California ISO (CAISO) has developed an extensive renewable energy infrastructure, positioning itself not only at the forefront of the industry but also among the first to address challenges associated with a reliance on intermittent resources. One of these challenges is curtailments, a form of energy loss that occurs when power plants generate more energy than the grid demands (or transmission allows) – often resulting in a loss of solar and wind production in regions like CAISO and ERCOT. In this Energy Market Insight, we’ll take a closer look at solar curtailments in CAISO and the factors influencing them.

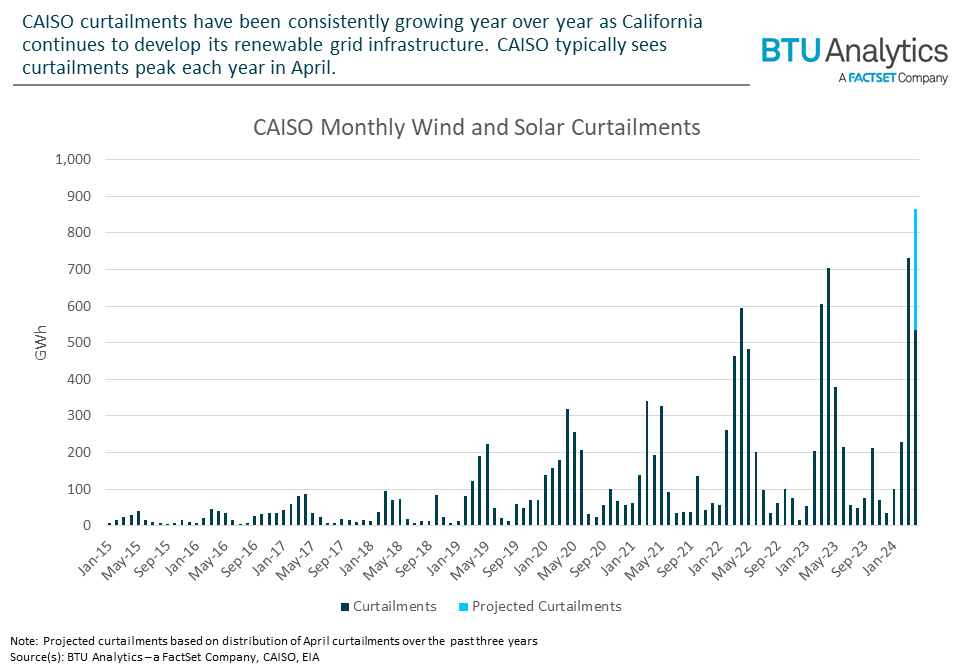

In 2022, BTU Analytics noted a drastic increase in curtailments and highlighted battery storage as a potential way to mitigate them. Since then, curtailments have shown no signs of slowing, as April 2024 is on track to be another record month at 865 GWh of curtailed solar and wind generation.

CAISO’s solar buildout has been the key driver of this trend, with 4.9 GW of new solar capacity being added over the last two years. It’s no surprise that an increase in solar capacity is accompanied by a rise in curtailments; however, the percentage of solar generation being curtailed is also increasing. Over the course of April, we’ve seen 23% of solar production curtailed. This is a steady increase when compared to previous years, when 2022 and 2023 saw 17% and 20% of solar production being curtailed, respectively, indicating that the problem is worsening.

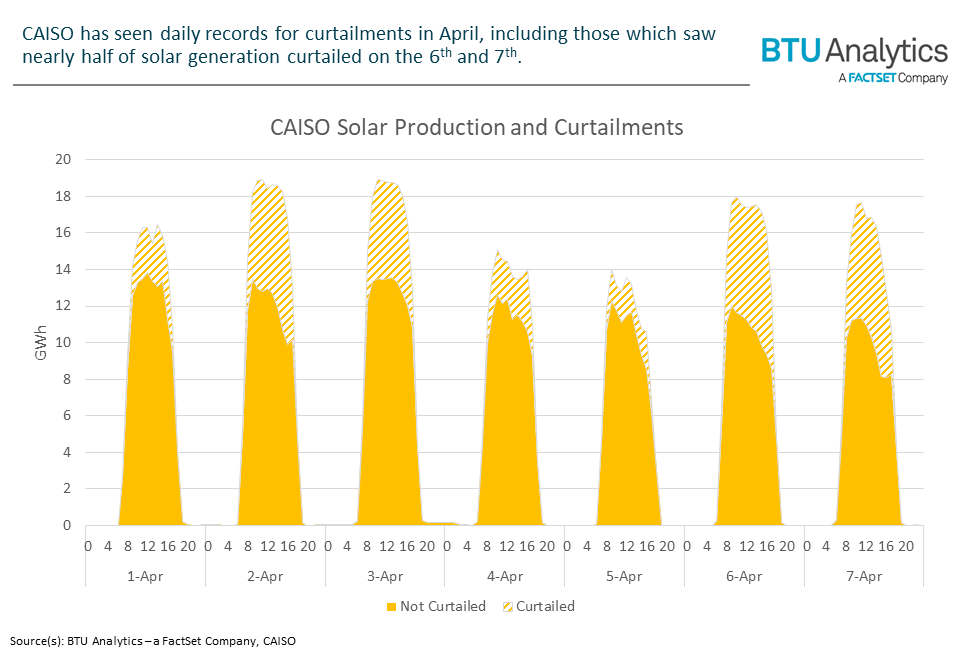

Looking at intraday curtailments, some moments saw upwards of 45% of hourly solar production being curtailed in the beginning of April. This was due in part to low load on April 6th and 7th, resulting in only two thirds of the day’s generated solar production being dispatched to the grid during daylight hours.

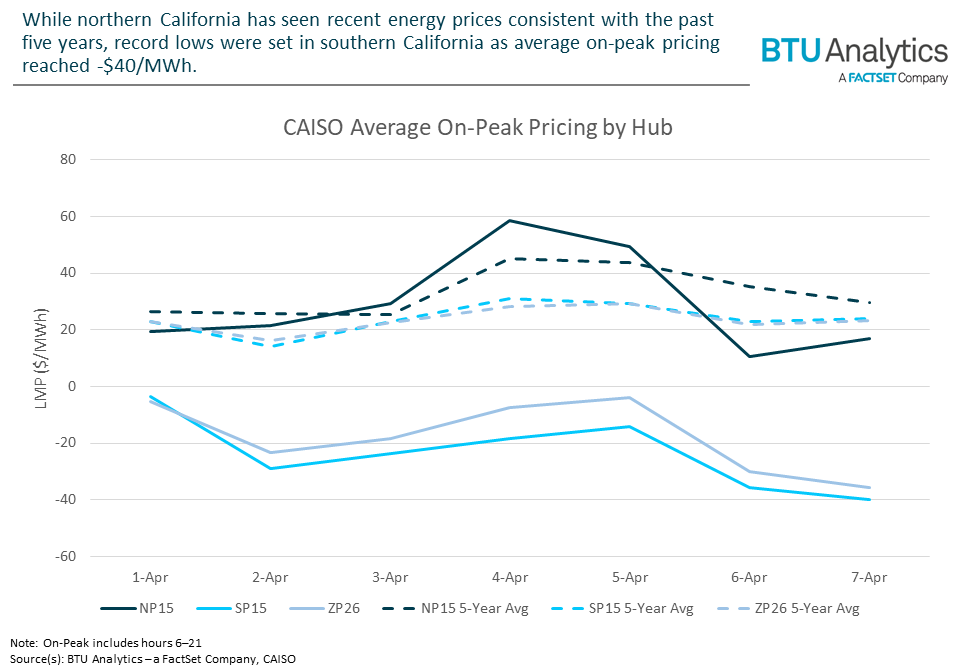

The high curtailment volumes were driven by the market conditions in southern California, which was seeing record low prices at the time. Average on-peak LMPs were around -$40/MWh on April 7th in SP15, over $60/MWh lower than the previous five-year average. The region saw a strong price disparity due to heightened congestion, as a few key transmission lines were down for maintenance, limiting the delivery of SoCal solar to NP15 and further elevating curtailments.

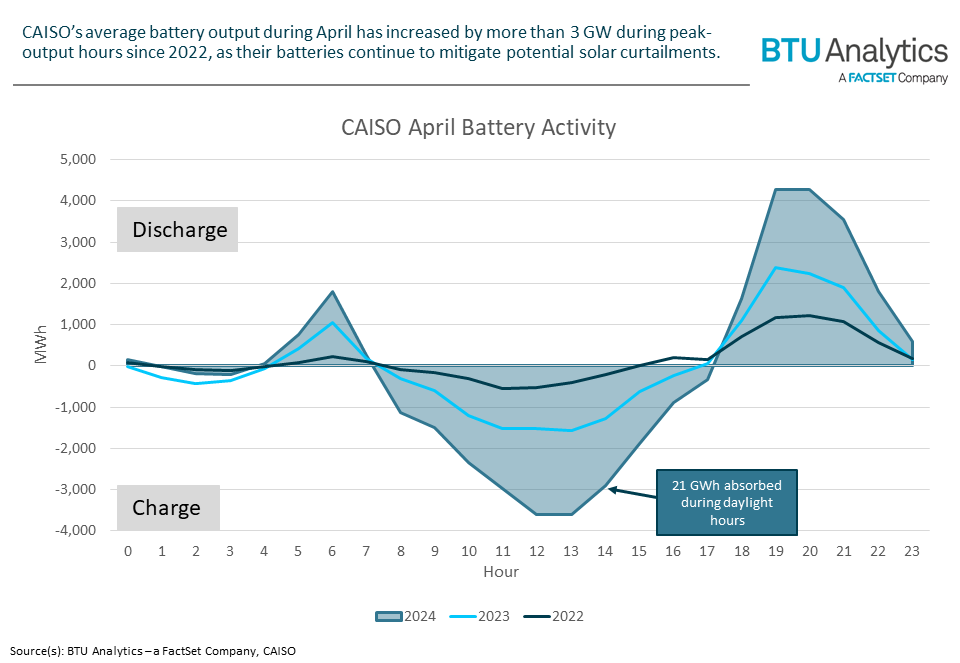

A lack of transmission capacity is a primary factor to observed curtailments. Since building new transmission infrastructure is a much slower process, battery storage has proven helpful as a near-term solution for curtailments. By absorbing excess power during periods of peak solar and then discharging that energy when demand is high, battery storage significantly lessens the amount of wasted solar energy.

While current battery storage capacity has provided some relief, it’s proven incapable of absorbing the growing surplus solar generation during peak production hours. Even so, ramping up storage assets alone will not solve the problem of getting low-cost generation out of southern California.

The challenge of curtailments lies in the distribution of CAISO solar. Most of the region’s operational solar capacity is in the south load zone, accounting for 18.8 of the ISO’s 21.6 GW. If this solar energy cannot be transported effectively to other regions that demand power, curtailments will persist. And while strategic battery storage expansion across the region effectively mitigates some curtailments, further investment into transmission infrastructure connecting northern and southern California seems necessary for a sustainable long-term solution. This would aid in scaling up the grid’s capacity to handle excess solar generation more effectively.