While coal retirements tend to capture all the headlines, natural gas retirements warrant attention in that as recently as 2018 over 8 GW of gas capacity retired. In 2020, natural gas has been the biggest contributor to US power generation making up 45% of capacity and 40% of power generation, respectively. While coal retirements have made room for gas to expand as a percentage of generation over the last decade, older gas plants are facing increasingly competitive markets, not only from new wind, solar, and energy storage projects but from new combined cycle gas plants as well. In this Energy Market Insight, a look at gas plant retirements may show the coming headlines are not as bad as they may seem.

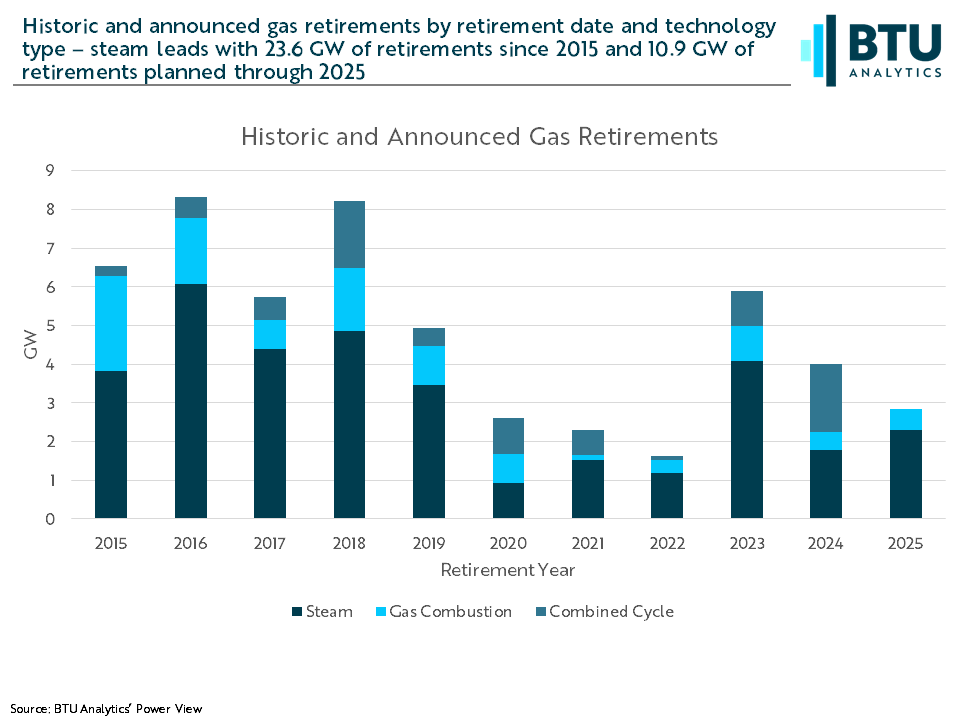

Existing gas capacity is dominated by combined cycle plants which typically provide baseload power and have the ability to ramp quickly to meet peaking demand. Plants comprised of gas-fired steam turbines, which take longer to start up than a combustion turbine and are much less efficient than more recent combined cycles, sit third in the capacity rank and yet represent over 67% of total gas plant retirements going forward as shown above. Gas-fired steam turbine development peaked in the 1970s, which helps to explain why many units have trailing 12-month capacity factors of less than 30% and are slated for retirement. When looking at gas plants in operation today, the combined cycle fleet has an average in-service date (ISD) in 2000, gas combustion turbines in 1996, and steam turbines in 1968.

As shown above, we see total gas plant retirements from 2015-2020 have been 36.4 GW with an additional 16.7 GW expected 2021-2025. Gas steam units have been leading gas plant retirements with over 23.6 GW retired since 2015 and another 10.9 GW expected to retire through 2025. To put this in perspective, 76.1 GW of coal has retired since 2015 and another 29 GW of coal is expected to retire through 2025.

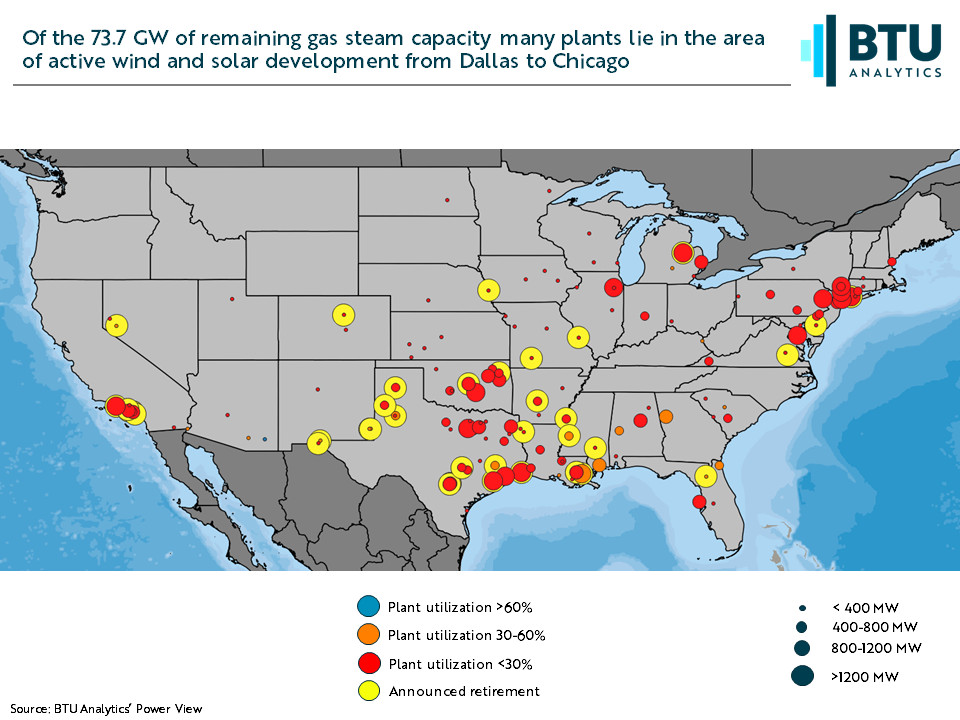

In the image below we can see many of the large units/plants with low utilization (in red) have already announced retirement (shown in yellow) especially in Southern California and the Texas Gulf Coast. The Dallas-Fort Worth area and Oklahoma have multiple medium to large plants with low utilizations and no announced retirements. The amount of wind and solar development in ERCOT will continue to put pressure on these plants, as we have seen in the Texas Panhandle where all the gas-fired steam turbines have announced retirements. Additionally, there are many small, low-utilization plants in Kansas, Nebraska, Iowa and Illinois which lie in the heart of the US wind development belt from West Texas to Chicago. These units/plants too will see competitive pressure going forward.

Gas steam plant contribution is less than 10% of total natural gas generation. No doubt many of these units will continue to see pressure to retire based on economic and increasing local environmental scrutiny. While the headline will call out ‘another gas power plant retires’, the impact to the natural gas industry may be muted considering many of these plants have low capacity factors already and contribute a small portion to total natural gas generation. To follow power market developments, request a demo of BTU’s Power View analytics platform.