US energy prices are on the rise. Reduced capital spending across natural gas and coal markets has finally given producers in each sector a boon this winter for pricing in both commodities. Coal prices are up 22% since last November while Winter Henry Hub forwards are trading between $5.00 to 6.00/MMBtu which would be the strongest monthly average since January 2010. A tight natural gas market has contributed to strong natural gas prices increasing the competitiveness of coal in the US generation stack. Today’s energy market insight will explore how coal generation and coal production is responding to higher natural gas prices.

*** To learn more about BTU’s view of this winter’s gas market, be sure to attend our complimentary webinar on Thursday, September 23RD REGISTER HERE ***

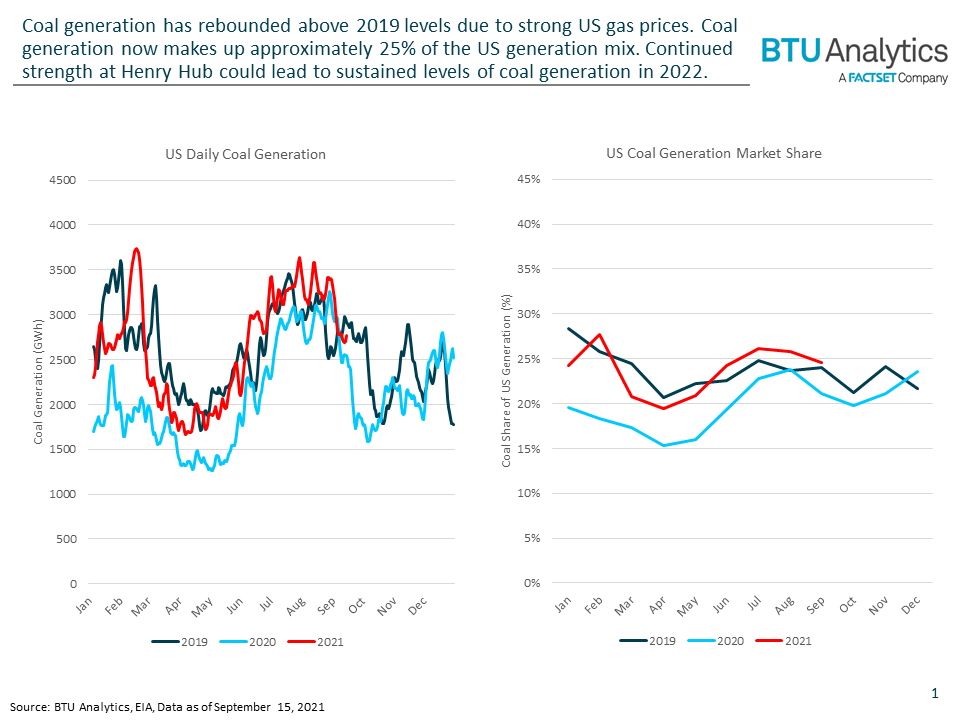

US coal generation has returned and even exceeded 2019 levels driven by strong natural gas pricing and increased demand for electricity in the US. Coal generation year-to-date is 28% higher than at the same point in 2020. Compared to 2019, coal generation is just 0.6% lower YTD, but 3% higher than 2019 since the beginning of the summer. Total US generation has also rebounded in 2020 and is up 5% YTD compared to 2019, but only 0.2% over the summer. Thus, coal generation has increased its share of US electric generation. Coal generation has averaged 23% of total US generation in summer 2021 up from 20% in 2020 and 22% in 2019. This increase though is not entirely at the expense of natural gas as record low hydro generation in the West has helped keep overall natural gas generation higher.

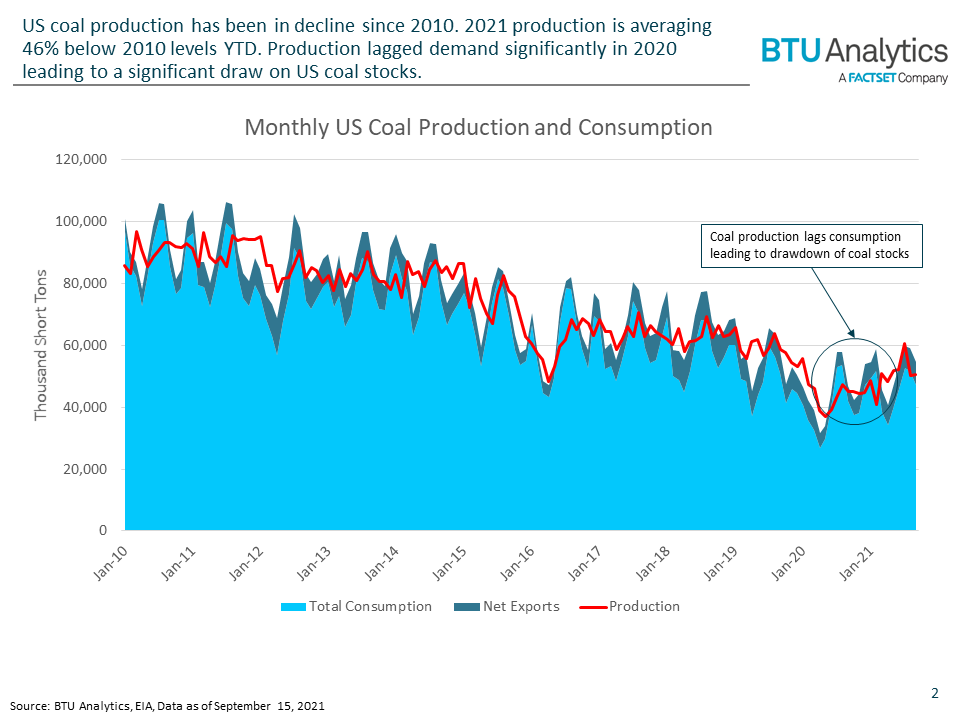

The Henry Hub forward market is currently trading over $4.27 in 2022 indicating that coal generation should continue to be competitive throughout next year. The rebound in coal generation though may come at a time when US coal producers struggle to keep up with rebounding demand for both thermal and metallurgical coal. US coal production has been in decline for over a decade falling from an average of 90 million short tons per month in 2010 to 49 million short tons per month in 2021. That has largely followed the same shape as coal consumption in the electric sector which has declined to an average of 39 million short tons per month compared to an average of 78 million short tons per month over the same time period in 2010. Combined with rebounding US exports of coal driven by strong demand in Europe and Asia, demand has exceeded the supply of coal YTD.

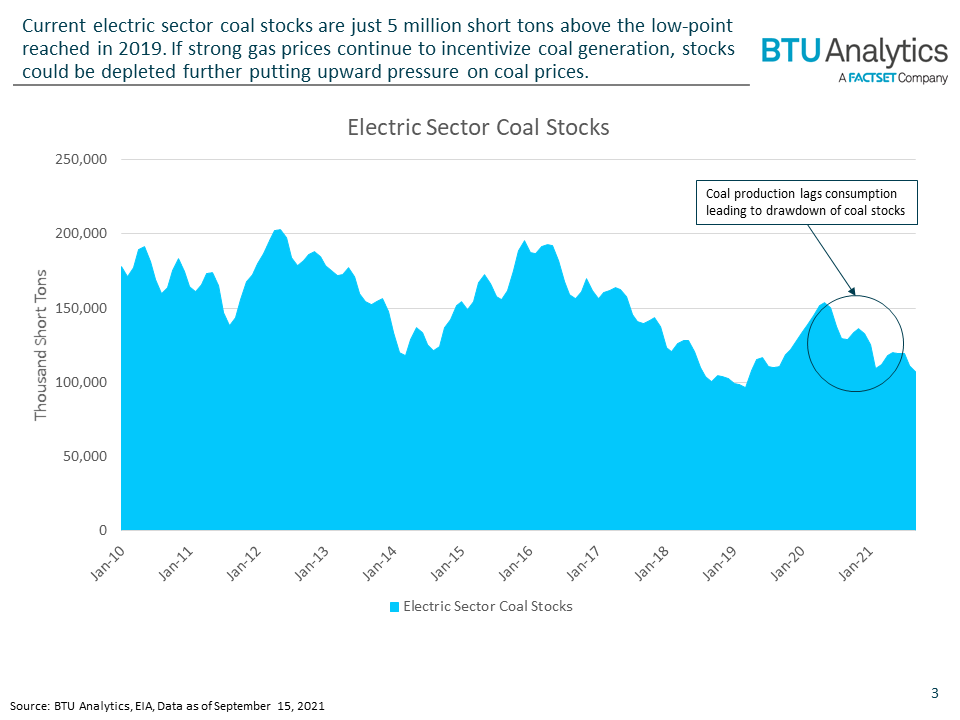

As a result of the rapid rebound in demand for coal and production lagging consumption, coal stocks for the electric power sector currently sit at 120 million short tons, only 5 million short tons higher than the low point reached in 2019 as shown in the chart below.

Coal consumption and coal production are currently at parity but the ability for US coal production to ramp significantly may be hampered going forward by many of the same forces curtailing investment in the US Oil & Gas upstream space. US coal producers have faced a decade of bankruptcy and underperforming investments as cheap US coal and US environmental policy has resulted in the closure of 100s of US coal plants and subsequently coal producers have shuttered dozens of mines to rebalance the market. Peabody Energy and Arch Resources, two of the largest US coal producers, are focused on using free cash flow on reducing liabilities due to mine reclamation, pension plans, and debt rather than expanding mining operations at a time when the future of US coal seems bleak. Additionally, boosting utilization at existing mines has been hampered by labor shortages like many of the sectors across the US.

European markets are already feeling the strain of a lack of ability to switch from natural gas back to coal with prices skyrocketing to over $20/MMbtu for the winter. Could the US natural gas market be on a similar path this winter if US coal producers fail to keep up with demand for coal? To find out more on BTU Analytics outlook for winter natural gas prices tune into our webinar on Thursday, September 23 REGISTER HERE or request a trial of our Henry Hub Outlook service.