Oil volatility continues to give the market fits and starts. Over the last four weeks, the market has seen a number of bullish and bearish pricing signals. On the bullish side, mother nature and unrest challenged global oil production in June. Oil supply disruptions in Canada, the Middle East, and Nigeria took nearly 2.5 MMBbl/d of supply offline at the peak. In response, WTI and Brent prices set new 2016 peaks of $51.23/bbl and $51.33/bbl, respectively on June 8, 2016.

On the bearish side of the equation, producers continue to clean up balance sheets and deploy incremental cash flow into the field. As a result, the US rig count has increased for six consecutive weeks. As early as February 2015 in our Upstream Outlook, BTU Analytics estimated drilling activity would bottom in the July 2016 time frame. Our call on the bottom was driven by our outlook for supply and demand bringing oil markets into balance. However, we underestimated drilling declines before the market hit bottom. Saudi Arabia, Iran, and Iraq production gains tipped the balance far more than both BTU Analytics and the market was expecting at the time. The extended pain in the oil patch though has forced producers and capital markets to focus on cleaning up balance sheets and, in the most dire of cases, wiping the slate clean.

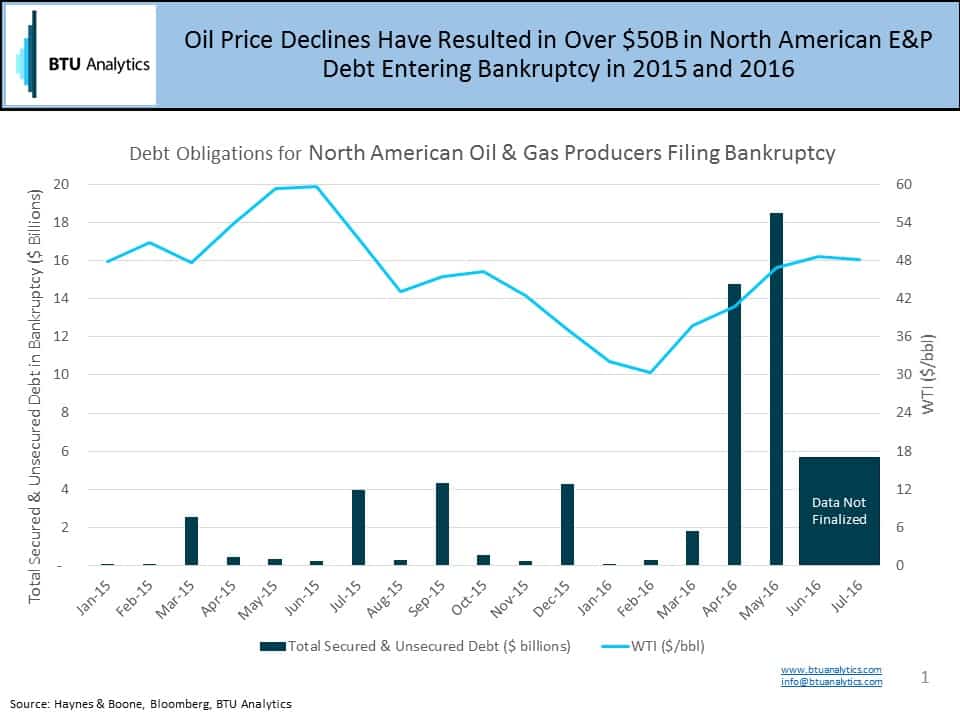

Where drilling activity and ultimately oil prices go from here will be determined by how rapidly producers can continue to clean up their balance sheets through debt exchanges, equity raises, and unfortunately for some, bankruptcy. According to the latest data from Haynes & Boone, E&P bankruptcies from January 2015 through May 2016 totaled more than $50 billion. Additional bankruptcies occurred in June and July.

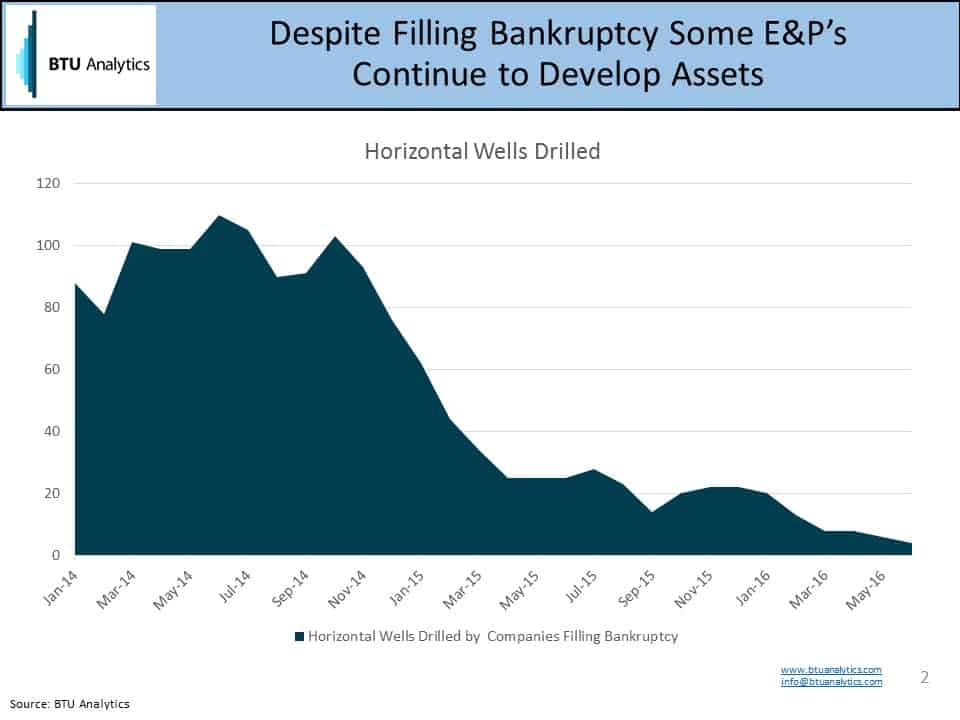

The chart below highlights horizontal wells drilled by companies who filed bankruptcy in 2015 and 2016. As bankruptcy filings accelerated in 2016, horizontal drilling ground to a halt. However, many of these companies had already stopped drilling as cash flow dried up in early 2015. Not all companies have stopped drilling though. Sandridge Energy continues to develop an oil play in the North Park Basin of Colorado drilling 2 horizontal wells per month in May and June. Similarly, Midstates Petroleum and Chaparral Energy have continued to develop plays in the Mississippi Lime and Woodford despite filing bankruptcy in April and May.

With the drag debt burdens accrued before the price crash eased, producers emerging from bankruptcy have more cash flow available to maintain or increase activity. A bearish signal for the market. Combining a clean balance sheet with increased cash flow from higher prices, the market should continue to see North American producers ramp up activity through the end of year. For detailed analysis on both the bullish and bearish factors creating oil market volatility, request a copy of our monthly Upstream Outlook.