Wyoming’s Powder River Basin (PRB) has been marketed as the next big stacked play opportunity by several public and private E&P companies for quite some time now. BTU Analytics discussed the economics of the basin in a 2018 energy market commentary, but commodity prices and producers’ strategies have changed significantly in the last 18 months. Today’s commentary will analyze recent activity and wellhead economics in the PRB by exclusively using data available through our BTU View user interface.

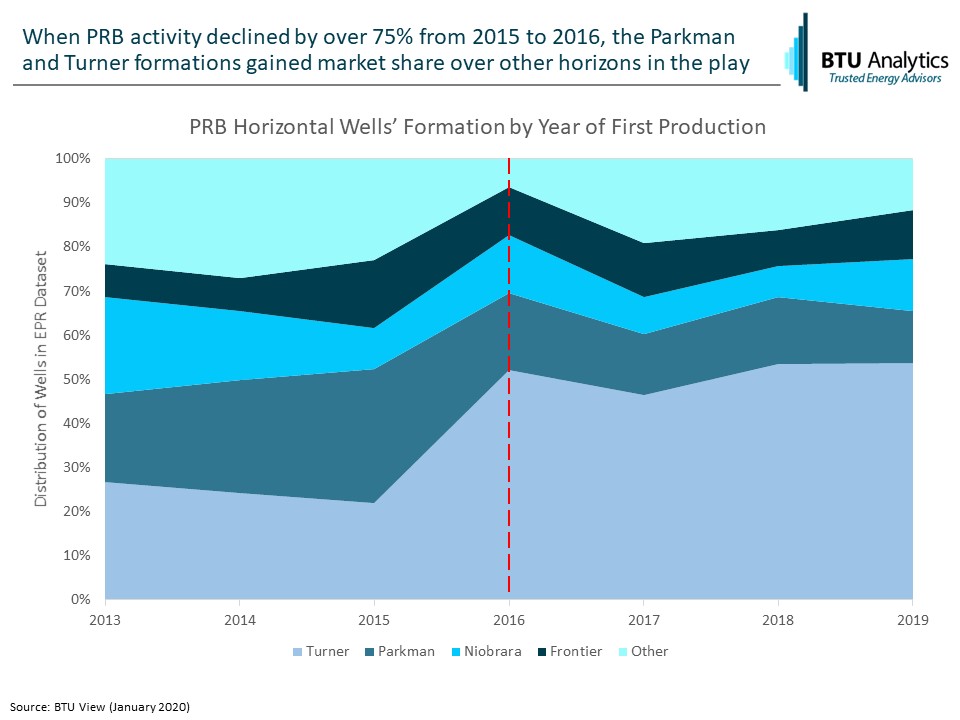

Multiple horizons have been targeted in the PRB throughout the years, but commodity pricing pressure in 2016 narrowed the focus to primarily the Parkman and Turner formations. The diversity of horizons developed plummeted in 2016 as producers’ focus shifted from exploratory drilling to only drilling the most economic wells or simply drilling to hold acreage. In the wake of 2016’s contraction in capital spent in the Powder River Basin, we have failed to see activity diversify away from Parkman and Turner targets to reach pre-2016 proportions. The chart below shows the distribution of wells’ formations in the BTU View dataset by year of first production.

E&P companies’ confidence in the economics of the Parkman and Turner plays allowed them to weather the storm until commodity prices recovered. Even with the return of additional capital allocated to the PRB and activity growth, there wasn’t a material reversal in drilling programs to resume exploration in other horizons. Are the economics of the Parkman and Turner still superior to the other horizons, or have drillers been refusing to fix what isn’t broken?

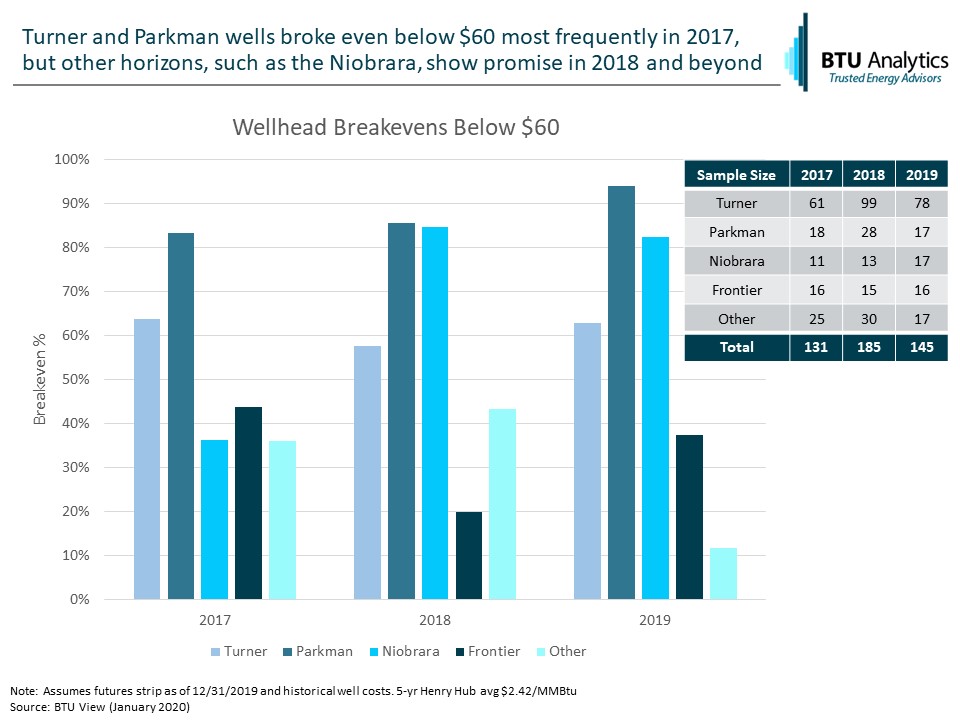

E&P companies have still drilled sub-$60 breakeven Parkman and Turner wells with greater success than the basin average since 2017, but their economics are no longer unquestionably superior to other horizons’ breakevens. While merely on par with other minority horizons’ economics in 2017, the Niobrara horizon has shown improvement in breakevens since 2018, surpassing the ratio of Turner wells breaking even below $60. So how are these Niobrara wells improving their economics?

Average oil initial production rates for the Niobrara horizon have been on the rise since 2017, counteracting the declining trend observed in both Parkman and Turner wells. While initial production rates are only part of the economic equation, they do signal that some minority horizons could be viable competition for capital, especially if well costs improve through additional development. It should be noted that the sample size of the minority horizon wells is significantly smaller than the two primary targeted formations. It remains to be seen how likely recent productivity from minority formations will be sustained as greater extents of the Powder River Basin are delineated.

Producers will need to continue exploring horizons outside of Parkman and Turner in order to improve well costs and repeat promising well productivity. However, until more delineation of acreage in the basin occurs, it will remain difficult to quantify the full potential of Powder River Basin stacked play opportunities. Which parts of the basin show the most development of stacked play? Who are the E&P companies leading the charge to test additional horizons? How much undrilled inventory remains viable in today’s $50 oil environment? The answers to these questions and more can be found in BTU Analytics’ BTU View, where all of the data found in this commentary was pulled exclusively.