Last March, China released the outline for its 14th five-year plan, which featured aggressive targets for emissions intensity reduction and lower reliance on fossil fuels. Of note, the outline featured plans to reduce CO2 emissions per unit of GDP by 18% from 2020 to 2025 and reduce energy consumption per unit of GDP by 13.5% from 2020 to 2025. China aims to increase the share of non-fossil fuels in its energy mix from 15.8% in 2020 to 20% in 2025, while reaching carbon neutrality by 2060. Additionally, China made the unexpected move to shift focus away from economic expansion, dropping targets for GDP growth in its most recent plan. As China gears up to release more details on the five-year plan in late-2021 and 2022, this analysis will focus on the potential for this shift to impact oil consumption in what has been the largest growth engine for global demand.

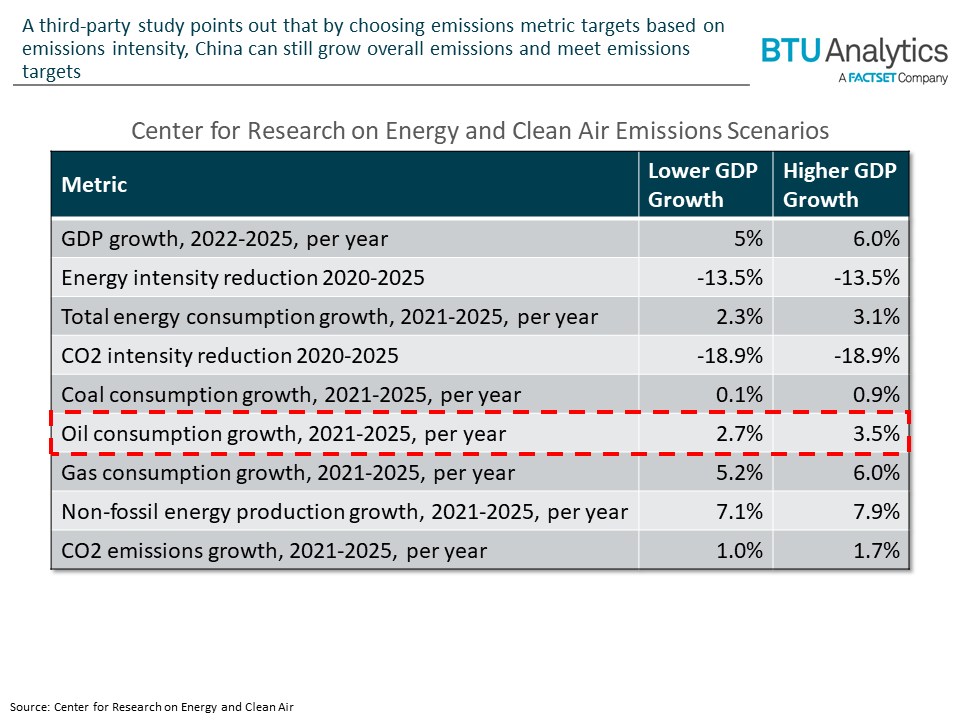

There are many interested parties investigating China’s future plans. The Center for Research on Energy and Clean Air (CREA), a research organization focused on the impacts of government legislation on air pollution, put together a study in March that concluded China’s headline reduction emissions intensity could actually lead to an increase in total emissions for years to come. This is because China’s GDP continues to grow at a rapid pace, averaging a 5.7% annual growth rate since the beginning of 2020. CREA’s report highlighted three scenarios, with GDP growth rates between 5% and 6% annually. These scenarios pointed to CO2 emissions rising by 1.0% to 1.7% each year through 2025, as shown in the table below. CREA’s conclusion was that GDP could allow oil demand in China to rise by 2.7% to 3.5% each year for the next five years.

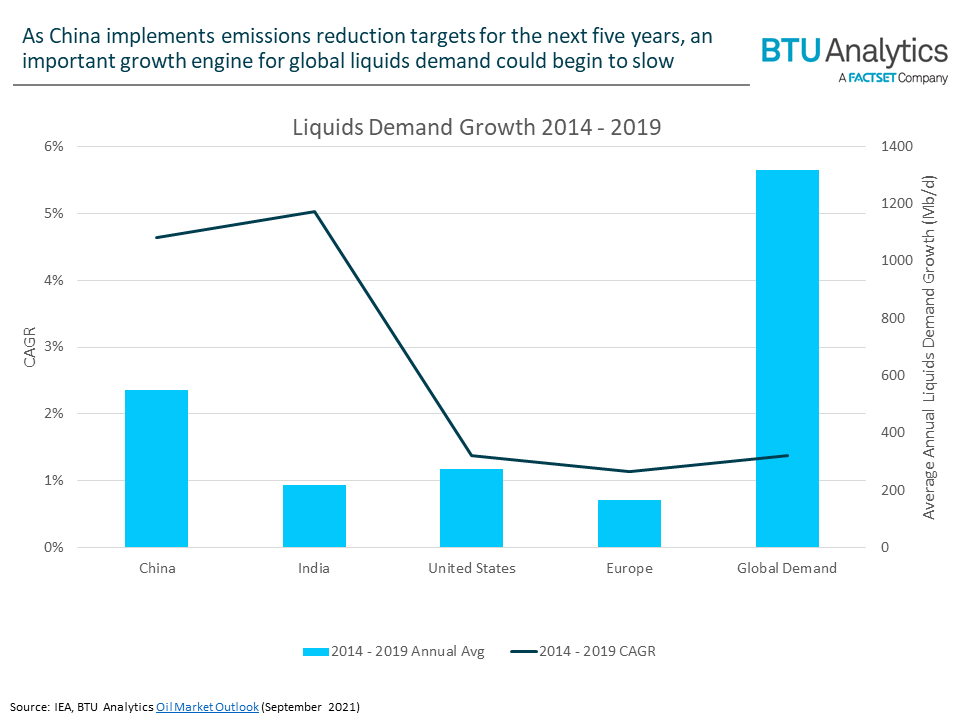

However, it is not China’s growth but rather the magnitude of China’s growth that matters to global oil demand. As highlighted in the chart below, China has been the primary driver in global oil demand along with India. In the 2014 – 2019 period immediately preceding the COVID-19 pandemic, China represented approximately 42% of the total increase in global oil demand. That equates to a 550 Mb/d annual rise in Chinese demand while all other countries have combined for just a 766 MMb/d annual increase in demand. Should that pace slow significantly in the years to come, the outlook for global demand deteriorates and likely speeds up the peak in oil demand.

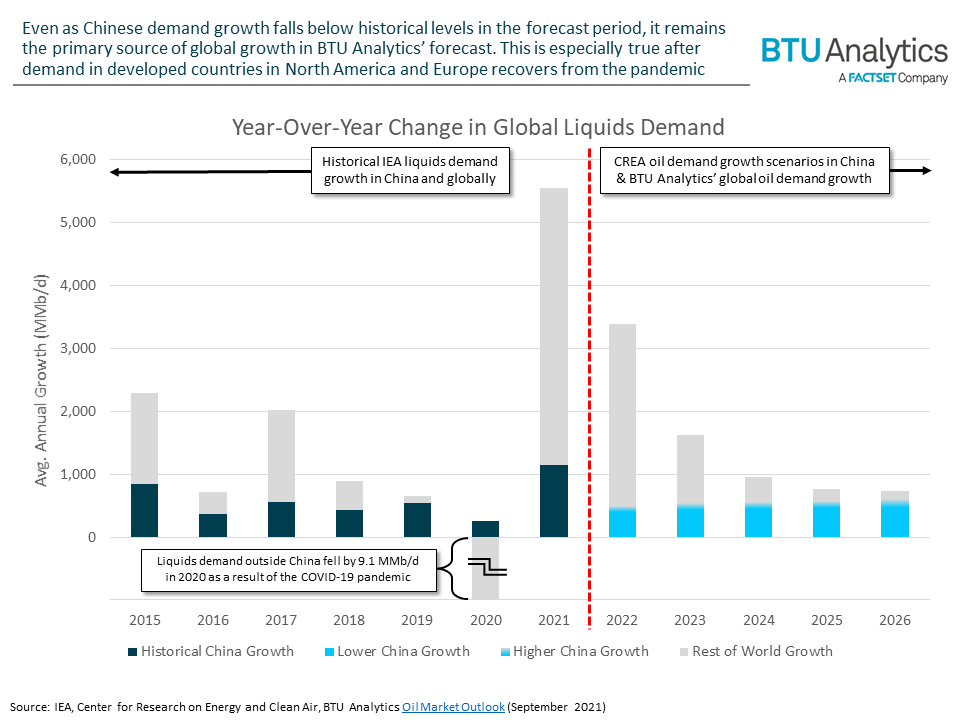

In BTU Analytics’ monthly Oil Market Outlook, global liquids demand is expected to recover back to pre-pandemic levels sometime in 2022. This is primarily driven by new growth from China, as developed countries like the US and those in Europe aren’t likely to see demand fully recover until 2023 or 2024, if at all. Beyond this recovery, BTU Analytics models that global liquids demand growth will slow significantly, falling below the historical norm of roughly 1 MMb/d of new growth each year to an average 0.75 MMb/d in 2025 and 2026.

However, the level of Chinese demand growth matters given that liquids demand growth elsewhere is expected to be limited beyond 2024. While BTU Analytics does not publish a country-level liquids demand forecast, CREA’s scenarios indicate that Chinese oil demand could grow between 431 and 570 Mb/d from 2023 to 2026. Compare that to BTU Analytics’ expected rise in global liquids demand from 2023-2026 and China would account for between 57% and 62% of global growth. It’s important to note that BTU Analytics is still expecting many developed nations to continue recovering from pandemic-driven declines in demand through 2024. When this recovery has subsided in 2025 and 2026, China could represent between 70% and 81% of global liquids demand growth.

As liquids demand growth stalls in other countries China will remain the major driver, and now a potential risk, to continued expansion in global oil demand. While not currently expected, a rapid deceleration in China liquids demand growth brings forward the eventual peak in oil demand. However, the existing plans to reduce emissions and energy intensity over the next five years will still likely allow for meaningful oil demand growth from the largest oil importer. To see how high BTU Analytics forecasts oil demand to grow in the coming years, combined with how much US oil production will be needed to satisfy that demand, request a sample of the Oil Market Outlook. Curious about the eventual peak in oil demand? Ask about our long-term oil demand forecast, which will be republished in November.