The conflict between Russia and Ukraine has highlighted a mutually dependent relationship between Europe and Russia. Russia provided approximately 40% of the gas consumed in Europe in 2021. Meanwhile, oil and gas sales accounted for 39% of Russia’s federal revenue in 2021. Europe purchased more Russian oil and gas than any other region, meaning oil and gas exports to Europe are an important source of income for the Russian federal government. In light of the emergence of conflict between Russia and Ukraine, Europe has begun urgently searching for a way out of its interdependent relationship with Russia and its petroleum. One potential solution that has been gaining a significant amount of steam amongst European lawmakers is the prospect of displacing Russian gas imports with imports from other sources in the form of LNG. However, Europe is unlikely to be able to completely move away from Russian imports for the foreseeable future without significant investment in LNG regasification capacity.

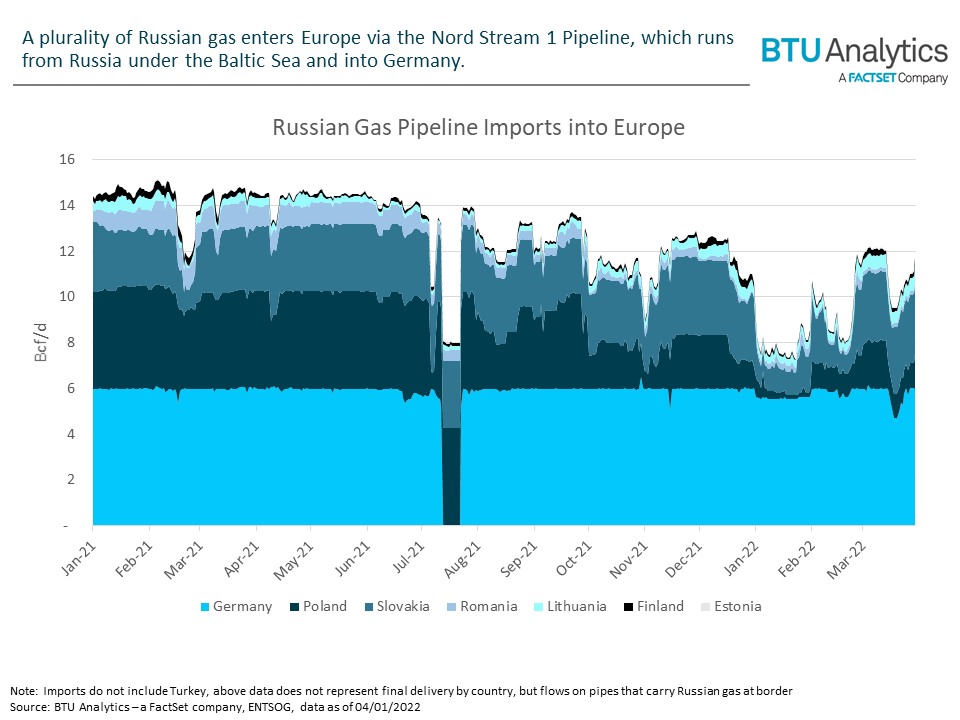

Most of the gas Russia supplies to Europe reaches the continent via pipeline; in 2021 only 6% of Russian gas bound for Europe reaches its destination via LNG tanker. Therefore, the primary challenge for European lawmakers will be to find alternative sources to Russian pipeline gas. The chart below shows Russian natural gas imports via pipeline into Europe by the countries through which the gas enters. In the first half of 2021, Russian gas imports via pipeline into Europe averaged 14.3 Bcf/d. In 2022, Europe has required as much as 12 bcf/d of Russian natural gas pipeline imports. This is the scale of the challenge facing European leaders moving forward, replacing 12 to 14 Bcf/d of gas, or approximately 40% of their daily gas consumption.

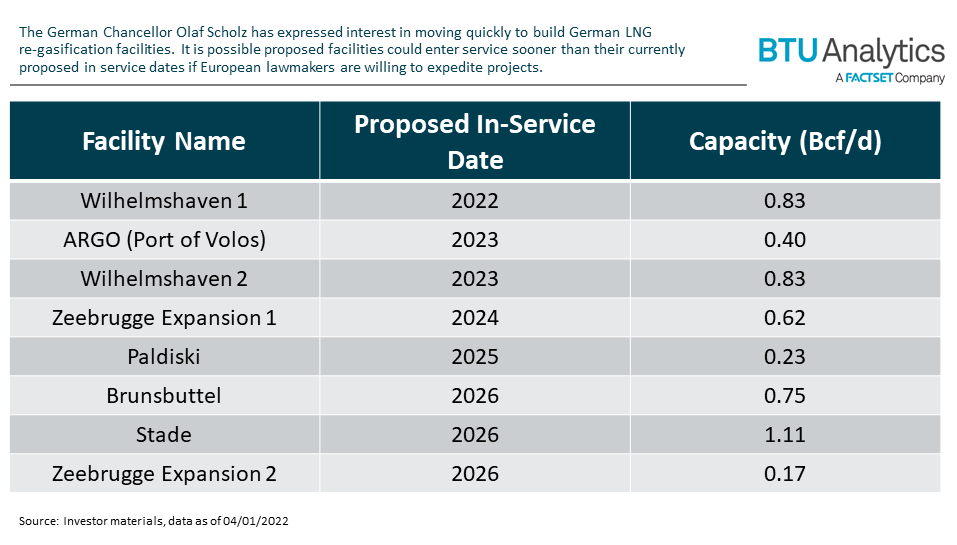

There has been a ground swell in support amongst European lawmakers to temper Europe’s reliance on Russian gas by connecting the continent to alternative gas producing regions using LNG import terminals. In addition to facilities that were already in the works, proposed import facilities that had previously been shelved or cancelled are are being revived all over Europe . The chart below lists some of the newly proposed and currently in the works projects. The chart is not exhaustive as there have been additional facilities revived or proposed since the conflict between Russia and Ukraine began. These additional facilities were omitted from our list due to the lack of detail surrounding their proposed in-service dates and capacities. Europe currently operates an existing fleet of re-gasification facilities with a combined capacity of approximately 22 Bcf/d.

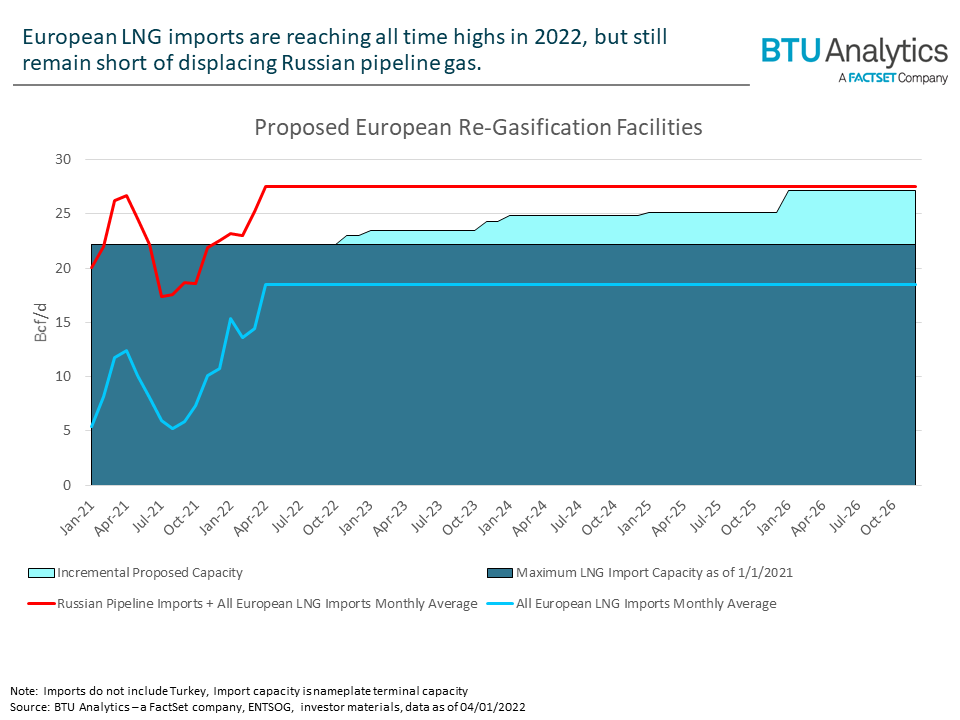

The chart below shows the capacity of existing European re-gasification facilities along with the capacities of currently proposed re-gas facilities. The chart also displays historic LNG imports at these terminals. The red line on the chart is the historic LNG imports at the existing European re-gas facilities plus gas imported on pipelines from Russia. This line functionally represents the amount of gas that would need to be imported at European re-gas facilities to replace Russian pipeline imports.

If Europe pursues LNG as the sole alternative source to Russian pipeline gas, Europe will need to increase the quantity of gas that it imports via LNG by approximately 9.04 Bcf/d relative to its max LNG imports in 2022. Additionally, Europe will need to increase its capacity to import and process LNG by at least 5 Bcf/d. If Europe operated its existing re-gas facilities at capacity, it could displace 4 Bcf/d of gas it currently imports from Russia immediately. However, for a variety of reasons including pipeline constraints, Europe is currently not capable of operating existing import terminals at 100% utilization. Will the newly proposed re-gas facilities cover the 5 Bcf/d of additional re-gas capacity that is needed for Europe to become independent of Russian gas supplies? Despite the large wave of re-gas facilities that have been proposed since the start of the Russia Ukraine conflict, Europe is likely still years away from displacing Russian pipeline gas as a major source. As the chart above shows, even if all the proposed facilities were built on time and all re-gas facilities in Europe were running at 100% utilization, Europe would still find itself approximately 0.5 Bcf/d short of being able to fully displace Russian pipeline gas in 2026.

Considering the fact that Europe has never ran its re-gas capacity near 100% utilization, it is likely that the current slate of proposed re-gas facilities (should they enter service) will not run at 100% capacity. Thus, in order to fully displace Russian pipeline gas via LNG imports, Europe will likely be required to propose and construct facilities beyond what is currently on the table or need to reduce the demand for natural gas significantly in that timeframe. Despite the current enthusiasm for displacement of Russian imports, Europe is unlikely to be able to completely separate from Russia until at least 2026 without a coordinated financial and regulatory effort to build new regasification capacity in Europe.