After years of legal battles, the saga of TC Energy’s Keystone XL pipeline is coming to an end. On January 20, 2021, President Biden revoked the key Presidential Permit needed to advance the 830 Mb/d pipeline’s development. While this news hardly comes as a surprise, it does leave Canadian oil producers, particularly in the prolific Alberta oil sands, with dwindling future pipeline expansion projects to relieve the highly congested pipeline network. While crude by rail can provide relief, it comes at a higher cost. Today’s Energy Market Insight will explore the outlook for Canadian oil production and future egress options for Canadian crude.

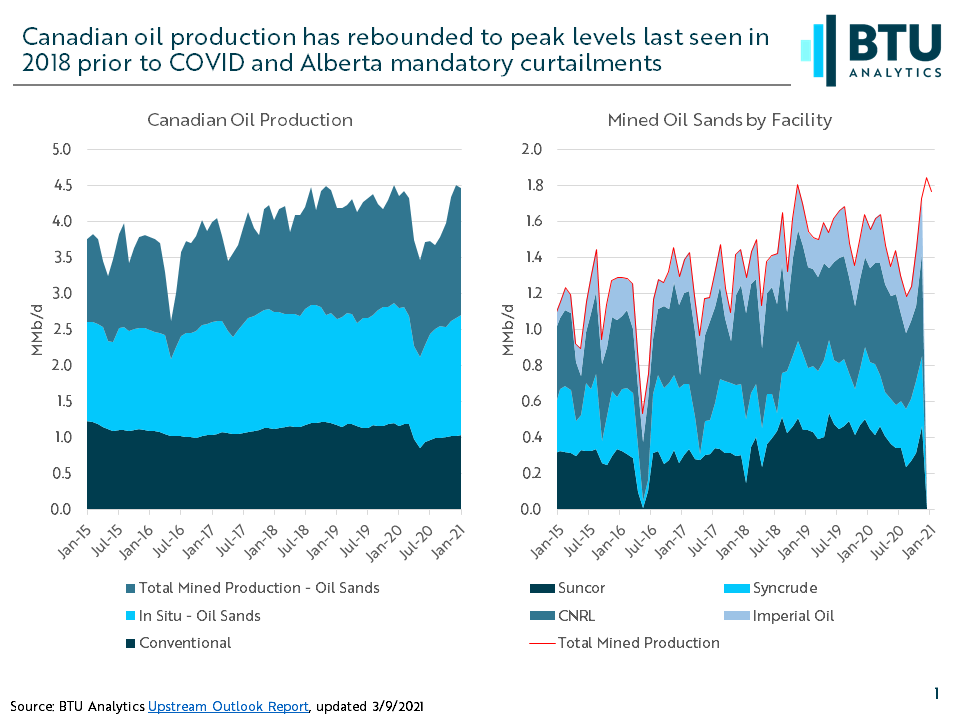

In 2021, Canadian oil production has rebounded to peak levels of 4.5 MMb/d as shown in the chart below, and has once again led to increased pipeline congestion, higher crude by rail volumes, and ultimately widening discounts of WCS oil prices to WTI.

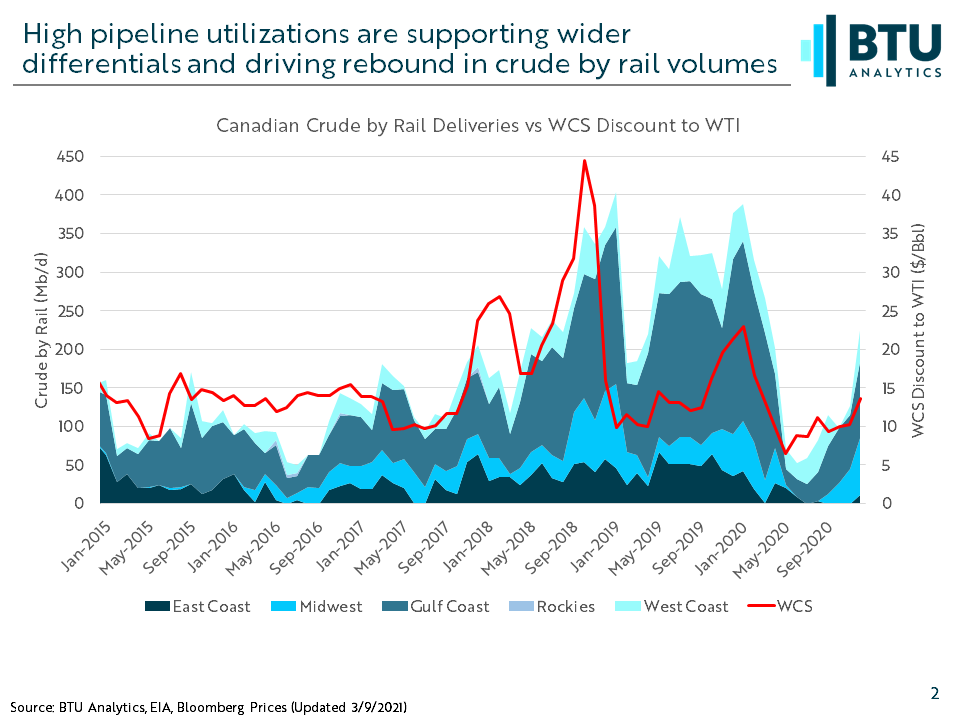

The rebound in oil production, primarily led by mined oil sands, has sent WCS discounts to WTI back to $13/bbl but is still well below the peak discounts experienced in 2018 and 2019. As a result of the widening discounts, crude by rail volumes have soared higher. The chart below highlights the increase in crude by rail volumes in response to wider discounts. However, wider discounts to WTI means lower netback pricing which hurts oil production economics and potentially future production plans.

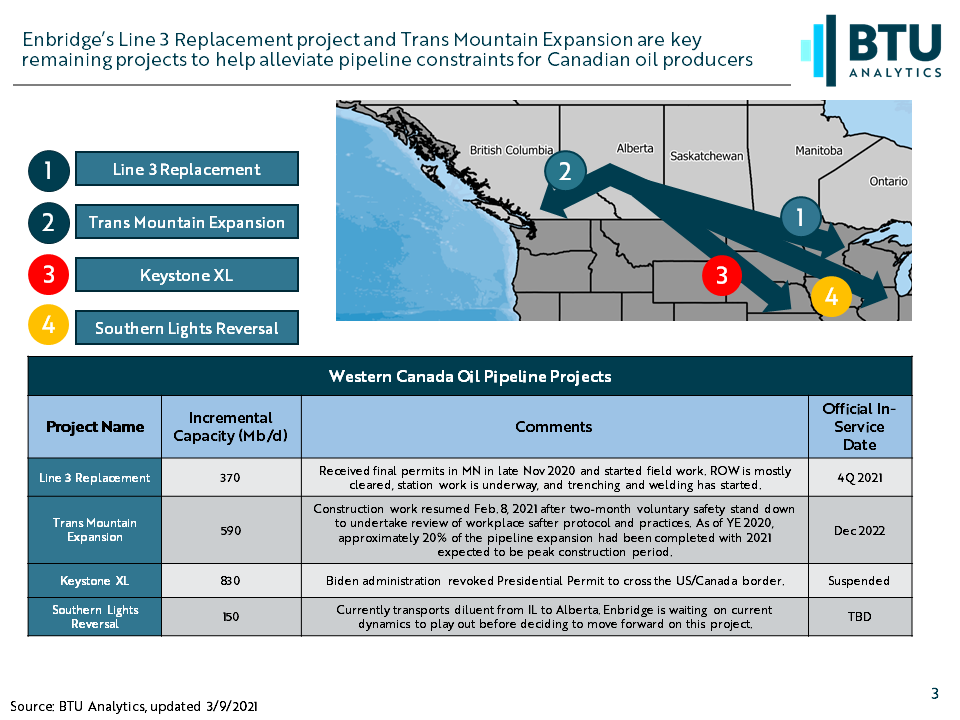

This brings us to the outlook for proposed pipeline capacity out of Canada. At one time, there was as much as 3 MMb/d of new pipeline capacity proposed to serve growing Canadian oil production, but over the years that number has dwindled due to project cancelations and suspensions, largely driven by environmental opposition. While some expansion projects have been completed, over 1.5 MMb/d of projects have been canceled, and only 1 MMb/d of projects are actively under development.

Of the 1 MMb/d of active projects, the Line 3 Replacement project proposed by Enbridge is expected to come to market by YE 2021. This project would replace an older existing pipeline that connects Hardisty, Alberta to Superior, WI. By replacing the older pipeline, Enbridge would expand the total capacity on the line by 370 Mb/d to a total of 760 Mb/d. However, this project has encountered significant opposition, particularly in Minnesota. In late November 2020, Enbridge received the final permits for this project to move forward and BTU Analytics includes this project in its Base Case outlook.

In addition to the Line 3 project, the Canadian government continues to push forward on the expansion of the Trans Mountain pipeline. This project was approved by the Government of Canada in mid-2019 and is subject to 156 conditions enforced by the Canada Energy Regulator (CER). In February 2021, the project resumed construction after a voluntary 2-month stand down to review construction safety practices and procedures. Additionally, Canada’s Federal Court of Appeal ruled favorably for the project ruling against four different challenges from First Nations groups opposing the project. While continued legal challenges are expected to ensue, 590 Mb/d expansion of Trans Mountain pipeline remains on track for operations in 2023.

BTU Analytics expects Canadian oil sands production to continue to grow over the next 5 years but the pace of that growth may be heavily moderated by the outlook for infrastructure development in Western Canada. For more information on BTU Analytics’ WCS and WTI oil price forecasts, request a sample of our Oil Market Outlook report.