In 2013, Mexico initiated steps to reform the state-run oil and gas monopoly to allow foreign entities to explore for resources. Last month, two separate discoveries in the Mexican Gulf of Mexico (‘GOM’) were announced with a combined estimated total resource of 2.4-3.0 billion barrels of oil in place, and production could start as early as 2019 (Talos Energy and ENI). In response, Mexican regulators delayed the next round of lease auctions by one month to January 2018, likely to let the successful finds percolate in the market.

These finds could impact WTI pricing if the projects produce material incremental light oil in the Gulf; similarly, Henry Hub prices could be impacted if the development plans don’t include reinjecting associated gas. What is more important for natural gas, however, is what comes out of the January auction. The next round of bidding is comprised of 30 sections totaling over 27,000 square miles (about 10% bigger than West Virginia). The proposed locations include known natural gas-rich areas.

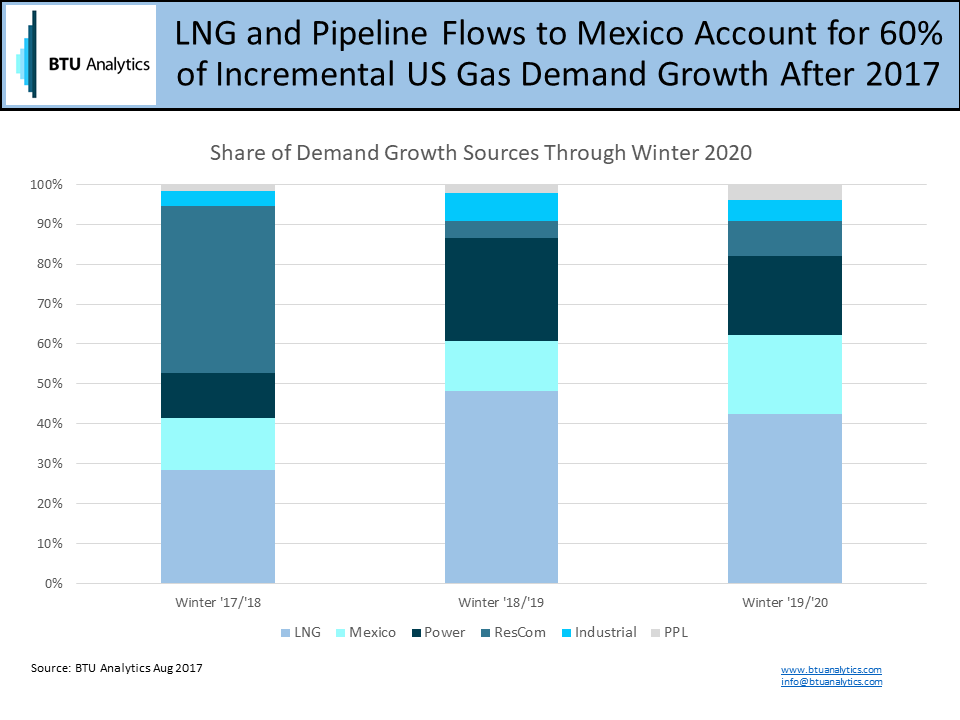

Demand from Mexico is expected to be a significant portion of incremental natural gas demand growth in coming years. BTU Analytics is forecasting that after the 2017/2018 winter, about 60% of incremental demand growth will come from LNG and Mexican pipeline exports through 2020.

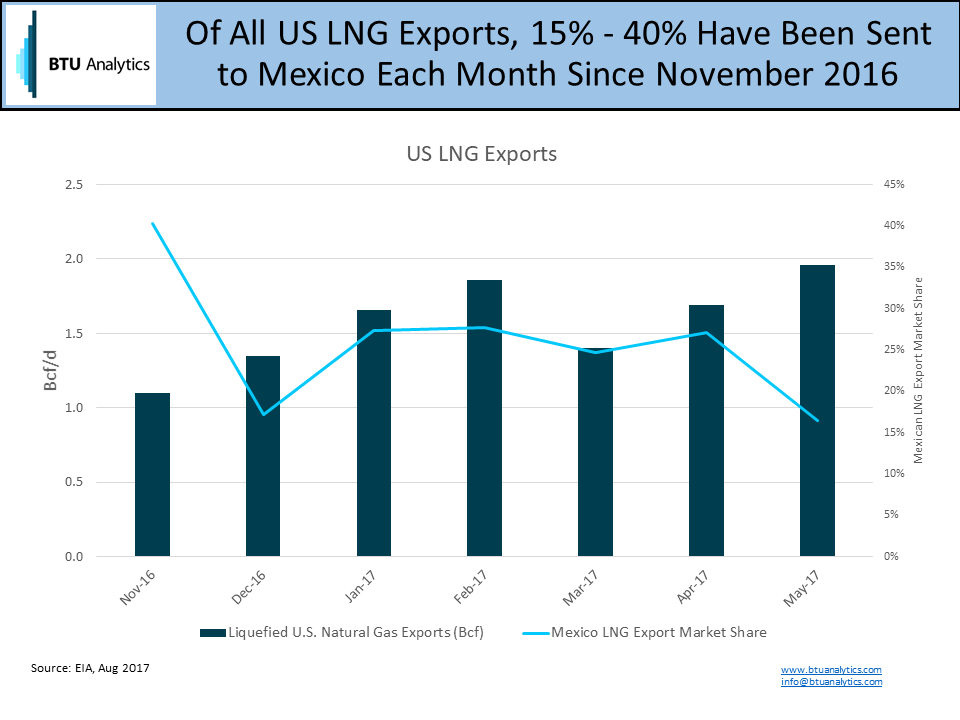

Even within LNG exports, Mexico is an important market as it has comprised 15%-40% of US monthly LNG exports since November.

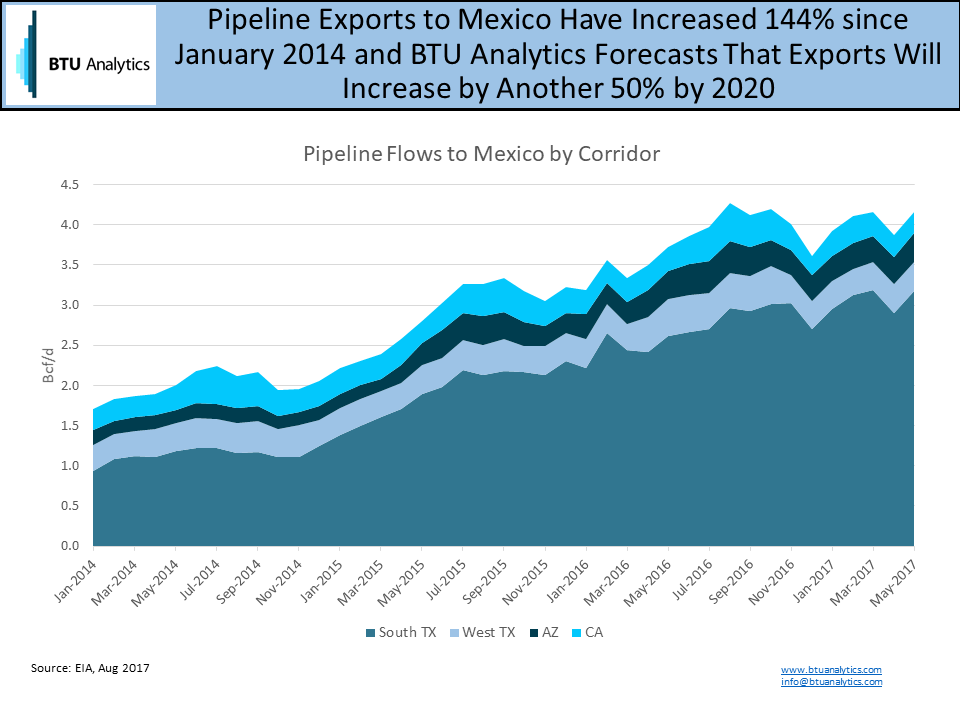

Most pipeline exports to Mexico are in close proximity to the Gulf, and many of the population-dense areas are along Mexico’s eastern shore, making resources in the gulf geographically convenient to satisfy demand.

If US producers are counting on strong demand out of Mexico to buoy the demand side of the market, stronger domestic Mexican production will only apply more pressure to Henry Hub. If the Mexican GOM resources parallel the historically rich US GOM, one could jump to the conclusion that WTI and Henry Hub should already be seeing downward pressure. The problem with that conclusion, however, is the long investment cycles for offshore projects, relatively unknown resource potential in unexplored acreage, and high government profit allocations.

Following ENI’s offshore discovery, they announced that they are fast-tracking the project with a preliminary estimated start-up in early 2019. Even fast-tracked offshore project cycles from discovery to first production are measured in years, whereas discovery to first production in shale plays can often be measured in months.

The long cycles, combined with unknown future outcomes from unexplored acreage, make timing and economic feasibility quite uncertain. The incentives for foreign entities are complicated by the government’s profit share. For example, the Mexican government will receive approximately 70 percent of the profit share from the Talos Energy discovery.

The GOM has been flying under the radar amidst the shale boom, but even the US GOM is expected to grow by over 300 Mb/d through the end of the decade. If the relatively untapped Mexican blocks become productive and economic, thereby attracting investment dollars from global producers, there are plenty of reasons to pay attention to how that can impact the markets in the coming years. For more information on the domino effect that Mexican demand has on pipeline flows, production, and pricing in the US, request a sample of the Henry Hub Outlook today.