The year 2019 has been cruel to many oil and gas stocks. Appalachian producers have been particularly hard hit, with many reaching record low valuations following the drop in stocks since mid-May. But this recent drop is a small piece of what has been a long decline in market valuation for a number of publicly traded Appalachian producers. Today’s Energy Market Commentary will take a look at trends in valuation for the largest Appalachian E&Ps.

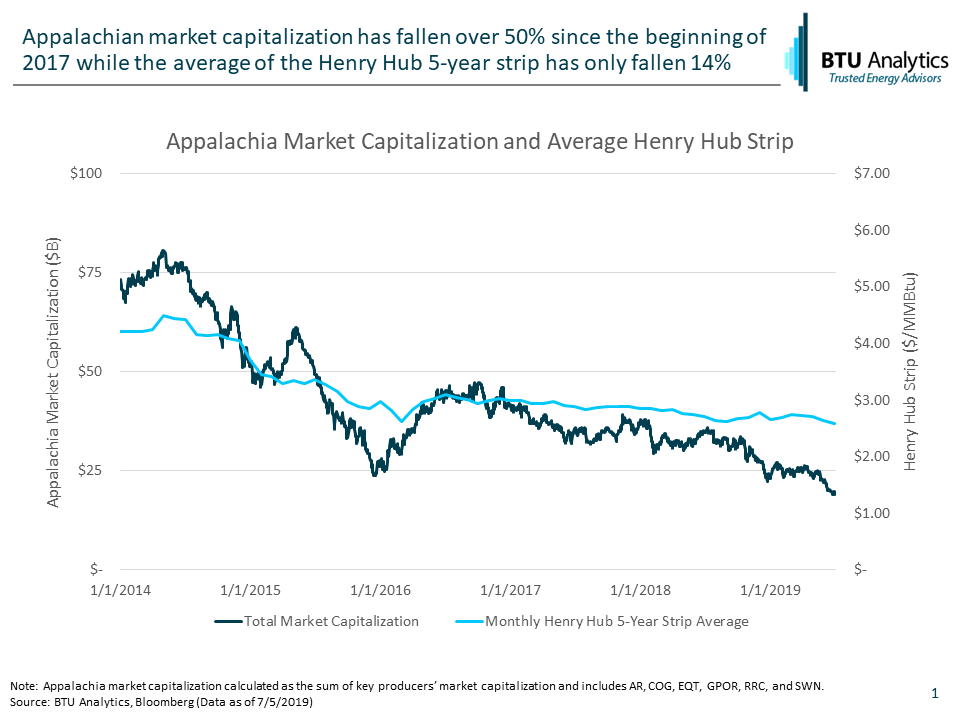

The chart below shows total market capitalization for key Appalachian producers versus the average of the 5-year Henry Hub strip over time. The producers included are Antero Resources (NYSE: AR), Cabot Oil and Gas (NYSE: COG), EQT (NYSE: EQT), Gulfport Energy (NASDAQ: GPOR), Range Resources (NYSE: RRC), and Southwestern (NYSE: SWN). The average of the 5-year strip over time shows that the recent decline isn’t necessarily due to a change in the outlook for natural gas pricing. Since the start of 2017, the 5-year Henry Hub strip has declined slightly, falling about 14% to $2.58/MMBtu for July 2019. Over the same period, market capitalization of the six producers has fallen over 50%.

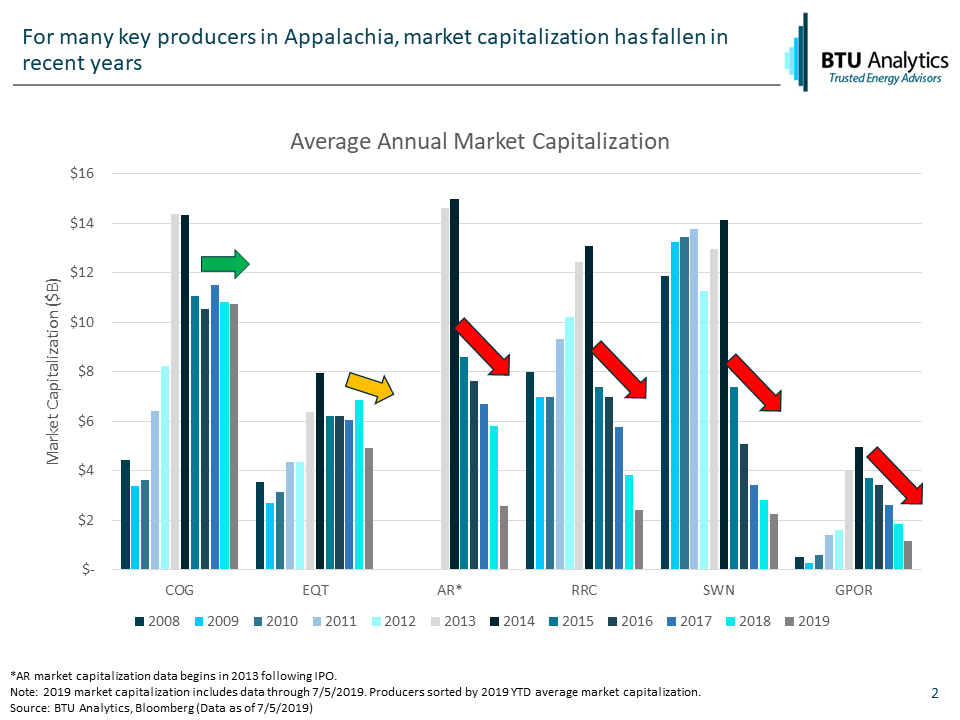

Let’s take a closer look and see how individual producers have fared in recent years. The chart below shows average annual market capitalization for a sample of Appalachian producers. As one might expect, most of these producers have followed the same downward trend as Appalachia as a whole.

A number of the companies have a market capitalization that is less than 20% of their 2014 values. However, two producers have notably bucked the trend. Cabot Oil & Gas has been an exception to its peers as its market capitalization has remained steady. Since 2016, Cabot has been free cash flow positive and consensus estimates indicate that the market expects them to continue to do so in 2019 and 2020.

EQT is the other producer in this sample that bucks the trend, but for different reasons. EQT’s market capitalization increased in late 2017 as the result of the acquisition of Rice Energy. Late 2018 saw a reduction in the company’s market capitalization as the company spun off Equitrans Midstream to shareholders. More recently, the company has been embroiled in a proxy battle between EQT management and the Rice brothers, fighting for control of the combined entity.

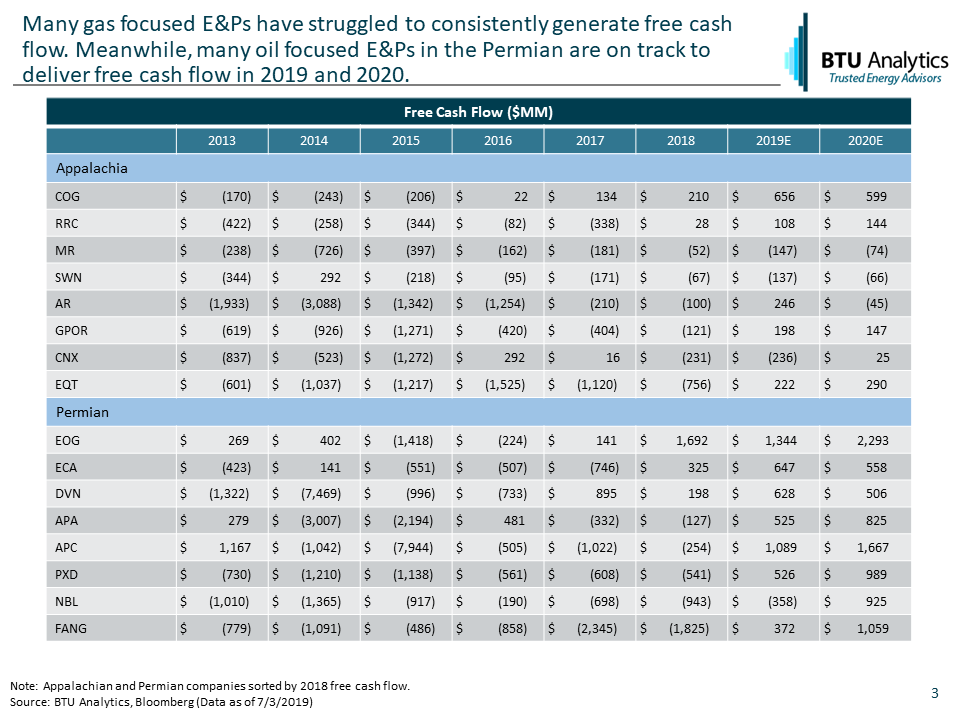

Why the continued decline in valuation for Appalachia? One reason is that while regional growth is slowing, positive free cash flow is still difficult to come by for some producers. Historical and analyst estimates for future free cash flow by producer are listed below.

Only four out of the six Appalachian E&Ps are currently expected to generate free cash flow both this year and next year and with prices languishing at multi-year lows, those expectations on free cash flow may need to be revisited.

With Gulf Coast Express and Midship set to add nearly 3.0 Bcf/d of new pipeline capacity to the Gulf region this fall, market expectations of a rebound in natural gas prices are muted at this point. Thus, Appalachian valuations languish. What catalysts might return market optimism for Appalachia? Where will Appalachian production go from here? For more information on BTU Analytics’ views on natural gas production in Appalachia as well as the rest of North America, request a sample of our Upstream Outlook.