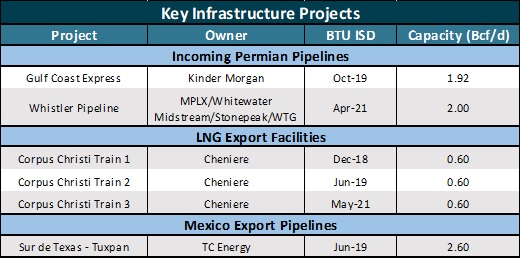

Last week, a joint venture project by MPLX, Whitewater Midstream, Stonepeak, and West Texas Gas announced a final investment decision to move forward with the Whistler Pipeline. The 2.0 Bcf/d pipeline will transport Permian gas to Agua Dulce with service scheduled to begin in 2021. The project will join Kinder Morgan’s Gulf Coast Express pipeline to meet growing demand for LNG and Mexican natural gas exports out of South Texas. However, new demand is expected before Gulf Coast Express enters service in October of this year, which could exacerbate the gas shortage in South Texas leading to stronger South Texas gas pricing through the end of the summer.

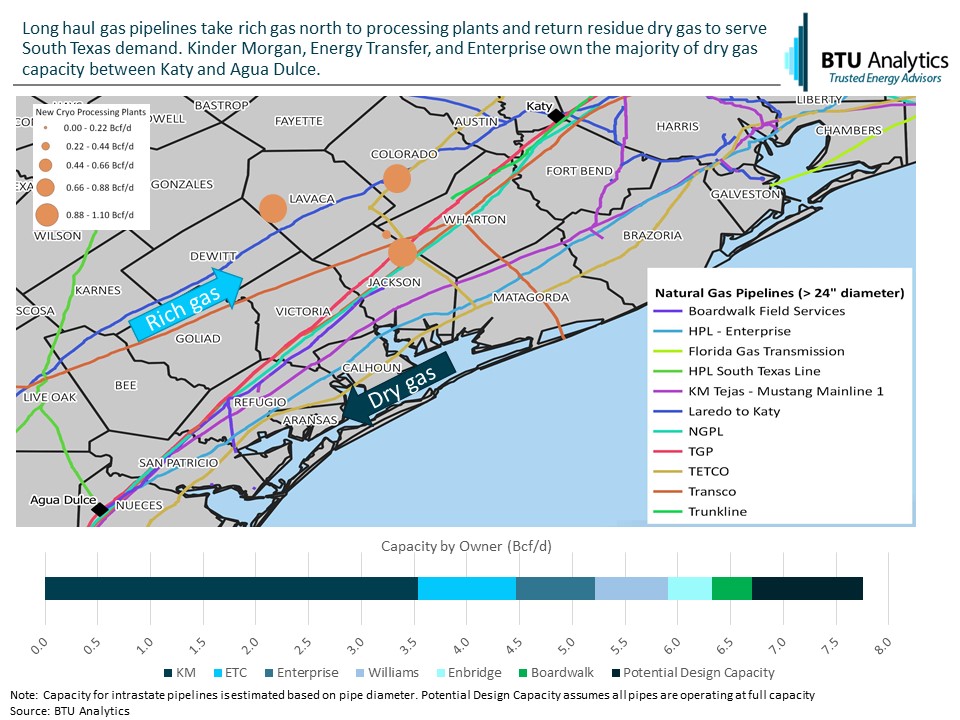

Gas processing plants, built to serve Eagle Ford production, are primarily downstream of Agua Dulce and even further up the coast than Corpus Christi. As a result, unprocessed rich gas volumes from counties such as Live Oak, Karnes, Dewitt, and further west move Northeast on rich gas pipelines. The gas is then processed at plants located in Lavaca, Colorado, and Jackson county, and the residue gas is delivered near the Katy market. From there, the gas flows back south to meet south Texas demand via long-haul natural gas pipelines. The map below highlights natural gas pipelines with diameters over 24 inches. Of these, Kinder Morgan, Energy Transfer, and Enterprise collectively own over 5 Bcf/d of north to south capacity between Katy and South Texas.

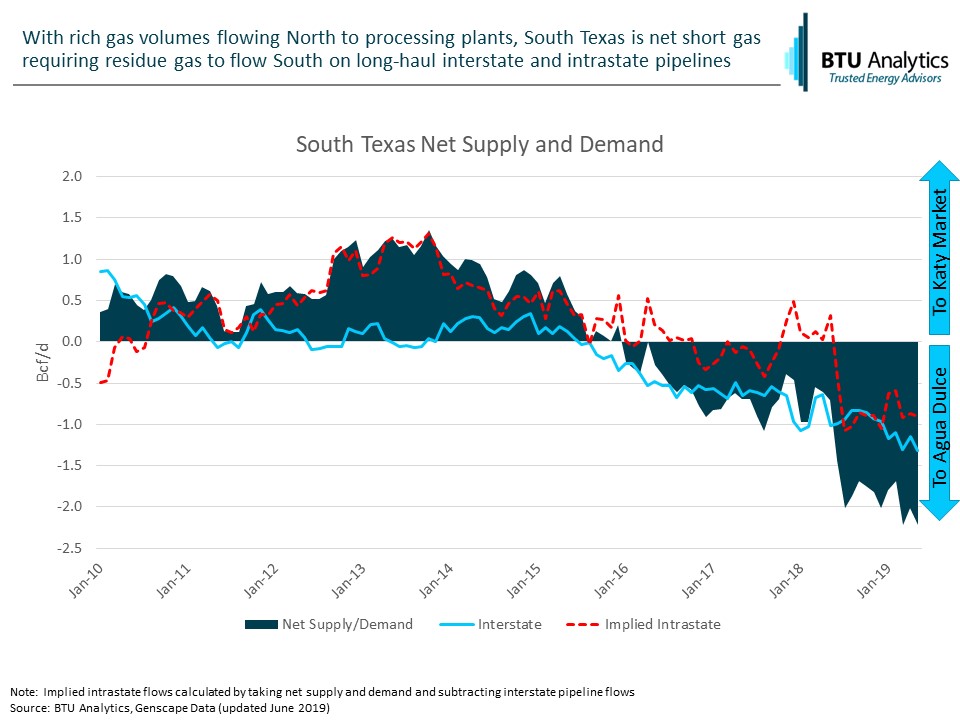

South Texas has historically been long gas due to the development of the Eagle Ford. At its peak, South Texas and Eagle Ford residue gas production was over 6.5 Bcf/d and exceed demand in the region by over 1 Bcf/d as highlighted in the chart below. However, in 2016 the balance in South Texas flipped negative as declining Eagle Ford residue gas production was unable to meet growing demand. As a result, pipelines that traditionally moved Eagle Ford production north to the Katy market and beyond emptied and began flowing south. In May 2019, over 1.3 Bcf/d of natural gas flowed south into the South Texas market on interstate pipelines and an estimated additional 0.9 Bcf/d on intrastate pipelines.

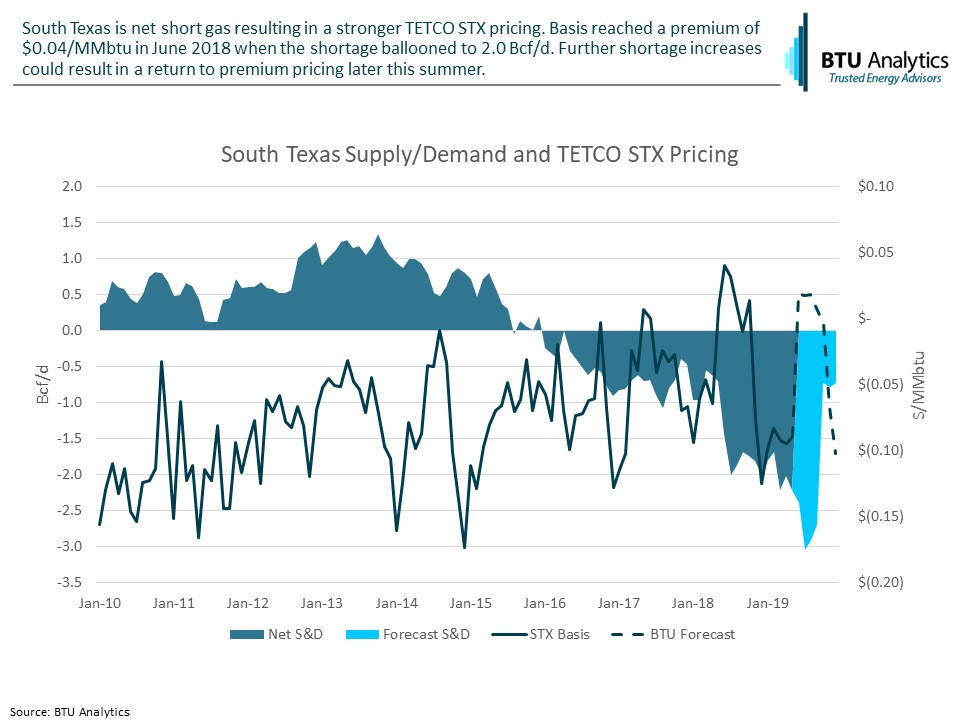

This shift is also illustrated in TETCO STX pricing. As South Texas has gone net short, TETCO STX basis tightened and even traded at a premium to Henry Hub. In June 2018, basis averaged $0.04/MMbtu premium to Henry Hub as South Texas was net short approximately 2.0 Bcf/d of gas. While basis has returned to $(0.09), BTU Analytics projects TETCO STX pricing to strengthen through the remainder of the summer as additional demand is added to the region prior to the arrival of Gulf Coast Express.

Yesterday, TC Energy announced that the Sur de Texas – Tuxpan pipeline has finally entered service after numerous delays. The subsea pipeline connects with Enbridge’s Valley Crossing pipeline just off the coast of Brownsville and could export up to 2.6 Bcf/d of gas from Agua Dulce to Mexico. While interconnects downstream remain delayed, as we detailed in a blog earlier this year, initial flows on Sur de Texas could be as high as 0.75 – 1.0 Bcf/d as BTU Analytics expects South Texas piped gas to displace LNG imports at the Altamira terminal and meet local demand near Tuxpan. Additionally, Train 2 of Cheniere’s Corpus Christi LNG facility will enter service this summer and add an additional 0.6 Bcf/d of demand to the region.

Assuming Eagle Ford gas processing dynamics remain the same, the gas shortage in South Texas may be as high as 3.0 Bcf/d just prior to the start of Gulf Coast Express in October. BTU Analytics expects TETCO STX to enjoy stronger pricing through the end of the summer until Permian volumes on Gulf Coast Express can return the South Texas balance to 2016-2017 levels. For an in-depth look at regional supply and demand dynamics and their effects on basis pricing, request a sample of our recently published Gas Basis Outlook which covers TETCO STX as well as 23 other basis points across the US and Canada.