The Wall Street Journal recently reported that privately held Permian operators, which have led the recovery in drilling activity since the pandemic, are running out of untapped resource. Specifically, the article stated that, at the current pace of drilling, 5.6 to 5.8 years of drilling inventory remain for private operators in the Midland and Delaware, respectively. While private producers certainly have lower inventory than public producers at current drilling rates, BTU Analytics’ proprietary inventory model shows private operators have an average 7.3 to 12.1 years of inventory remaining in the Midland and Delaware, respectively. Underlying assumptions, such as those regarding lateral length, spacing, and the perceived viability of stacked pay, can cause inventory models to differ heavily, thus leading to wide ranges in estimates. Because of these differences, today’s Energy Market Insight will focus on a different approach: how a depletion in undrilled acreage would reveal itself in real data.

It is well-documented that privately held producers drove the surge in Permian rig activity over the last two years, which only recently began to roll over. However, completions lagged drilling activity this year due to constraints on frac crews, sand, and other materials. Preliminary completion data shows privately held producers drilled 46% of Permian wells YTD, up from 26% in 2019, but this group only completed 37% of the wells so far this year, up from 25% in 2019. However, the elevated drilling rates suggest private producers are certainly drilling their acreage at a much faster rate than publicly traded producers, which have largely passed on rapid activity increases in favor of higher returns to shareholders.

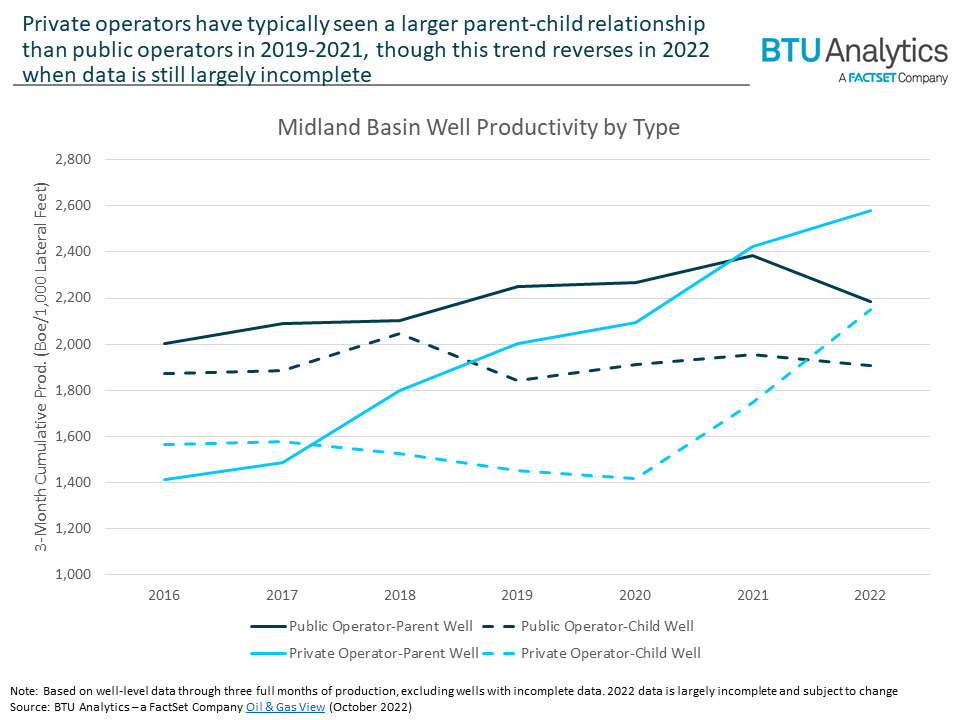

These higher drilling rates are not necessarily an issue unless there is little acreage to support them. As highlighted above, BTU Analytics estimates privately held producers hold 7.3 years of undrilled inventory in the Midland Basin, which has the heaviest concentration of private producers. As the Wall Street Journal highlighted back in 2019, producers will rely more heavily on infill drilling as they continue to drill out their acreage and attempt to extend their inventory. Historically, these infill wells are less productive than the ‘parent’ wells that preceded them, as shown in the chart below.

For both public and private producers in the Midland Basin, child wells are generally less productive through their first three months of production. However, the negative relationship is typically more impactful for private operators. From 2019 to 2021, child wells underperformed parent wells by roughly 30% through the first three months for private operators, compared to a 17% underperformance for public producer child wells. This underperformance converged in 2022, though much of this year’s data is incomplete. Still, private producer well productivity continues to improve after adjusting for longer laterals, surpassing those of public operators this year.

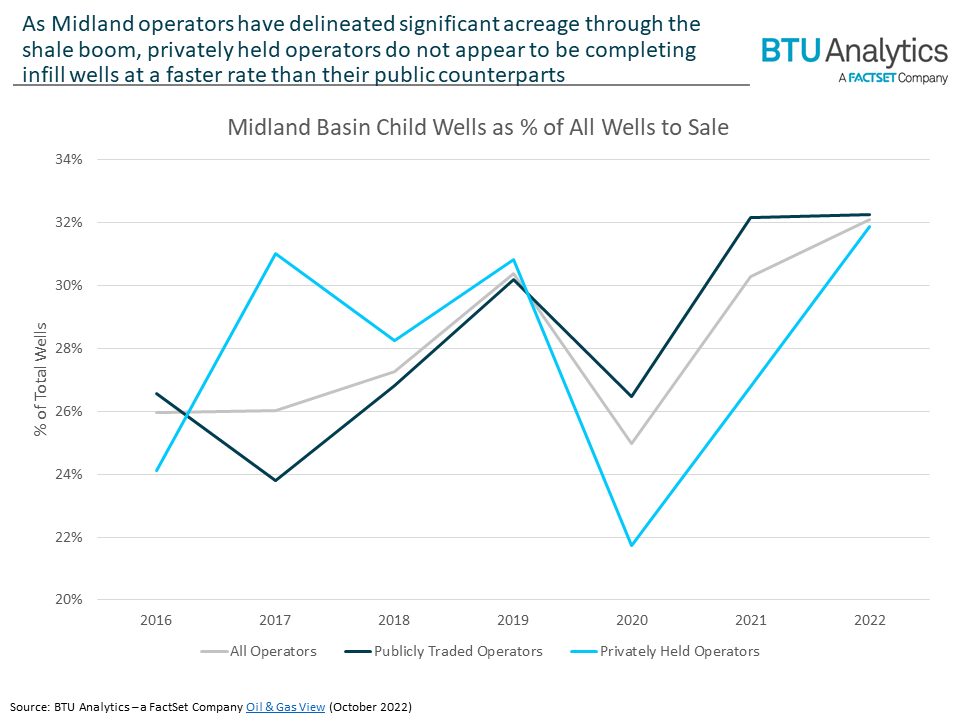

Because of this parent-child relationship seen by both private and public operators, increased infill drilling would likely drive a decrease in overall productivity. As stated above, that’s not yet the case. The chart below shows the percentage of child wells completed since 2016 in the Midland Basin. While child well completions for both operator types are generally rising, privately held operators aren’t much different than publicly traded operators. 2022 data shows child wells represent 32% of all wells to sale YTD. BTU Analytics expects private producers would drill far more child wells if low breakeven acreage was nearing depletion.

With several years of low breakeven inventory remaining for private operators in the Permian, more consolidation, like what was seen from Diamondback this week, is likely on the way. However, continued oil price volatility could dampen deals, which has already been seen this year.

While most private operators are likely unconcerned about inventory longevity today, their rapid pace of drilling will eventually cause inventory issues. As detailed in recent editions of the Upstream Outlook, BTU Analytics expects private operators will be an important part of the forecasted pullback in drilling activity next year. For more information, contact info@btuanalytics.com or request a sample of the Upstream Outlook today.