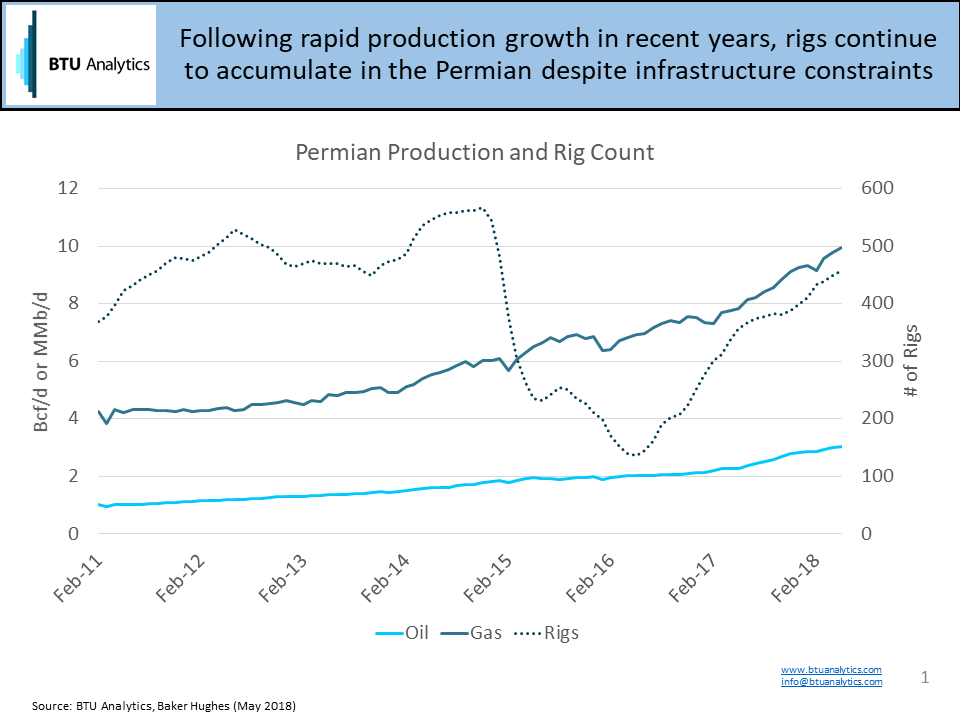

Our client base is comprised of many different energy industry stakeholders spread across the globe, but over the last few months, almost every conversation is eventually related to what’s going on in West Texas, especially with both oil and gas prices blowing out. Rig counts continue to rise in the Permian, adding momentum to already rapid production growth, and potentially putting more pressure on pricing into late 2018. March 2018 oil production is up over 30% versus 2017 with gas production up about 20%, and last week saw the highest rig count since January 2015.

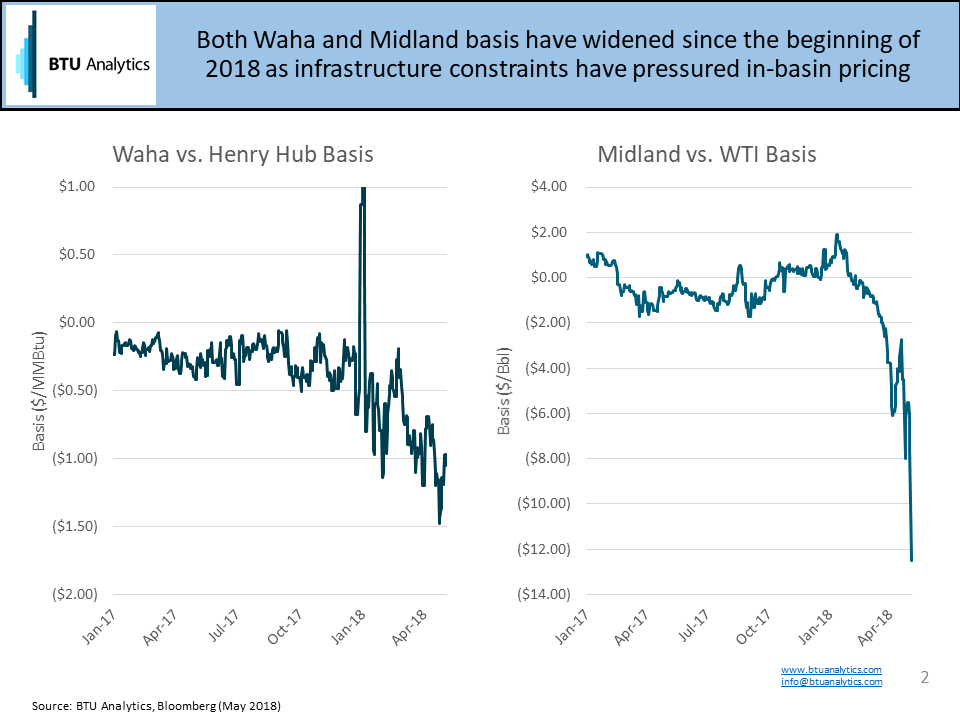

With production at record levels and more drilling on the way, much of the focus has turned to infrastructure development to transport volumes to demand markets, primarily the Gulf Coast. The recent blowouts in Permian pricing highlight the in-basin constraints for both oil and gas, with the Midland vs. WTI differential and Waha vs. Henry Hub basis widening, particularly over the last several weeks.

How Low Can Waha Go?

The combination of rising production and accelerating activity has resulted in low cash prices and weak forward curves for in-basin pricing for oil and gas. For gas markets specifically, until infrastructure constraints are relieved, Waha could get really weak, potentially going to zero or even negative, as the Permian story evolves from a displacement story to a physical capacity story. Economics in the Permian are dictated by liquids pricing, and with nearly $70 WTI, producers will continue to bring associated gas online without much consideration to gas prices. That can continue until the pipes are physically full, at which point oil production will be inhibited by gas takeaway constraints, and BTU Analytics expects that to happen later this year.

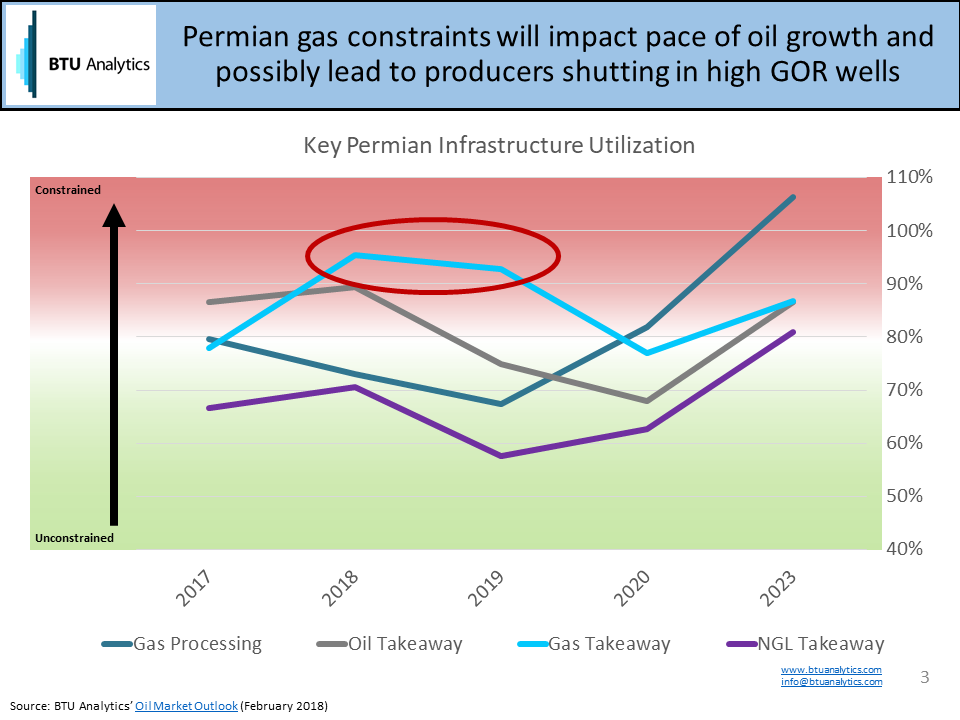

The chart below shows BTU Analytics’ views on infrastructure takeaway out of the Permian, and while oil takeaway utilizations are expected to be high in 2018, gas pipelines are expected to be nearly full until pipeline projects come online in 2019, which could lead to producers altering production strategies and/or shutting in wells that produce mostly gas.

Temporary Relief on the Way

Infrastructure constraints are highly relevant given accelerating activity and already weak pricing, but with Gulf Coast Express on the way, and several other projects being announced, such as recommissioning Old Ocean Pipeline alongside a North Texas Pipeline expansion, relief could be on the way in the next 18 months. Unless more pipelines are announced soon, however, the Permian could be in the same situation after a couple of years. Check out the Upstream Outlook for our view on how this plays out over the next five years, and check out Part 2 of this blog next week where we will dive into upcoming Permian infrastructure projects and how that plays out given today’s level of activity.