US LNG exports have not only provided an important source of incremental demand for the domestic natural gas market, but those exports, along with other sources of growing global LNG supply, have begun to disrupt traditional seaborne flows of gas. As the LNG spot market develops and the share of contracts without fixed destination clauses grows, a fight for market share is likely to ensue. So, how will US LNG fare in an increasingly congested global market?

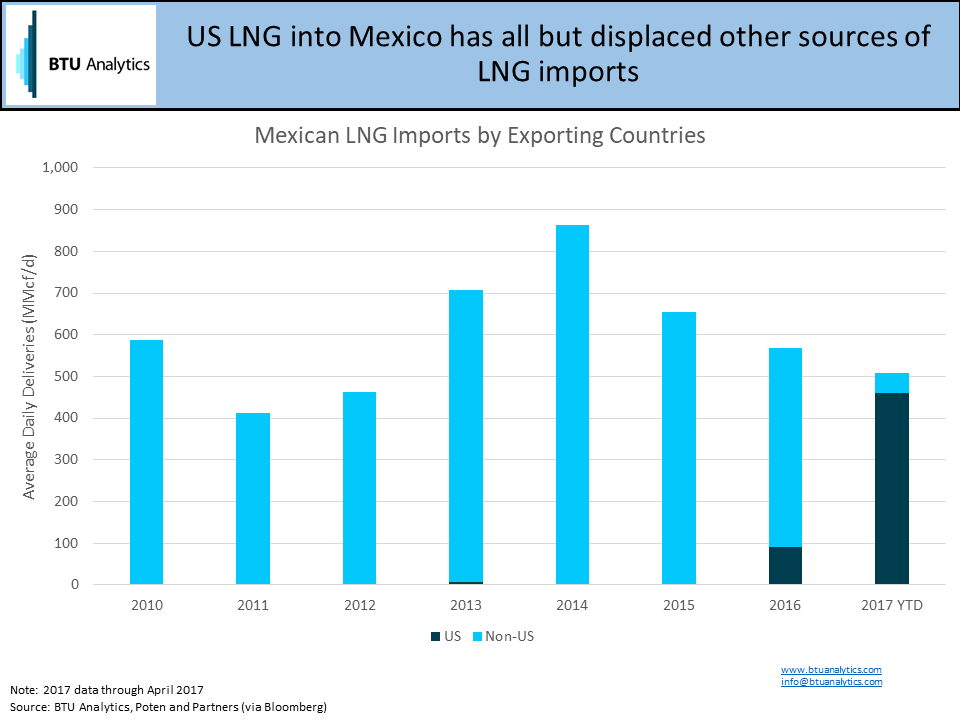

One market that saw major changes in supply over the last year is Mexico. Over the last five years, Mexico has imported an average of 600 MMcf/d of LNG to meet its demand. However, the sources of these imports have changed dramatically, specifically over the past year. The graphic below shows Mexico’s LNG suppliers over time with the US taking a larger portion of total Mexican LNG import market share, virtually displacing all other sources of cargoes.

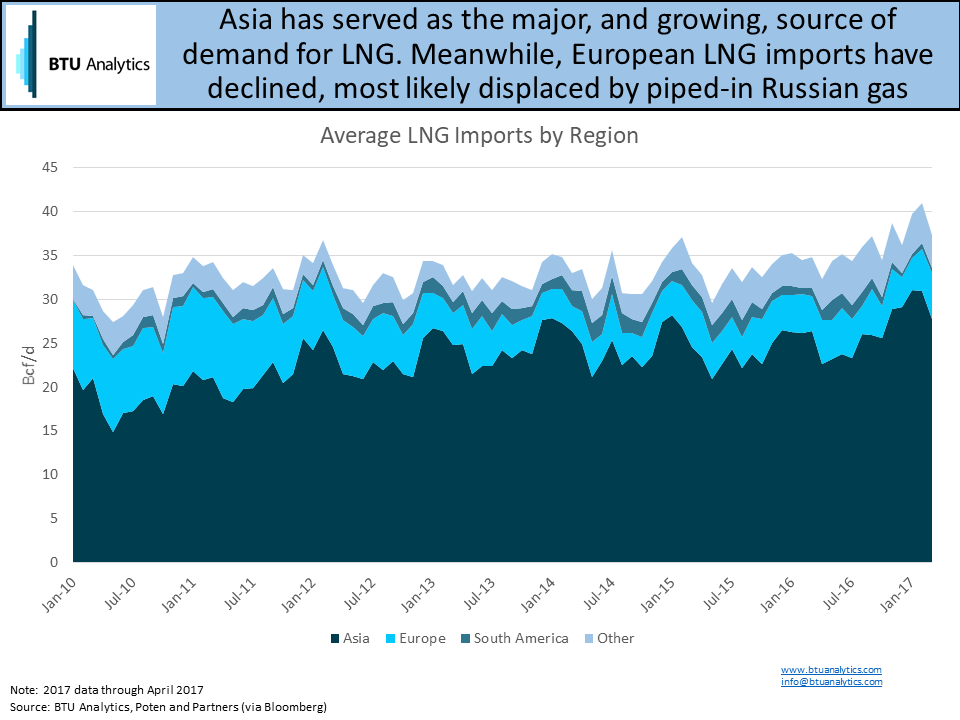

This change is occurring close to home and leaves us wondering if US LNG will have the same effect in other parts of the world? The US is not the only country bringing on new LNG terminals and adding incremental cargoes into the market. Australia, Malaysia and Russia, among others, have also announced LNG export projects with in-service dates in the next few years. Asia and Europe are often cited as the markets that are likely to soak up this impending incremental supply. Not only are they currently the two largest markets, as the graphic below shows, but they also hold the greatest potential for growth.

Historically, Asia has proven to be the largest source of imports, reaching 31 Bcf/d in winter 2017. European imports have dwindled from an average of 7.9 Bcf/d in 2010 to 4.3 Bcf/d in 2016. However, European declines are not necessarily directly attributable to declines in demand. While, according to the 2016 BP Statistical Review, European gas consumption has been on the decline since peaking in 2008, Europe also received much of its supply from piped-in Russian gas, which might have squeezed out some LNG imports over the past few years. This means that, if made economic, LNG imports could retake market share back from Russian gas.

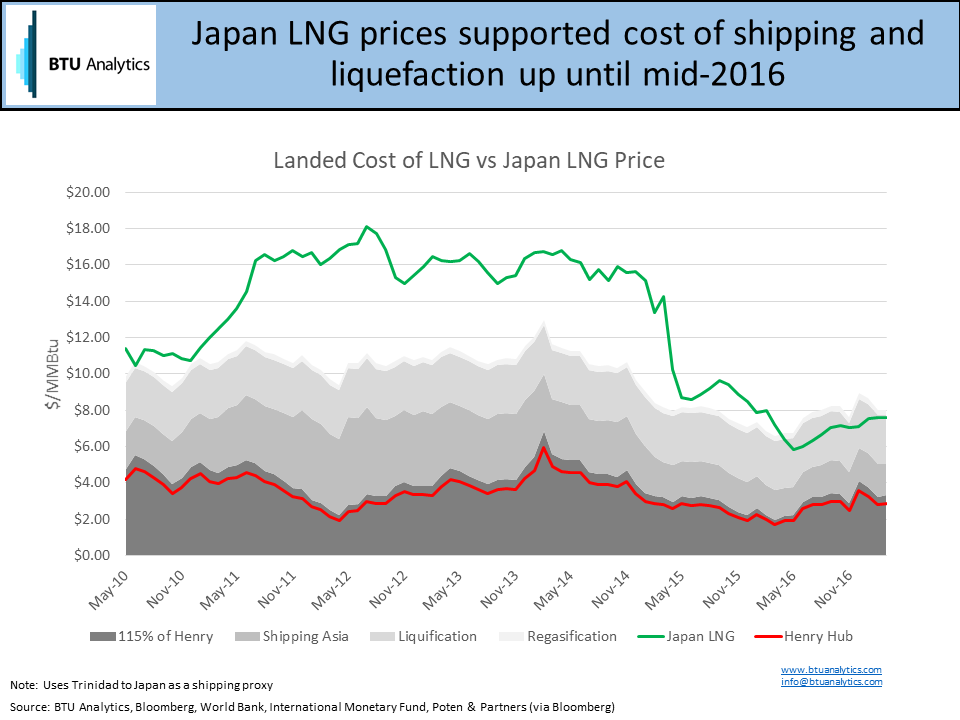

Assuming that Asia will continue to be a large source of demand for LNG, will US LNG be able to compete in the region? To answer this, we must look at how economic US LNG cargoes would be entering the region (in this case Japan).

To be incentivized to ship to Asia, Japanese LNG prices need to be greater than the variable costs to ship cargo. Let’s assume the cost of the gas (115% of Henry Hub) and shipping costs are variable. That would mean over the past year it would have been economic to send cargoes to Asia. However, if incremental demand in the region is not able to keep up with supply, Japanese LNG prices would have to fall below variable costs to disincentivize imports into the region. While the US gas market is set to enter a time of potential oversupply and depressed Henry Hub prices, transport costs into the region could become prohibitive in a liquid spot market leaving US cargoes heading back to sea in search of a destination closer to home. To see how LNG exports will affect US supply and demand dynamics and Henry Hub pricing over the next five years, see our latest publication of our Henry Hub Outlook.