Over the last few years, natural gas production and demand growth have been increasingly segregated geographically. Production growth has occurred outside of the Gulf Coast, mainly in Appalachia and the Permian, while most demand growth has been driven by LNG exports, almost exclusively based on the Gulf Coast. This dichotomy pushed the infrastructure bridging the Gulf Coast to the rest of the US to its limits in 2019, seen both in Permian and Northern Louisiana pricing. As Summer 2020 quickly approaches, nothing structurally has changed to improve this situation.

In a written report included in our recent Upstream Outlook, we quantified how this mild winter has put much of the gas market behind the eight ball for the coming year. With much of the market to be oversupplied this coming year, we outlined how much production we believe needs to be curtailed or deferred this summer and from where.

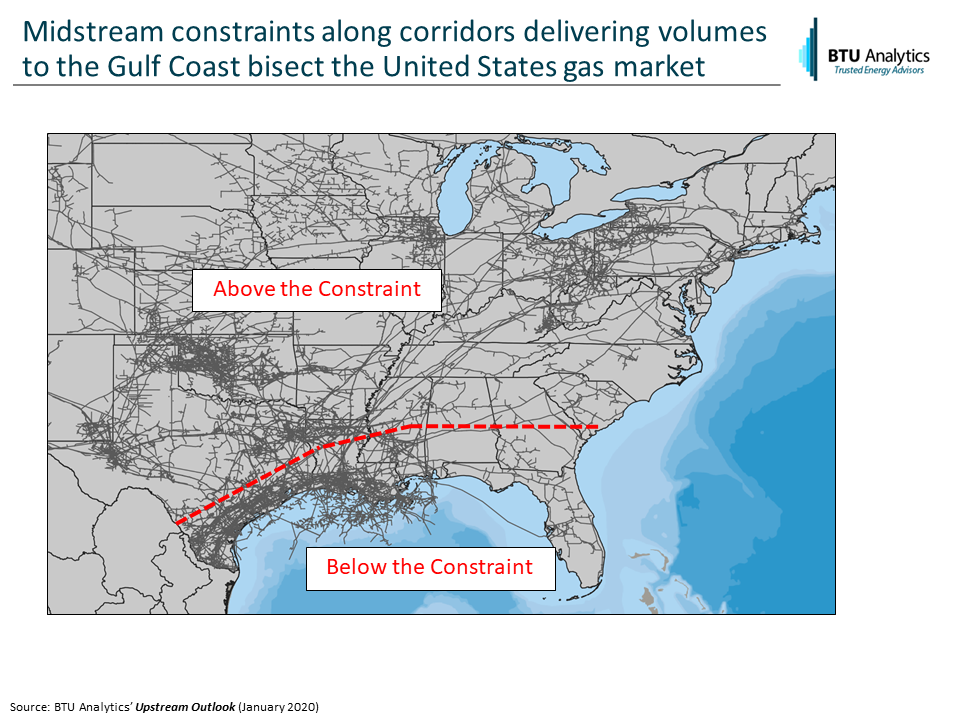

The map below highlights midstream issues that have divided the US gas market into two regions, the Gulf Coast (Below the Constraint) and everything else (Above the Constraint). The red dotted line represents approximate locations for constrained pipe, stretching from the Permian to Mid-Louisiana to the Atlantic Seaboard.

While BTU believes the Gulf Coast will be in short supply and that current forward pricing does not reflect the fundamental drivers of this summer’s NYMEX pricing, areas Above the Constraint will be long supply and excess gas will need to be taken out of the system.

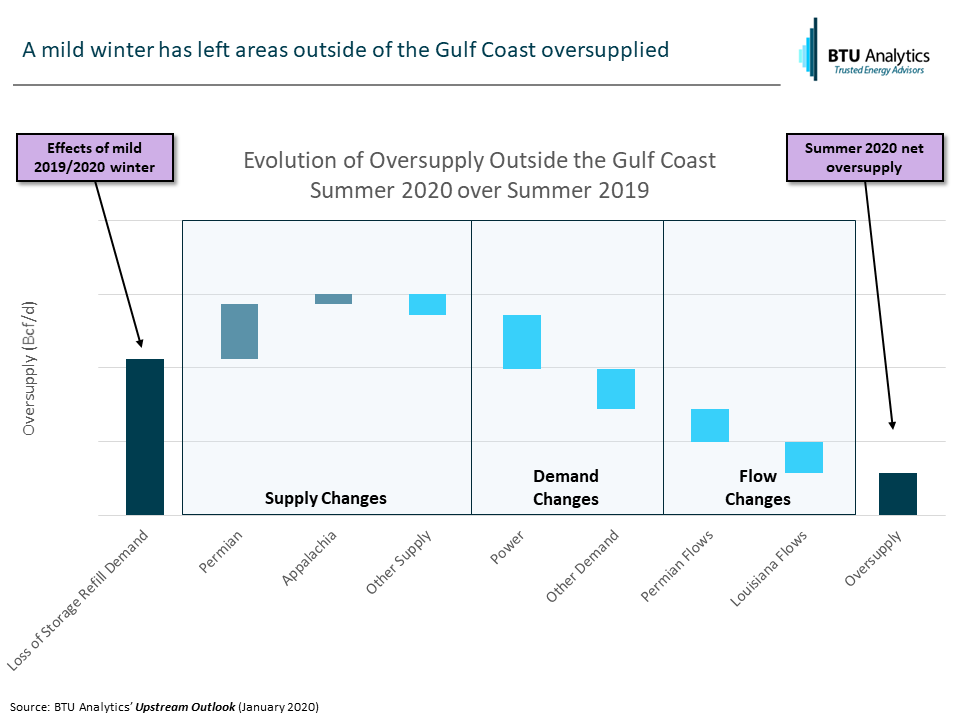

The magnitude of oversupply will have impacts everywhere from upstream production to downstream demand, so we defined that excess amount of gas that will need to be accounted for. The following graphic is a simplified and aggregated version of the graphic found in the Upstream Outlook, that begins with the effects of higher storage inventory on the left, takes into account summer-over-summer changes to production, demand, and infrastructure, to get us to the total amount of oversupply outside the Gulf Coast this coming summer.

Defining the oversupply is one thing, but how that oversupply will be corrected is what will be most impactful to the market. In our study, we then highlight the market mechanisms that will come into play, including curtailed (shut-in) production, deferred completions, and the magnitude and prices needed for coal-to-gas switching. Where and who can you expect to curtail production this summer and by how much? Get the most recent copy of our Upstream Outlook to best prepare for this coming summer’s difficult gas market.