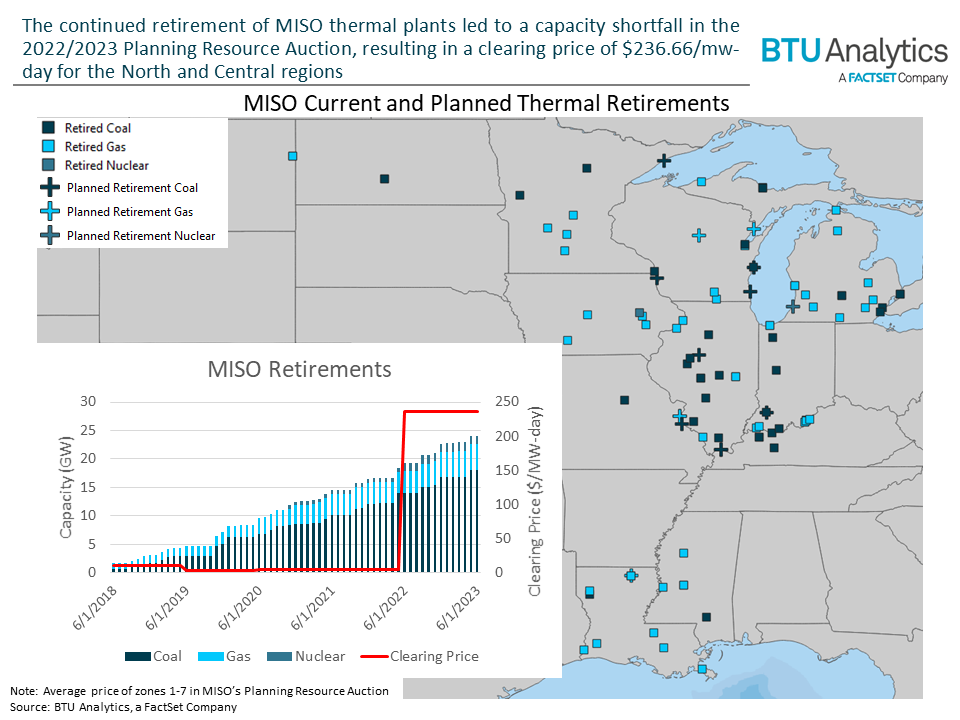

On April 14th, 2022, the Midcontinent Independent Service Operator (MISO) released the results of their 2022/2023 delivery year Planning Resource Auction (PRA). In MISO’s North and Central regions, the amount of capacity that cleared the auction was 96.8 GW, well short of the 101.2 GW requirement to meet peak load in the regions during the upcoming delivery year, which goes from June 1st, 2022, to May 31st, 2023. Adding in 3.2 GW of imports from external resources and the MISO South region still left the North and Central regions 1.2 GW short of meeting the required amount of capacity. This led to the North and Central regions clearing the auction at a price of $236.66/MW-Day, while the South region, which did not have a capacity shortfall, clearing the auction at $2.88/MW-Day. Today’s insight will explore how MISO got to this point and the near-term outlook of MISO’s capacity and generation.

From 2018 to 2021, the PRA resulted in clearing prices of less than $10.00/MW-Day for most of the zones within MISO’s North and Central regions. However, the most recent auction cleared all 7 North and Central zones at $236.66 due to there not being enough capacity to meet the peak demand. While part of the reasoning for this is that the load forecast came in higher than expected, MISO has also seen a decrease in accredited capacity, which accounts for capacity factors of renewable resources. As shown in the map below, from June 1st, 2018, to June 1st, 2022, there were 19.3 GW of thermal retirements across the ISO, with more to come.

While this was somewhat offset by 6.3 GW of gas, 12.2 GW of wind, and 2.9 GW of solar either placed into service or planned to be in service by June 1st, 2022, these new additions were not enough to offset the thermal retirements, leading to the capacity shortfall in the North and Central regions. In part, this is due to how much credit MISO gives wind and solar farms in the PRA.

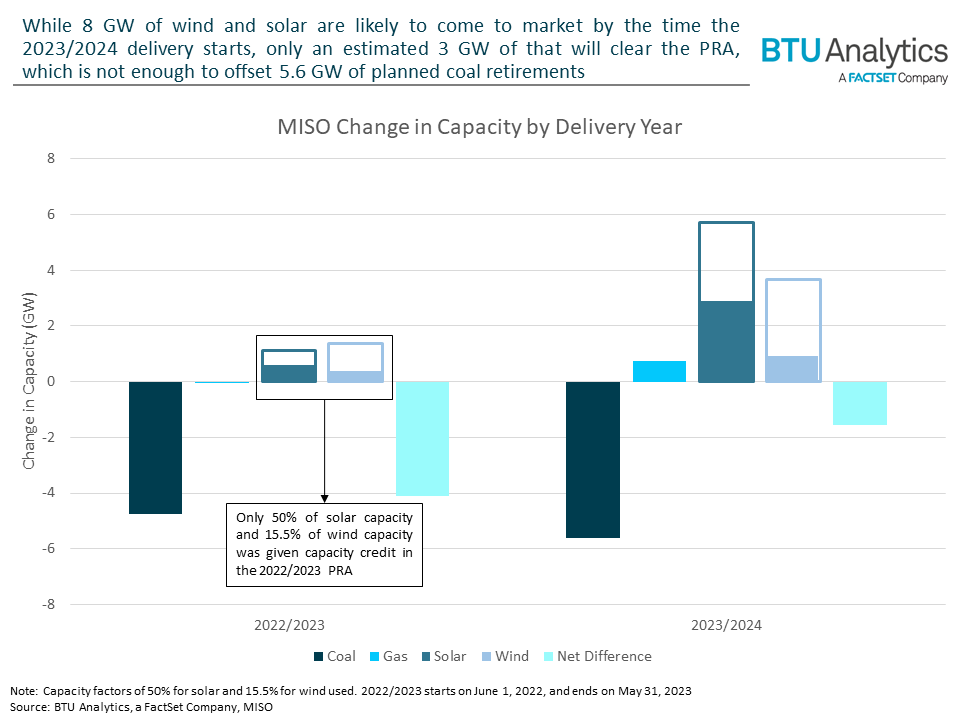

Since the PRA is based on meeting peak demand, MISO focuses on what plants can produce in hours ending 15, 16, and 17. For solar farms, MISO accredits their capacity at their average generation during peak hours over the past 3 years. For new solar facilities, this is assumed to be 50%. For wind farms, MISO determines the total amount of wind generation that can be relied upon during peak hours. This resulted in an average capacity factor of 15.5% for the 2022/2023 delivery year. These discounted rates are part of the reason that MISO will not be able to offset the amount of coal retirements that have been planned over the next two years.

We can see that the net difference in accredited capacity for 2022/2023 is -4.1 GW. Furthermore, despite more gas, wind and solar generation planned for 2023/2024, the net difference is still at -1.6 GW, implying that the capacity shortfall may get even larger next year.

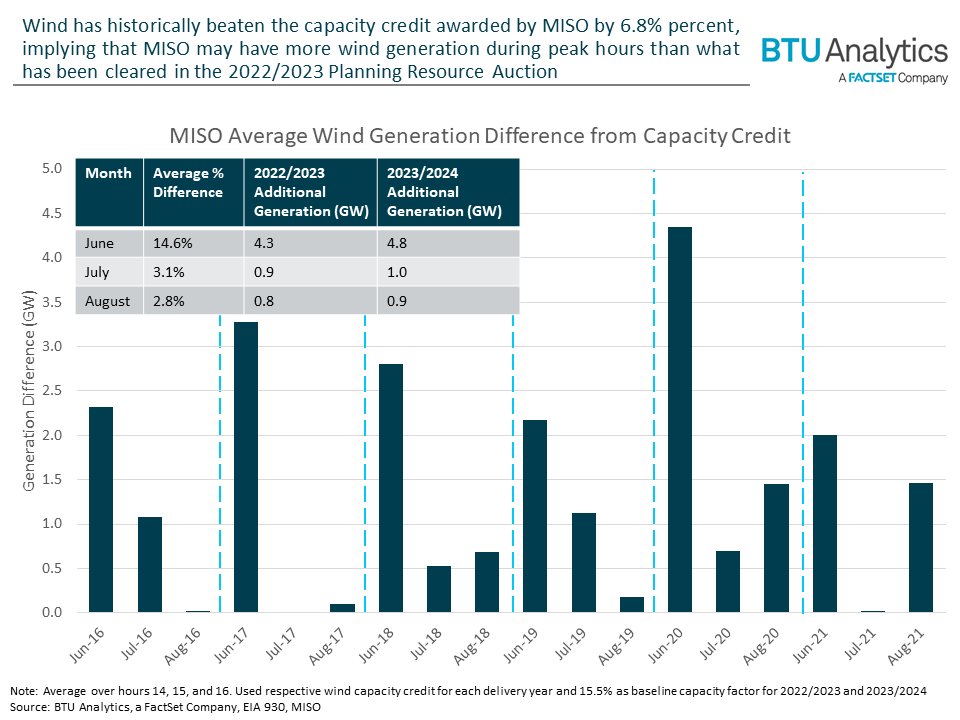

While this capacity shortfall does mean an increased risk of planned outages and increased load shedding, the risk may not be as high due to the amount of wind generation seen during peak hours over the past 6 years.

Wind generation has been 6.8% higher than what MISO has given wind farms in the PRA, showing that there is the potential for more generation than what clears the auction. However, this is heavily driven by wind farms in June outperforming the MISO wind capacity credit by 14.6%, providing between 2 and 4.3 extra GW compared to the PRA. With July and August only producing 3.1% and 2.8% more than the MISO wind capacity credit MISO is more likely to have a tighter margin between load and available capacity during these months.

MISO’s capacity shortfall highlights the difficulties of balancing state climate goals and the energy transition with grid reliability. The shortfall may result in heightened risks for load shedding and blackouts during peak summer hours for each of the next two delivery years. This will lead to high peak pricing in MISO and create new trends to explore in future Insights.