In Q2’2014 earnings calls, Permian producers highlighted continued infrastructure challenges. While midstream companies are racing to solve the current infrastructure bottlenecks in the Permian, producers continue to ante up, drilling more and more wells, raising the stakes not only for operators in the basin, but threatening the balance of the entire market.

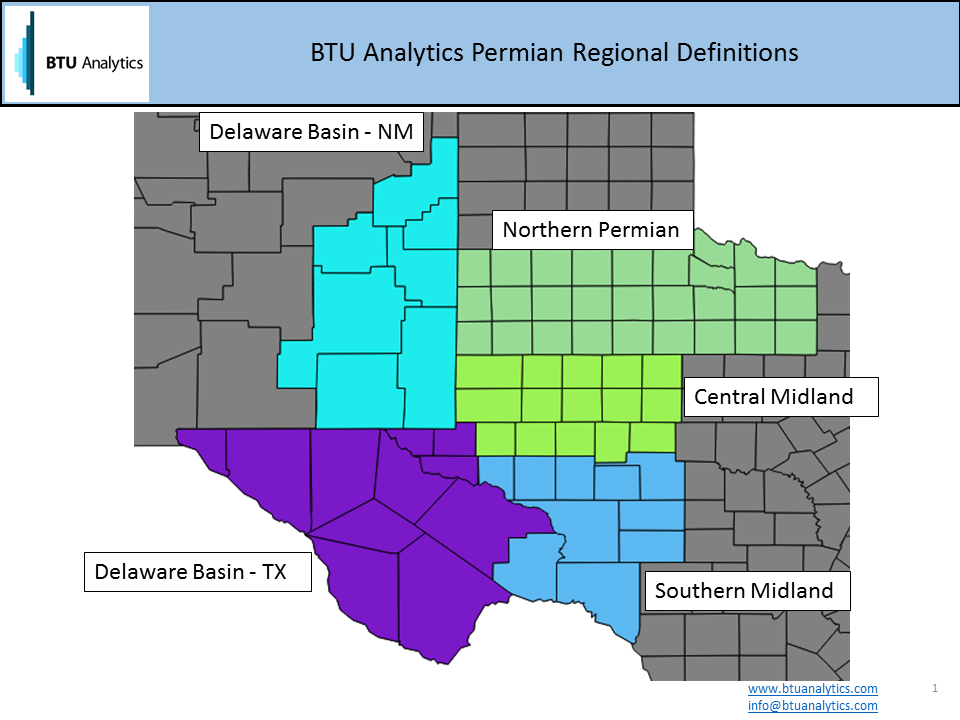

The Permian basin covers more than 70 counties across Texas & New Mexico (see map below map) and currently produces 5.2 Bcf/d of liquids rich gas, accounting for 6.7% of lower 48 US production, and 1.6 MMb/d of crude oil, or almost 19% of US production in July.

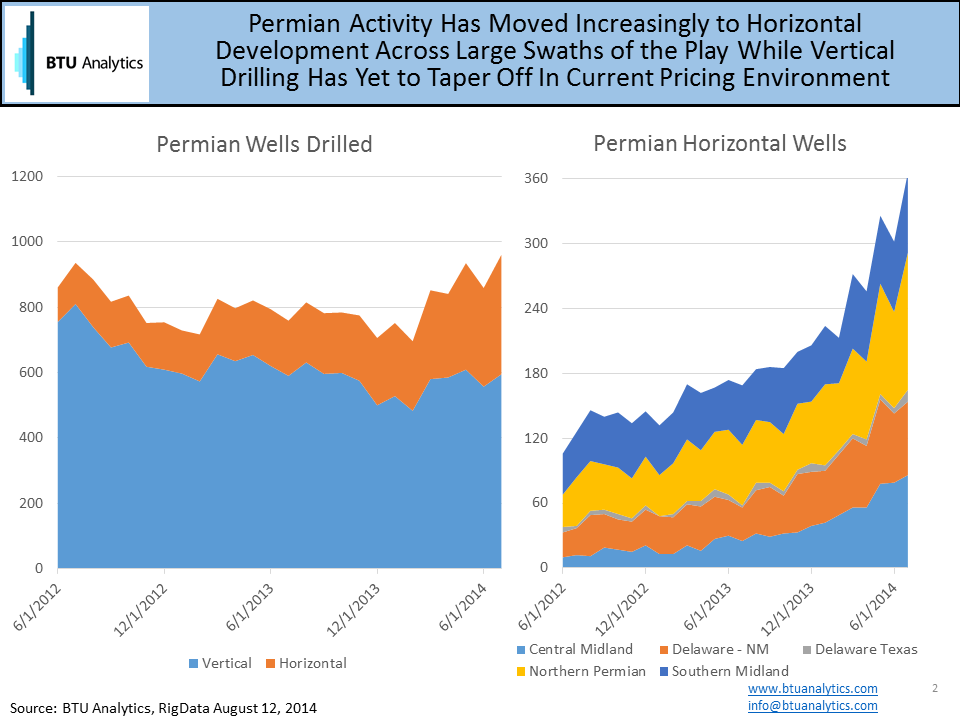

Activity in the basin is at an all time high, as producers explore the limits of potential of new horizontal plays in the Bone Springs and Wolfcamp formations among others. Producers have menagerie of targets in the Permian that should provide decades of drilling opportunities as completion techniques are refined across broad swaths of the play. In addition to the new horizontal development, private and public producers continue to drill hundreds of vertical wells exploiting conventional and tight sand horizons in the play.

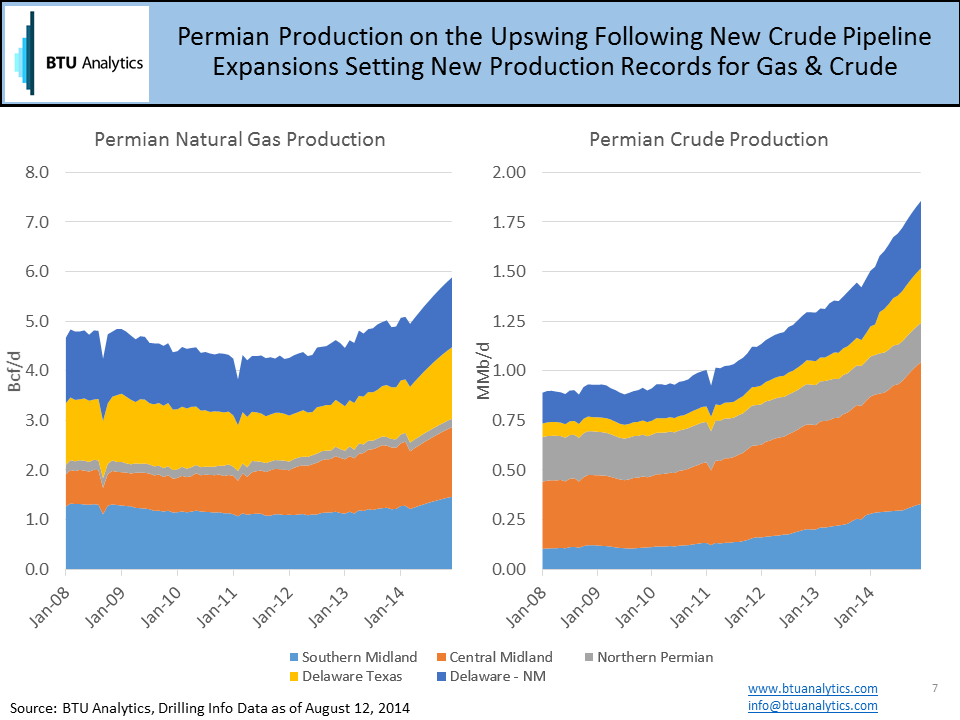

Permian production of both natural gas, natural gas liquids, and crude oil have started to accelerate over the last 18 months and BTU Analytics expects that trend to continue over the next twelve months and beyond. By the end of the year, Permian oil production could increase by over 200 Mb/d as the new Bridgetex pipeline temporarily debottlenecks the region and the accompanied boost in natural gas production results in an additional 0.5 Bcf/d coming to market.

By the end of 2015, the Permian should see more than 700,000 B/d of new oil pipeline capacity to the Gulf coast with the start of the 300 MB/d Bridgetex pipeline, 200 MB/d from the Permian Express 2 Pipeline, and 200 Mb/d from the Cactus pipeline. On top of that, Scott Sheffield, CEO of Pioneer Natural Resources, one of the largest acreage holders in the basin, sees the need for an additional 1.0 MMB/d of pipeline capacity in 2017-2018 and the BTU Analytics outlook for the Permian confirms those projections based on current drilling activity. However, can the US market support another 1 MMbcf/d of Permian oil production beyond the 0.7 MMb/d of growth from the current wave of pipeline expansions? Can regulatory change in Washington happen fast enough to give producers an international market for those barrels or will the Gulf coast become increasingly awash in supply benefiting refinery pocketbooks? What will producers do with the significant quantities of associated gas and liquids? Could new NGL pipelines and gas pipelines be in the works as well to facilitate additional exports?

For more on BTU Analytics, infrastructure tracking products and production analysis in the Upstream Outlook, please contact info@btuanalytics.com

Photo by @MTPetroleum on Twitter