Last week, the Baker Hughes’ rig count dropped 19 rigs as the total US rig count fell to 916, the lowest level since November 2017. The drop comes as no surprise after second quarter earnings from E&P companies signaled an imminent decrease in second half drilling activity, as we discussed earlier this month. While the slowdown will impact gas production across the board, gas plays are likely to be the hardest hit as natural gas prices remain low and US gas demand begins to stagnate. In today’s energy market commentary, we take a look at US natural gas production and what the future could have in store as the drilling slowdown begins.

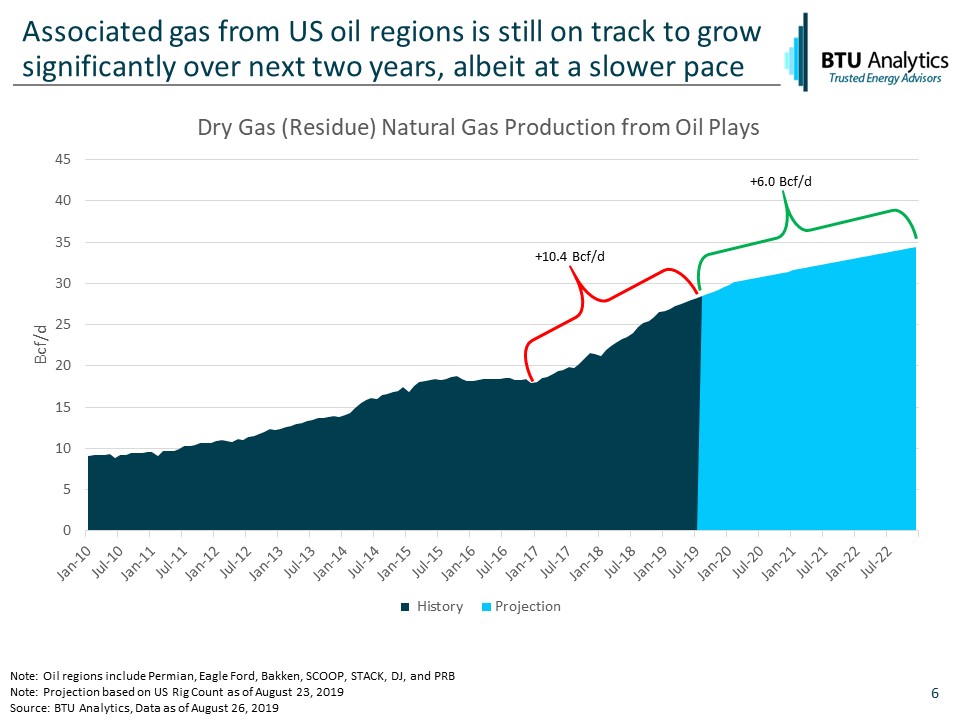

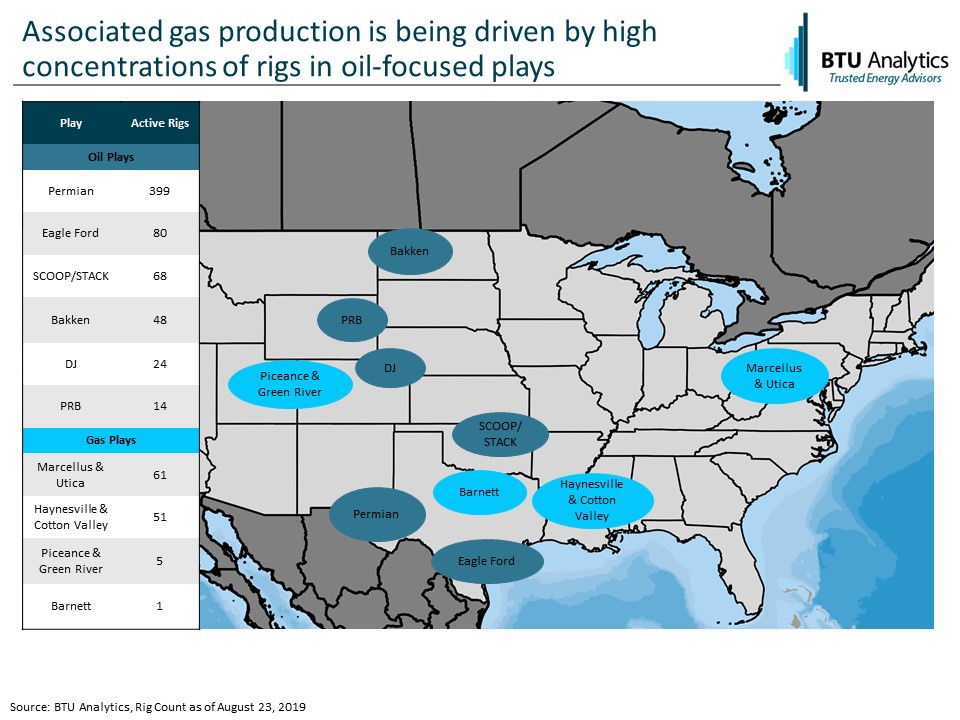

Associated gas production from US oil plays has seen significant growth in recent years, growing nearly 10.4 Bcf/d since January 2017. This growth was driven by constructive oil prices and occurred despite sinking natural gas prices. Since 2017, Henry Hub has fallen over 35% to just $2.15/MMBtu as a result of abundant US shale gas production. Oil price forecasts remain tenuous amidst global political turmoil today, but associated US gas production is still projected to continue to grow over the next three years, albeit at a slower pace than previous years. Assuming current rig levels, associated gas production is projected to contribute approximately 6 Bcf/d of growth through the end of 2022. That growth will come primarily from the Permian and the DJ as pipelines and gas processing infrastructure comes online to relieve constraints.

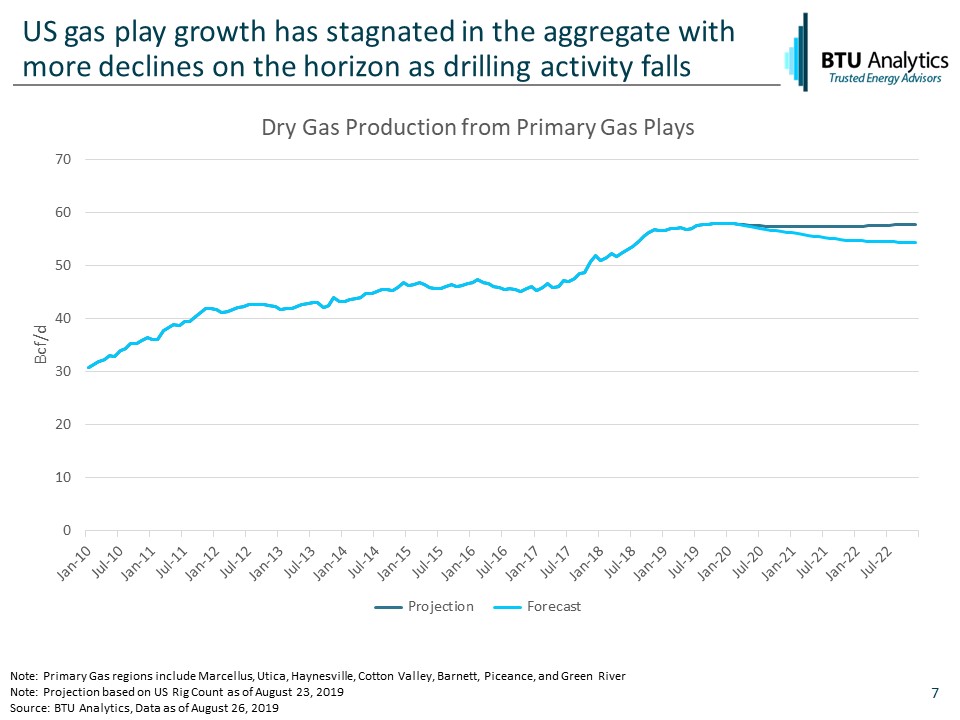

However, the rise in associated gas production has come at the expense of production from gas plays. While gas play production increased by 5.9 Bcf/d in 2017 and 4.8 Bcf/d in 2018, 2019 production has stagnated, rising just 1 Bcf/d year to date. At current rig levels in these plays, dry gas production is projected to flatten over the next three years. However, with associated gas projected to increase by 6 Bcf/d, production from dry gas plays may need to decline even further to balance the US gas market. As illustrated in the chart below, BTU Analytics expects production in primary gas plays to decrease by over 3.3 Bcf/d by the end of 2022.

Decreased second half drilling activity may slow growth through the end of 2019. However, the bigger impact will be felt in 2020 and beyond. At current natural gas prices, gas-focused plays should face further declines. However, a second wave of LNG demand is on the horizon which could lead to a new period of growth for US gas producers. Join us next week for our Getting to the Gulf webinar where BTU Analytics will explore the challenges of supplying Wave 2 LNG. And for more information on US drilling and production forecasts, request a sample of our US Upstream Outlook.