Investment in supply continues to dwindle and as producers of coal and gas go bankrupt, the ability for North American supply, in the short run, to respond, becomes more limited day by day. One of BTU Analytics’ fundamental thesis going into 2017 and 2018 is that the drop in drilling activity, due to sub-$50 oil prices, will consume the majority of the backlog of drilled and uncompleted wells and ultimately reduce natural gas production from liquids plays. Concurrently, growth in demand continues to swell following the completion of new pipelines to Mexico, LNG facilities’ ramp up, power plants converting from coal to natural gas, and industrial projects consuming methane and ethane to make plastics, fertilizers, and fuels. If the supply and demand dynamic is swinging in favor of the natural gas producer, it should also be swinging in the favor of the US Coal producer as higher natural gas prices should reduce the competition in the existing generation stack. However, can coal producers really respond if electric generators determine that coal, not natural gas, would be the preferred feed-stock to generate megawatts in the short run?

To delve into this issue, we wanted to better understand how coal production dynamics really changed over the last 7 years as a combination of regulatory and pricing pressures have pushed coal production lower year after year. Utilizing MSHA mining statistics and reported production on a mine by mine basis, we reviewed the status of coal mines across the country through the 4Q2015. Mines can be lumped into 3 primary groups: active, non-producing or idle, and abandoned. Mines are considered to be in temporarily idled status when the work of all miners has been terminated and production related activities has ceased. The mine still has recoverable reserves, it is anticipated that this is a temporary condition, and the mine will reopen in the future. This category includes mines that do not maintain ventilation or conduct underground examinations. The only activity at these mines would be security checks, visual examinations of surface areas to determine conditions, or surface activity due to another agency’s requirements (e.g. state environmental agency).

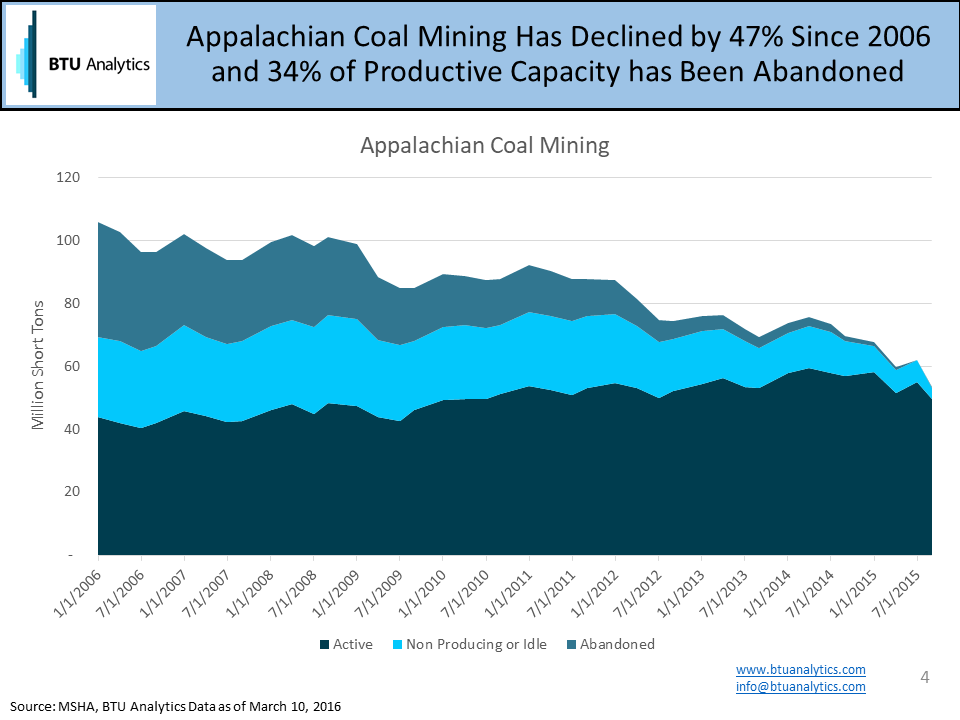

As show in the chart below, Appalachian coal production has declined nearly 47% since 2006, but production from mines active today has actually increased over time as the remaining coal mines boost production to stay competitive with low natural gas prices in the Marcellus and Utica. Of greater importance though is that nearly 47% of the productive capacity as of 2006 has been reported as abandoned to MSHA and would require capital and regulatory hurdles to reopen.

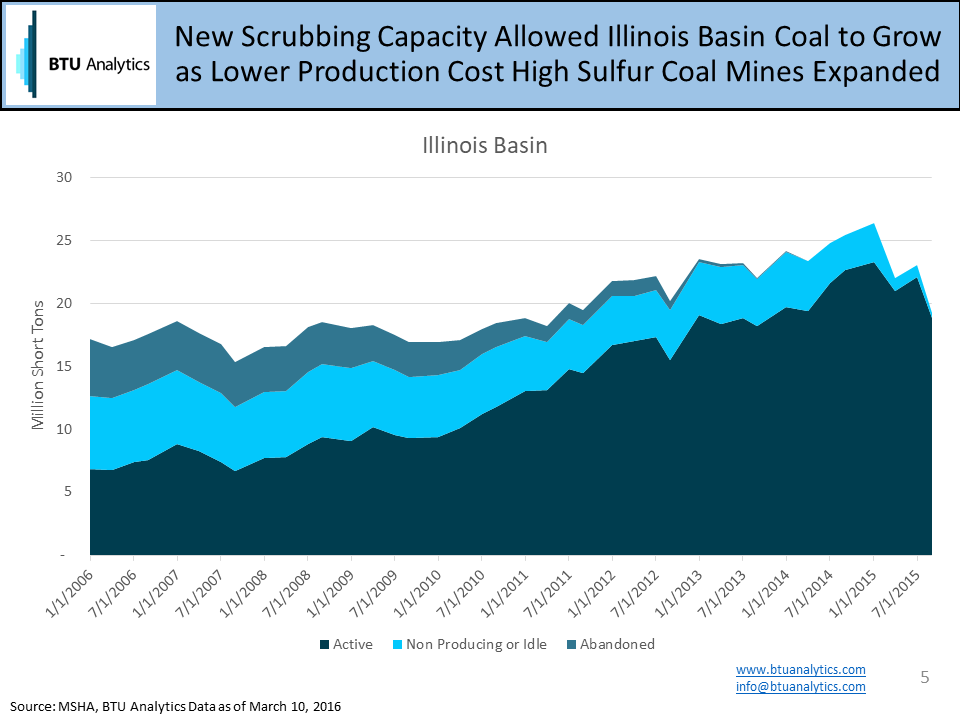

While Appalachian coal has been in steep decline with closures rampant, Western Mines have mostly managed to stay open but run at lower utilization rates. Powder River Basin coal dominates production in the West and accounts for over 50% of US coal supply. With extremely low cash costs to produce, it has been able to hold and gain coal market share against pervasively low natural gas prices.

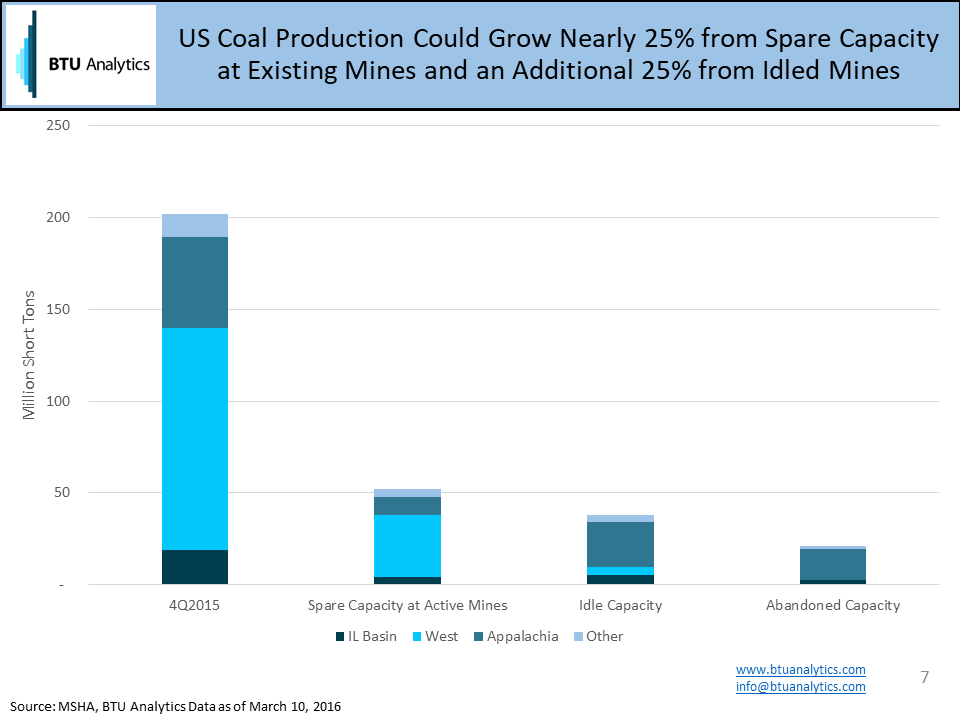

More importantly to the gas market are the structural changes in coal productive capacity. In the fourth quarter of 2015, coal production equaled 200 million short tons (MST), but currently, active coal mines had the production potential to add over 50 MST. Spare capacity was calculated based on the max quarterly production rate since 2010. Lower run rates at Western mines dropped supply as natural gas took share in the power market leading to the growth in spare capacity. Additionally, since 2010, another 38 MST of mining capacity has been idled primarily in Appalachia where cash prices for natural gas have long been below the marginal cost of coal extraction in the region. Finally, over 20 MST have mines have been abandoned or about 10% of 4Q2015 volumes.

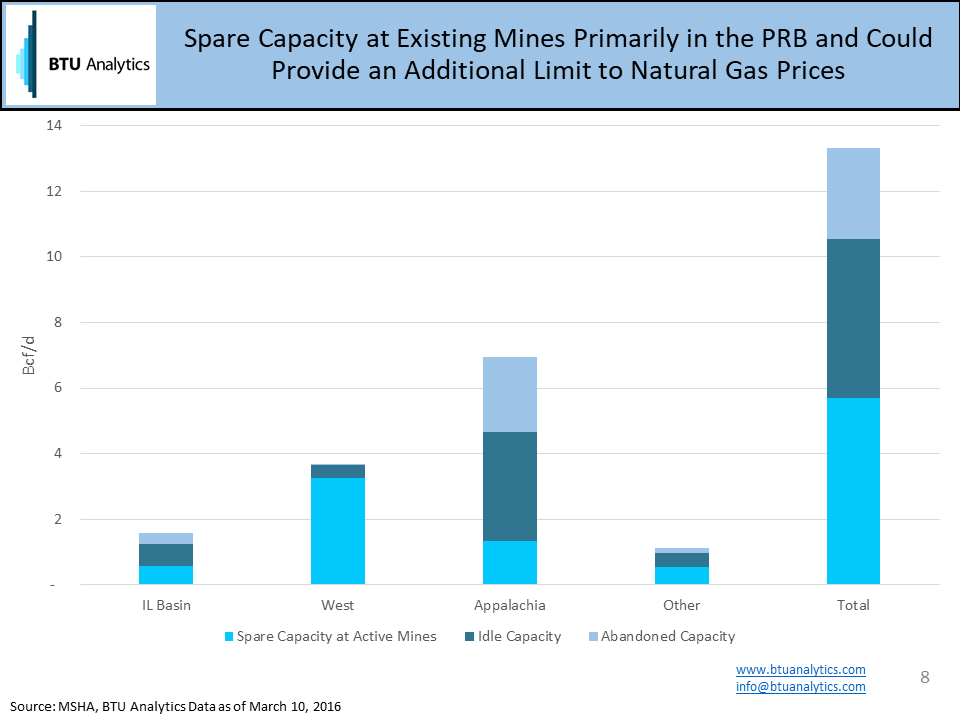

Converting all this coal production into natural gas by utilzing the heat content of the coal in each region and accounting for heat rate differences between coal fired power plants and natural gas fired power plants results in nearly 5 Bcf/d of spare productive capacity at existing and active mines. The largest region in spare capacity is in the West where surface mines could quickly ramp up production should gas prices rebound and generators increase the call on coal from the region.

The next chunk of spare capacity in the system is from idled mines, where the owners of the mines would, at a minimum, need to hire crews to bring the mines back into operation. These mines are primarily in Appalachia and could facilitate as much as 4.4 Bcf/d of switching from natural gas back into the coal market, but would require higher prices than spare capacity in the West. Lost forever to natural gas though are volumes that have been abandoned at over 2.6 Bcf/d since 2010.

While we do not expect a recovery in the coal market over the long run, as utilities and regulation continue to expand the natural gas fleet, in the short term, should the power market need coal, there is spare capacity to switch back though it will take time to ramp up production, arrange coal car logistics, and deliver coal to the generators.