As COVID-19 has swept through North America, attention has turned to natural gas supply and demand balances as the crude oil market has crashed. Fortunately for natural gas producers, the fuel they produce is not a transportation fuel, providing some shelter from the storm. In 2019, natural gas demand as tracked in BTU Analytics’ Henry Hub Outlook was made up by power at 31.3 Bcf/d or 34%, res/com at 23.7 Bcf/d or 26%, industrial at 23.3 Bcf/d or 26%, Mexico exports at 6.8 Bcf/d or 8% and LNG at 5.6 Bcf/d or 6%. So far, power burn and res/com gas demand have remained relatively resilient during the COVID shelter-in-place period. When looking at industrial natural gas demand, impacts from a drop in ethanol and methanol have had a large impact on the pipeline sample as gasoline demand has plummeted. Analyzing industrial natural gas demand is a challenge as the interstate pipeline sample size is small relative to total actual industrial demand. This commentary will look at the industrial demand reaction to COVID, the potential for skewed samples, and what is in store for the remainder of 2020.

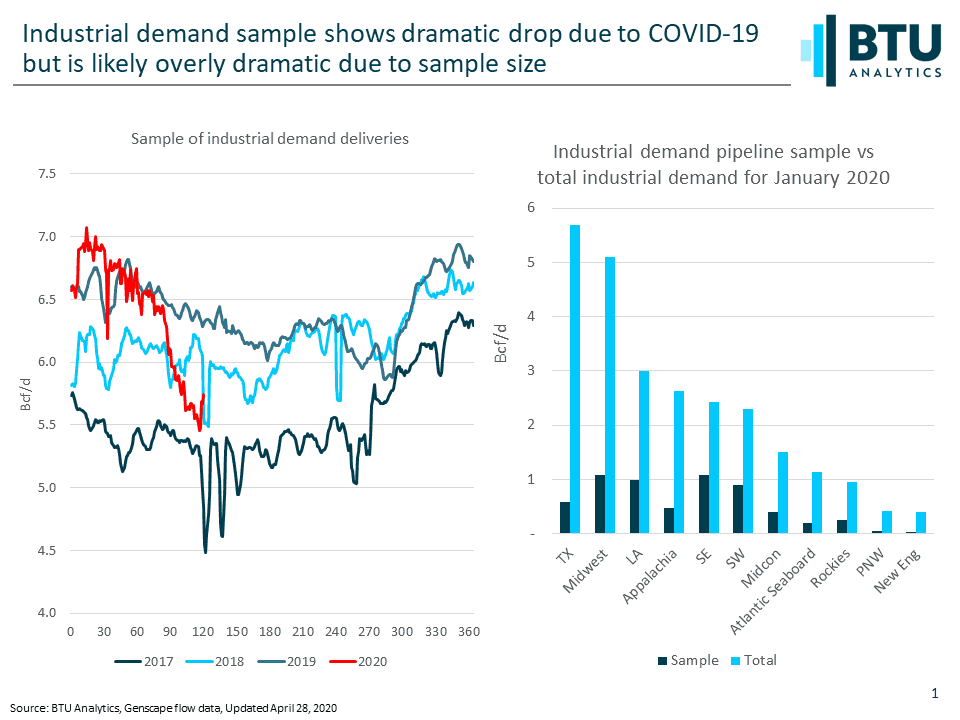

When looking at the US industrial interstate pipeline sample, the impact of COVID looks precipitous as demand has dropped by more than 15% from 6.5 Bcf/d in February to 5.5 Bcf/d in April as shown above on left. Analyzing industrial natural gas demand is challenging considering in January 2020 (pre-COVID) the pipeline sample was 7.0 Bcf/d compared to total industrial demand of 22.1 Bcf/d. As shown above right, key regions such as Texas, the Midwest, and Louisiana suffer from small sample sizes relative to total industrial consumption. As most of the US refining and petrochemical demand is located in Texas and Louisiana off intrastate pipelines, this means much of this demand is missed in the interstate sample.

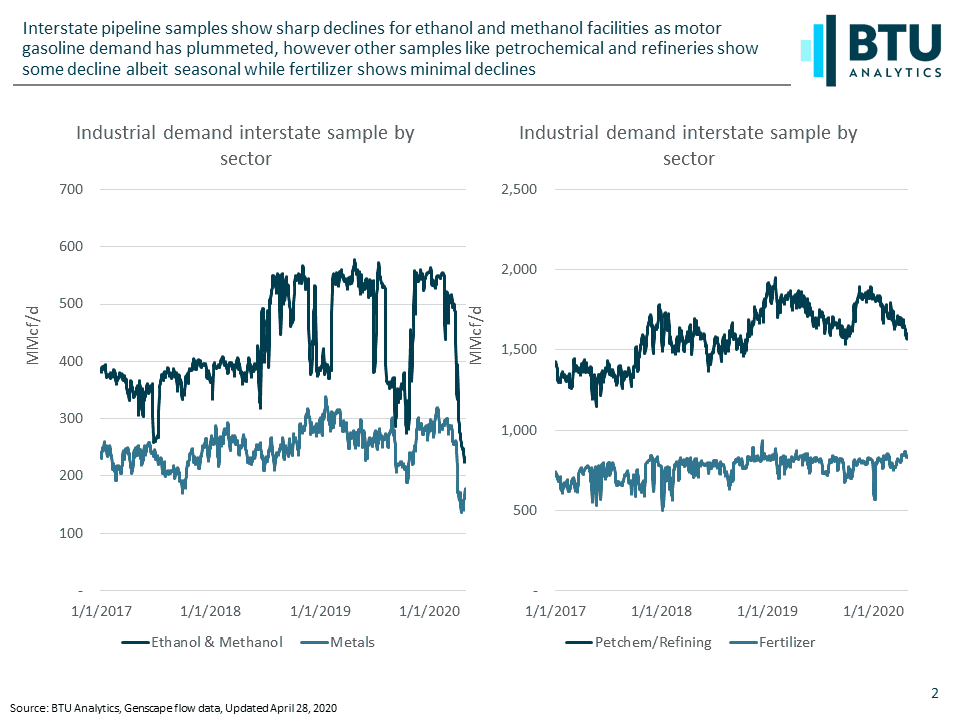

When looking at components of the industrial sample we can see steep drops in ethanol and methanol and steel as seen above left. The steep drop in ethanol and methanol is the result of the COVID driven decline in motor gasoline demand. However, ethanol has an oversized impact on the industrial demand sample overall, since most of these meters are in Midwest states that have better connectivity to interstate pipelines. Similarly, some of the largest interstate pipeline steel meters are in Appalachia and the Southeast regions, potentially skewing the sample. Other components of industrial demand have held steady as shown above on right. Petrochemical and refining have seen declines, but seasonal declines do occur at this time of year as refinery maintenance season starts. Also, refinery curtailments due to COVID may not have as much impact on natural gas consumption as refineries still require heat and power to operate even at reduced utilization rates. Meanwhile, the fertilizer sample has remained resilient. Other industrial samples that were looked at for this commentary included food processing, paper and cement which have shown small declines relative to this same time last year.

BTU Analytics does expect to see industrial demand decline in 2020 by about 2.0 Bcf/d at 21.4 Bcf/d due to a COVID driven recession. But as the COVID situation remains dynamic, the scale and the length of the recession may require more demand revisions – see previous commentary on industrial demand and recession impacts. To follow BTU Analytics’ forecast for natural gas demand components including power, res/com, industrial, Mexico and LNG, request more information on BTU Analytics’ Henry Hub Outlook.