG from TGP.

Here we can see the impact of some of NFG’s recent projects that totaled about 400 MMcf/d of new capacity, including its Northern Access 2015 that allowed more gas to be pushed northward on their system towards Canada. Meanwhile, Dominion volumes off of TGP have been more or less flat with some minor declines recently. Maybe when NFG’s delayed, 500 MMcf/d Northern Access 2016 project comes online next year, we will see some additional volumes flow off of TGP. Until then, however, TGP’s interconnects in the region sit near historic highs, suggesting they are at capacity.

So on the whole, thanks mostly to Transco, there does seem to be some additional capacity out of the region. Why does this capacity go unused right now? The answer lies in Transco Leidy and Dominion South pricing, which are trading within pennies of each other. Why pay increased transport costs to get your gas to other markets when you can stay home and collect a similar price? Now, if takeaway out of Western Pennsylvania develops faster than out of Northeastern Pennsylvania and Dominion South strengthens relative to Leidy prices then we would expect that unused capacity to come into play. Until then, expect NFG, and the outlet it provides to Canada, to continue play an important role in getting gas out of Northeast Pennsylvania.

For more analysis of Marcellus and Utica flow dynamics, as well as infrastructure and basis forecasts, see our upcoming Northeast Gas Quarterly.