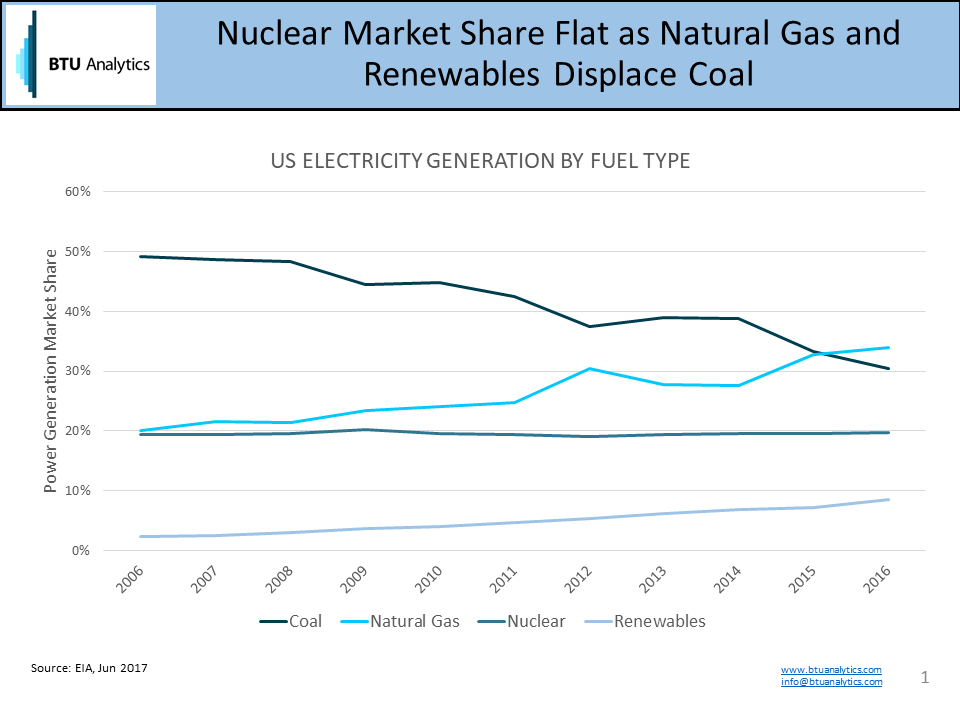

Last month, BTU Analytics published an analysis of global energy consumption trends, highlighting that the United States is decarbonizing over time as consumption trends rotate away from coal and oil towards natural gas and renewables. For power generation, specifically, natural gas and renewables have offset declines in coal, while nuclear power’s market share has stagnated, even though it emits zero carbon. The graph below shows the change in market share for the top four power sources in the US, representing 93% of the market.

The Cost of Zero Carbon Power

Nuclear power plants cannot compete with other fuel types on cost alone. States recognize that a power source with zero carbon emissions is valuable, but that value is not easily monetized by power companies, and nuclear plants are subject to much greater (read: costly) regulation; hence, some states offer subsidies to incentivize both innovation and sustained operation.

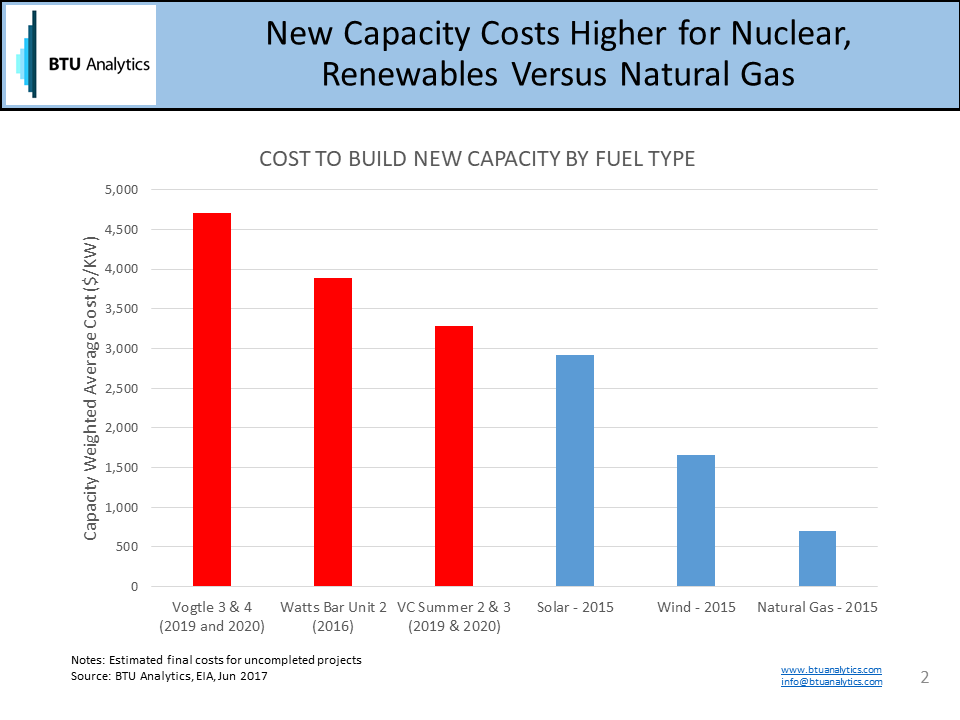

The chart below highlights the average cost by power source type in 2015 (most recent EIA data, US average cost), and compares it to the cost per kilowatt of the five nuclear reactors that have come online or are scheduled to come online by 2020. The nuclear plants are more expensive than wind or solar, and the average of the five plants is over 400% more expensive than natural gas generators. Wind, solar, and natural gas comprised 98% of the 18,025 MW of new capacity in 2015.

Tax Subsidies Keep Nuclear Operations Feasible

With wholesale electricity prices near 15-year lows, nuclear plants are struggling to compete with other fuel types. Last June, Exelon announced that they would be closing the Clinton and Quad Cities power plants in June 2017, primarily because they were losing a combined ~$100 million per year. At the final hour of the Illinois legislative session in December 2016, a bill was passed that enabled the plants to continue operating. The bill provides $235 million annually in subsidies for the next 10 years under the Zero Emission Standard.

New York passed a similar bill that is also designed to support both nuclear and other renewable technologies. There are several other states considering similar measures, including Pennsylvania, Connecticut, New Jersey, and Ohio. Currently, a bill presented to Ohio lawmakers has faced more intense opposition than the bills in New York or Illinois because many people claim that the law will only benefit nuclear plants (versus a broader scope of renewable technologies).

Impact on Natural Gas

The table below shows announced nuclear closures in the next five years. While not all lost supply would be replaced by natural gas, it is worth noting that any additional closures or deferred closures will have a material impact on the market. If the five plants listed below close as scheduled, there will be approximately 0.9 Bcf/d equivalent demand that will be serviced by another source. Similarly, the legislation passed in New York and Illinois effectively kept 0.8 Bcf/d equivalent demand from being serviced by another source.

![]()

If natural gas and coal prices remain cheap, nuclear plants could face increased pressure to close in the absence of additional subsidies. How will changing power demand characteristics, power plant utilization, and regional constraints fit in with other variables in the natural gas market? How will those fundamentals impact producers across the US? BTU Analytics’ monthly Henry Hub Outlook includes a comprehensive analysis of natural gas supply and demand fundamentals, including updated and projected power plant operating dynamics.