As the 2020 presidential election approaches, speculation around what the impacts of a Democratic White House could mean on the energy industry has intensified. One thing is clear: Joe Biden and Donald Trump have very different views on the energy industry and how that impacts the environment. While delving into all these differences would require much more than just one blog post, today’s Energy Market Insight will discuss how a potential ban on new drilling permits on federal lands might impact operators and how they’ve been preparing.

A total ban on fracking appears out of reach in the near-term as any attempt to do so would likely be heavily litigated and take years to implement. However, one move that a Biden White House could make early in the presidency is to limit development on federal lands. In fact, Joe Biden’s own climate plan specifically calls out “banning new oil and gas permitting on public lands and waters.”

A ban on public lands permitting may sound dire for near-term US onshore production, given that fracking has been the primary driver of production growth in the Lower 48. However, the only federal lands that are regularly home to oil and gas activity are the Bureau of Land Management (BLM) lands. Only a small portion of drilling occurs in those areas in relation to the US as a whole. This analysis excludes activity on the Bureau of Indian Affairs lands. Native American tribes are given sovereign nation status and federal limits may not apply to these lands. Onshore drilling activity on BLM lands is typically reserved for the Green River Basin in Western Wyoming, the Piceance in Colorado, and the New Mexico portion of the Permian. Today’s energy market insight will focus on the Permian as the vast majority of current BLM activity resides in the Permian Basin.

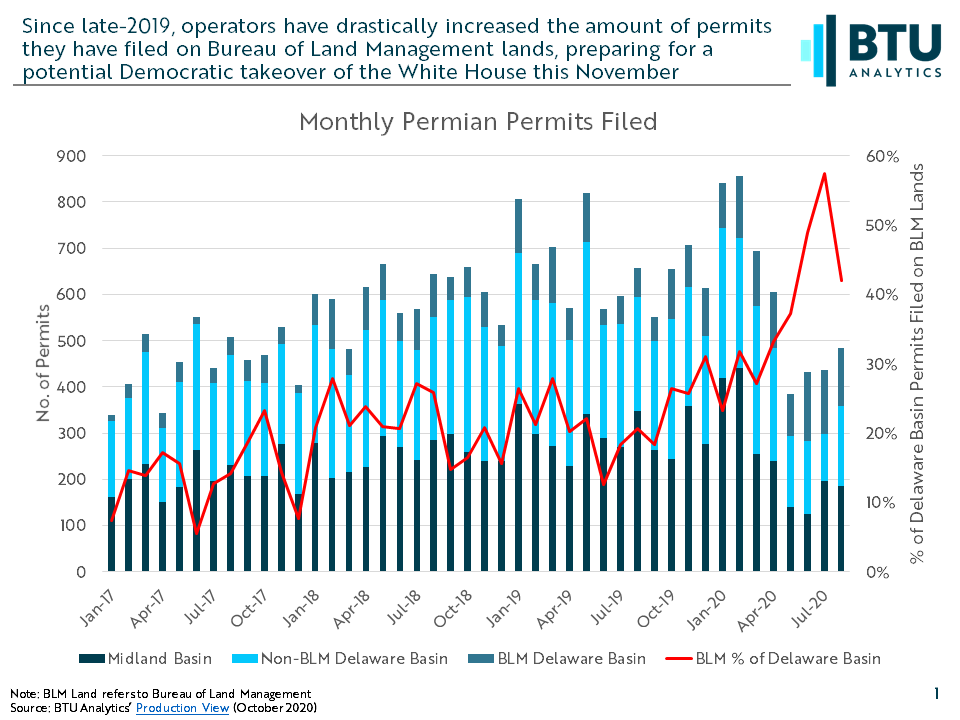

The chart above shows all oil and gas permitting activity in the Permian since 2017, separated by that in the Midland Basin, non-BLM Delaware Basin, and BLM Delaware Basin. The chart illustrates that from 2017 through much of 2019, permitting activity on BLM lands made up between 15% and 25% of Delaware Basin permitting. However, as majors increasingly moved into the Permian and the prospect of federal land permitting ban gained steam, operators have drastically increased the proportion of BLM lands permitting, especially in 2020.

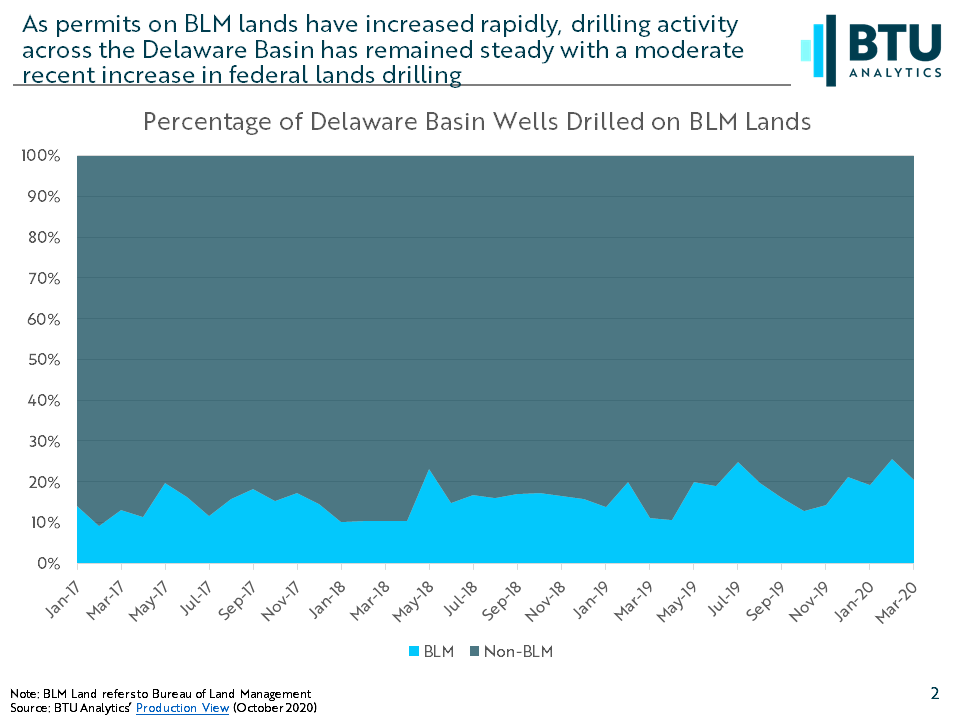

This rapid shift in permitting far outpaces the drilling activity in the Delaware Basin, as shown in the chart below. Since 2017, drilling activity in the Delaware Basin has heavily favored non-BLM lands. All Permian BLM lands are in the Delaware Basin. While the proportion of wells drilled on BLM lands has gradually increased since 2017, it rarely surpasses 25% of all Delaware wells. This mismatch of BLM land permitting vs. drilling activity creates a backlog of permits that can be tapped in the future. This backlog of permits would hopefully be honored if a ban on new oil & gas permitting on federal lands has been enacted.

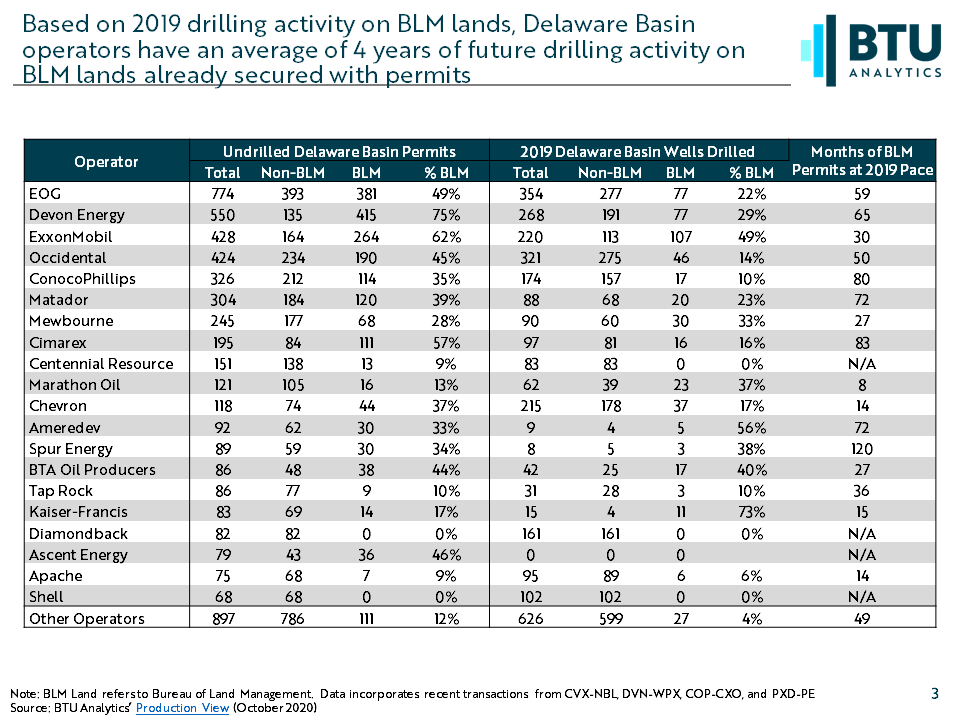

This permitting backlog on BLM lands varies significantly by operator, as the table below shows. The table includes the number of outstanding permits and each operator’s Delaware drilling activity on and off BLM lands in 2019. On average, the top Delaware Basin operators have approximately four years worth of BLM permits based on their 2019 pace of drilling. Basin leaders like EOG, Devon, ConocoPhillips, Matador, and Cimarex have an even longer runway of drilling permits. However, not all operators are prepared. Chevron, for example, focused 37% of its 2019 Delaware Basin drilling activity on BLM land but has just 14 months of BLM land permits based on last year’s pace of drilling.

Any regulatory change to this effect will undoubtedly have an impact on the oil and gas industry. However, the most pertinent questions are who will be impacted the most and how rapidly those impacts will be felt. To learn how a potential ban on federal lands permits could impact oil and gas production across the US, request a discussion with BTU Analytics’ Upstream Outlook analysts on the future of development in these regions.