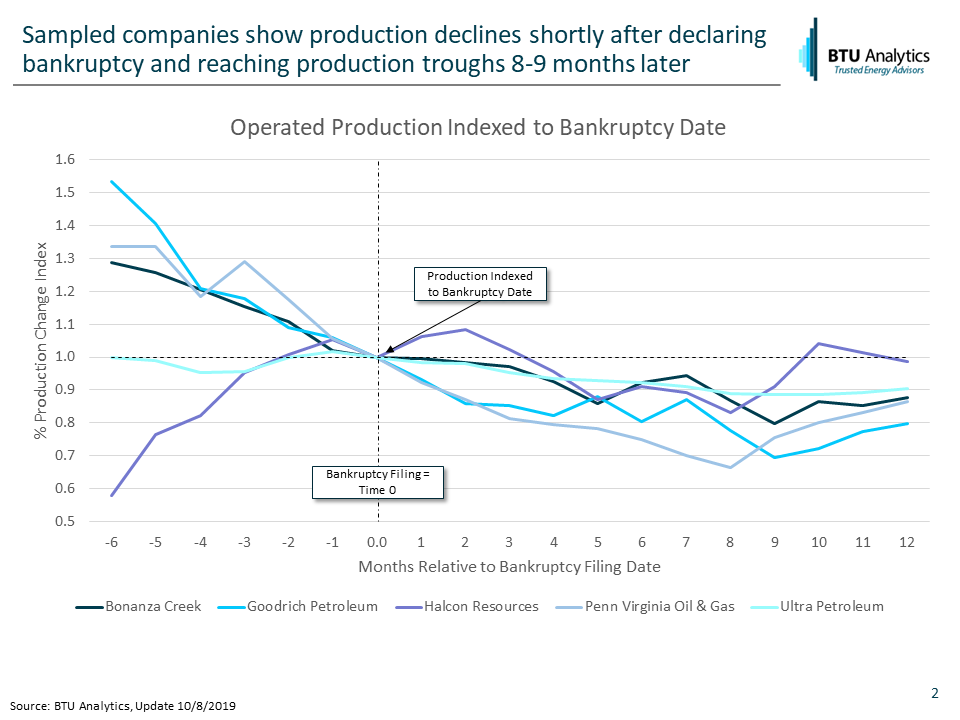

Bankruptcy continues to plague the oil and gas patch. EP Energy became the latest victim to low prices and filed for chapter 11 protection late last week. According to Haynes and Boone, over 30 North American companies have declared bankruptcy through September 2019. As pricing outlooks for oil and gas remain challenged and Wall Street continues to pressure operators to maintain capital discipline, many producers continue to be caught between a rock and a hard place. Without improvement in oil or gas prices, more potential bankruptcies loom and could impact the trajectory of US oil production. A sample of five companies shows that following filing for bankruptcy, production declines, and not an insignificant amount. Most of the operators go into PDP (Proved, Developed, Producing) declines. As highlighted in “Do Shale Base Decline Rates Have Producers on the Ropes?”, PDP base annual decline rates range from 35% to over 50% across key US shale plays. While base decline rates will also vary by operator, if more and more producers go into bankruptcy, the growth trajectory for US production could stall.

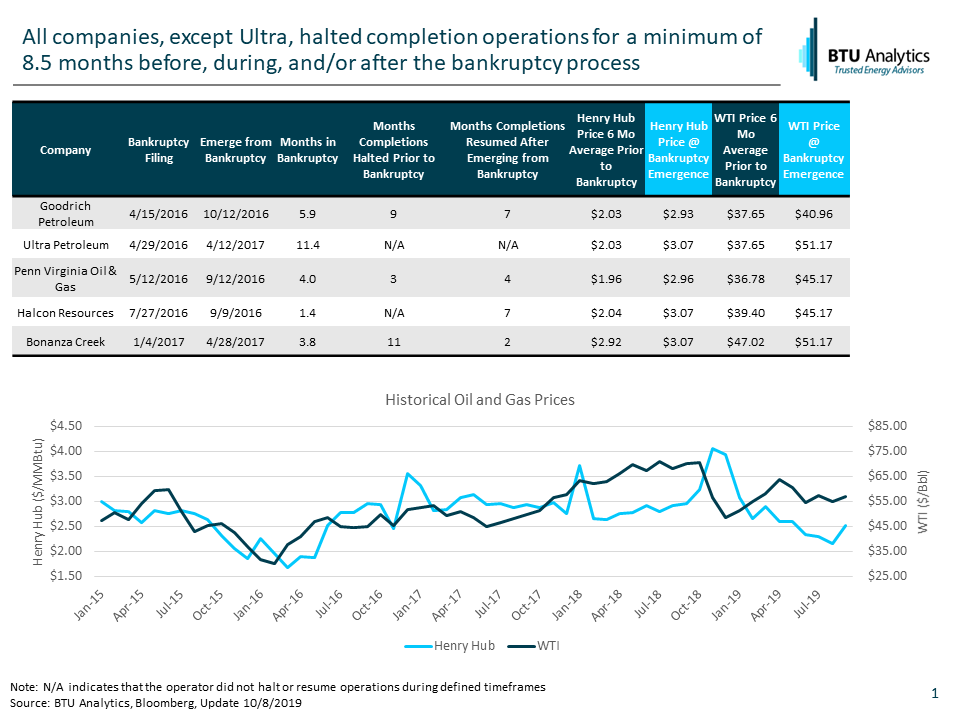

A sample of five companies who previously declared and then emerged from bankruptcy shows that all companies halted or significantly slowed completion activity for some period either before, during, and/or after filing for bankruptcy. However, the period of halted completions ranges significantly. In 2016, Goodrich Petroleum halted completion activity for 8 months before declaring bankruptcy. Then, following bankruptcy, maintained no activity for 13 months, resulting in no completions for a total of 21 months. On the other hand, Ultra Petroleum never halted completions but did slow activity significantly throughout the bankruptcy process.

However, in all cases, the impact of halting and decreasing completions before and after bankruptcy resulted in declining production for at least eight months after filing, as shown below. From bankruptcy to trough production, declines ranged from as low as 12% for Ultra and as high as 33% for Penn Virginia. For producers who are already struggling to generate cash flow to meet debt obligations, declining production only exacerbates the problem – lower production means lower overall revenue from commodity sales. The only way to stem the production declines is to increase drilling and completion activity. However, increasing activity requires more capital expenditures and cashflow. Thus, putting producers’ backs against a wall in the currently weak pricing environment.

As EP Energy and others continue to navigate bankruptcy and difficult pricing in 2019/2020, could a reversion to base declines by these companies slow the overall US oil and gas production outlook more than expected? Will prices recover in time to save those on the brink? For more information on operator economics and price forecasts, request a sample of our E&P Positioning Report.