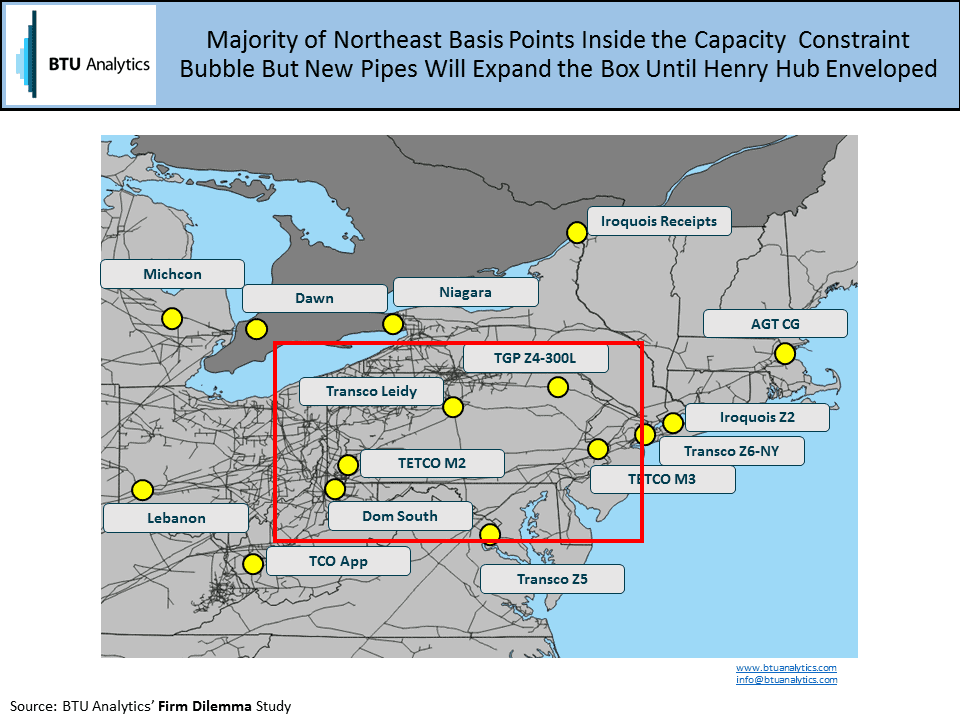

Lebanon, Ohio and its surrounding area, dubbed the Lebanon Hub, once occupied the role as a waypoint for gas entering the Northeast, but the tide of natural gas has reversed. As we discussed in the recently published Firm Dilemma gas market study, points in the Northeast can be thought of either inside or outside of the over-supplied capacity constrained box. For example, the box below shows points that suffer from over supply and lack of capacity to get to a demand market resulting in very weak realized well head pricing. Now a wave of Northeast infrastructure projects may push the box out to include the Lebanon Hub.

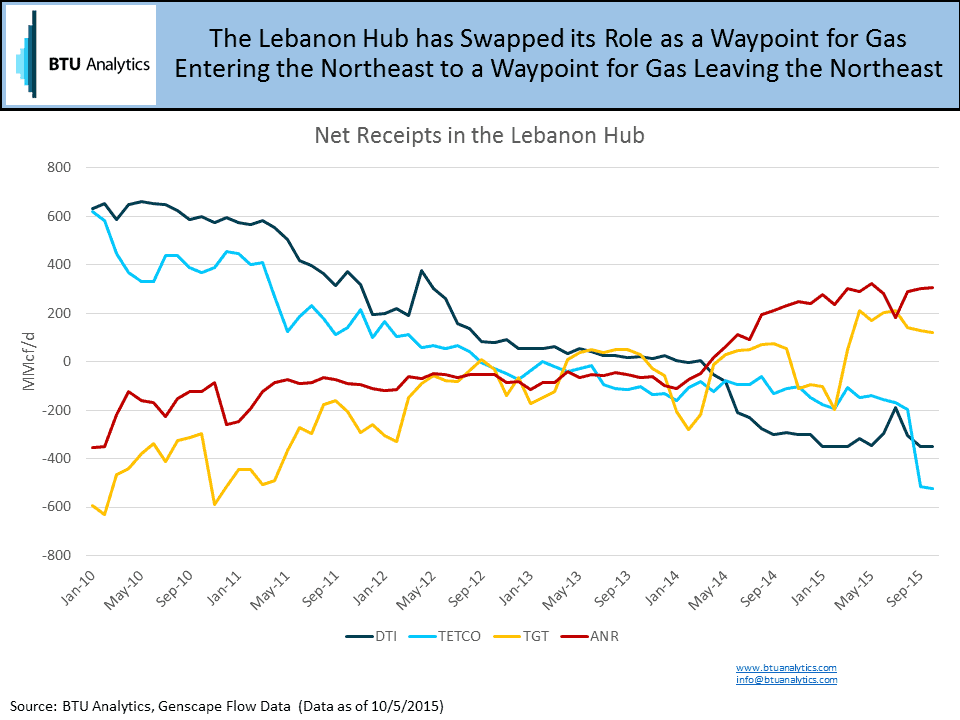

For perspective, take a look at the following time series. This graphic shows the net receipts onto four of the major pipes in Lebanon since 2010. Here, negative volumes represent deliveries into Lebanon Hub, while positive volumes represent receipts (or gas being taken away from the Hub). Before the shale revolution, ANR, TGT, and others would carry gas from Texas, Louisiana, and Oklahoma up to Lebanon, where they would deliver to pipes such as TETCO and Dominion (DTI) that would then disperse the gas to markets in the Northeast. Now the roles of these pipes in Lebanon have virtually swapped, meaning DTI and TETCO are now flooded with Marcellus and Utica gas and deliver gas to Lebanon Hub while TGT and ANR now use Lebanon Hub as a supply source for reversal projects to the Southeast.

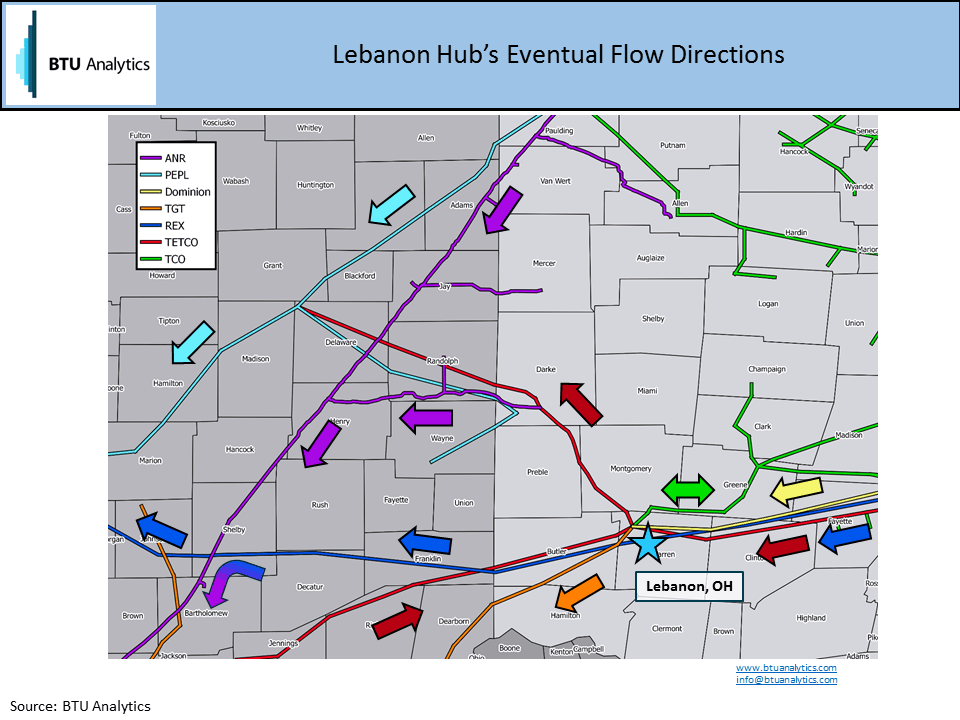

However, these four pipes aren’t the only ones in Lebanon. The schematic below adds Panhandle, REX, and Columbia gas into the mix to account for all major longhaul pipes involved in Lebanon, with the arrows indicating eventual flow direction. While many of these pipes have already begun to flow east to west, more east to west capacity is still to come such as, REX with its Zone 3 Capacity Enhancement project (Q4 2016) and TGT Ohio Louisiana Connector project (Q2 2016), others will be phasing in through 2018. In all, accounting for an incremental increase of about 3.7 Bcf/d of gas.

In addition to those projects, Rover (not shown) will have 2.8 Bcf/d of interconnecting capacity with ANR and Panhandle at interconnects located north of Lebanon Hub. Panhandle already has a project in the works to push 750 MMcf/d of that gas south to the Gulf via Trunkline, while ANR has not yet disclosed the volume of gas it will backhaul from its Defiance, OH interconnect with Rover past the Lebanon Hub. All of this translates to more congestion in Lebanon.

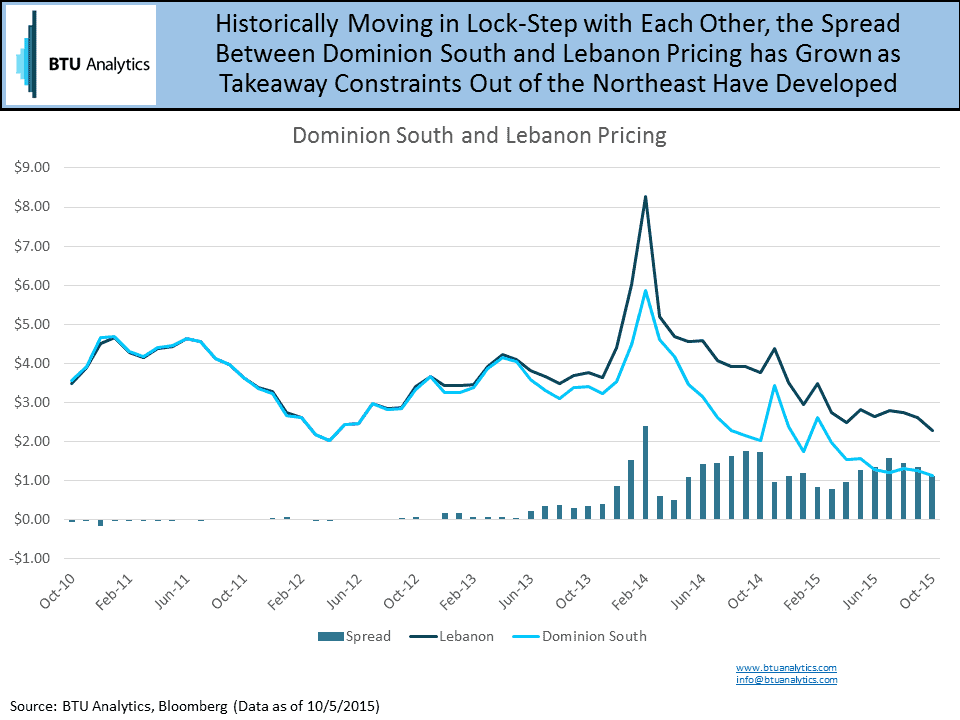

The last part of the equation to look at is price. How will prices react when as much as 5 Bcf/d of gas is flowing through Lebanon? Comparing Lebanon prices to Dominion South prices shows that historically, up until 2013, prices have moved in lock-step with each other with minimal spreads between the two. However, starting in 2013, with growing Marcellus production and limited takeaway capacity out of the region, they began to significantly diverge with the spread this year averaging $1.20.

As new takeaway capacity comes online and gas begins to flow unconstrained between the Northeast supply and Lebanon, expect those spreads to tighten as Lebanon Hub may soon fall inside the Northeast oversupply box. For more on Northeast infrastructure, regional pricing, and flow dynamics request a free sample of BTU Analytics’ new Northeast Quarterly product.