n October 1st the Pipeline and Hazardous Materials Safety Administration (PHMSA) finalized new rules for natural gas pipelines that have been in the works since 2011. The new PHMSA pipeline rule has expanded the segments of pipes that require periodic inspections, beefed-up reporting and record keeping guidelines, and asked operators to reconfirm their pipe’s maximum allowable operating pressure. Maintenance, especially unexpected maintenance, can cause prices to jump as recently seen in Algonquin pricing with Enbridge’s announced maintenance. That got us thinking: over the long term what pipes are most at risk as inspections and potentially maintenance due to PHMSA ramp up?

A boom in production thanks to the advent of horizontal drilling and hydraulic fracturing and public/political opposition to new pipe have put stress on the US’ aging natural gas infrastructure. The result has been that aging pipes are pushed harder and harder. Looking at a selected group of 25 major gas transmission lines representing about 140,000 miles of operational pipe shows that the average age of pipe operating in 2018 was 49.5 years.

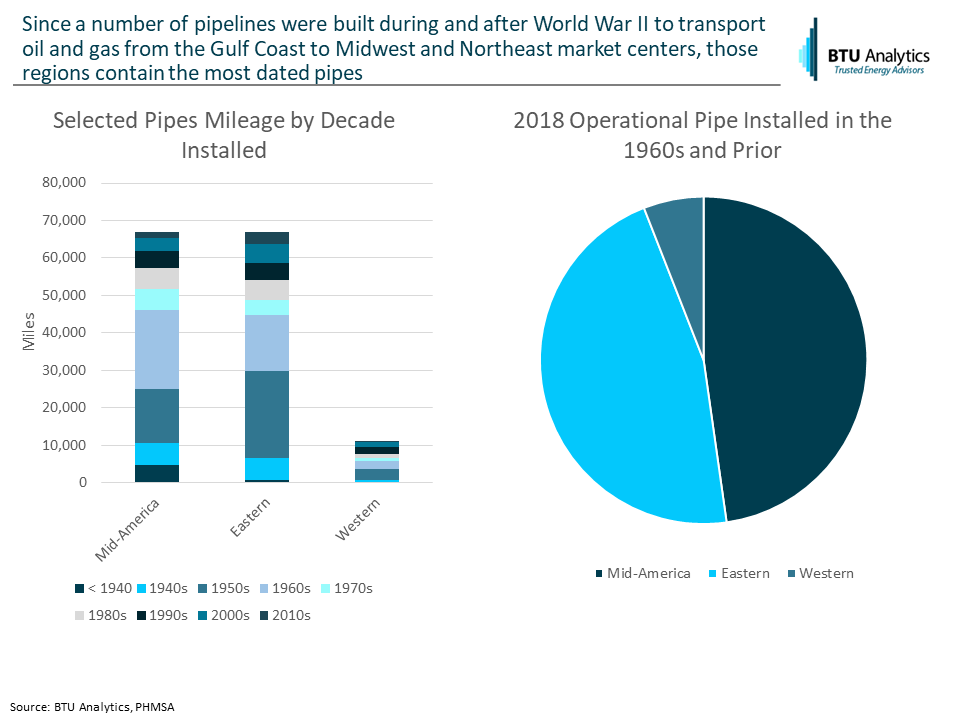

Taking those 25 pipes and segmenting them into three broad regions shows that the much of the oldest pipes in the US are operating in Mid-America and the Eastern US. Probably not big surprise as much of this infrastructure was built during or after World War II to move oil and natural gas supply from the Gulf Coast to market centers like Chicago and New York. For example, TETCO was once comprised of two oil pipelines, Big Inch and Little Inch, built during WWII, then converted shortly after to natural gas service.

Obviously, a lot has changed since World War II. For the most part over the past 15 years, the US has set new gas production records. While new pipes like Gulf Coast Express, Rover, NEXUS, and Atlantic Sunrise have facilitated some of this recent growth, existing pipes in the ground have carried their share of the burden as well.

With the growing importance of getting gas to the Gulf Coast, especially in preparation for Wave 2 LNG export facilities (see our recent study, Getting to the Gulf), any interruption in supply could have far reaching effects as export facilities have to utilize different sources of supply in the case of an outage. Nothing is expected to change overnight. Operators have until 2028 to inspect half of the required mileage. The remaining mileage must be inspected by 2035. Meanwhile, any potential outages or required maintenance will have implications to production potential, basis prices, and how demand sources natural gas supply. For other factors driving long-term gas supply see our Long Term Gas Outlook.