Environmentalists and other groups have been fighting for years to limit the buildout of pipeline infrastructure in the US. The cancellation of Keystone XL and Atlantic Coast Pipeline are two recent successes in the effort to block new pipelines. However, activist groups are also placing increased pressure on existing infrastructure to be shut down. Last month, BTU Analytics highlighted the potential impacts of a forced shutdown of the Dakota Access Pipeline. While the major risks of that shutdown have since been removed, another important crude oil conduit could face a forced closure: Enbridge’s Line 5. Back in November, Michigan Governor Gretchen Whitmer ordered the line to shut by May 12th, arguing that it posed immense risk of spilling oil and refined products into the Straits of Mackinac, which separates Lake Michigan and Lake Huron. Today’s Energy Market Insight will focus on the potential impacts of a Line 5 closure, including which pipelines may benefit from the closure.

Enbridge’s Line 5 is a 540 Mb/d pipeline that moves oil and refined products from Superior, WI to Sarnia, ON, with additional delivery throughout Northern Michigan. The line serves as one of the primary connections for Western Canadian crude to reach refineries in Eastern Canada. However, the line also provides key delivery of products like propane, gasoline, diesel, and jet fuel throughout Michigan. Last November, Governor Whitmer decided to revoke and terminate the 1953 easement that allowed the Enbridge line to operate under the Straits, arguing that Enbridge violated terms of the easement regarding stretches of unsupported pipeline and mandates on pipeline coatings. Enbridge announced in its earnings call last week that it planned on defying the order, stating that the line is still the safest mode of transportation for crude in the region.

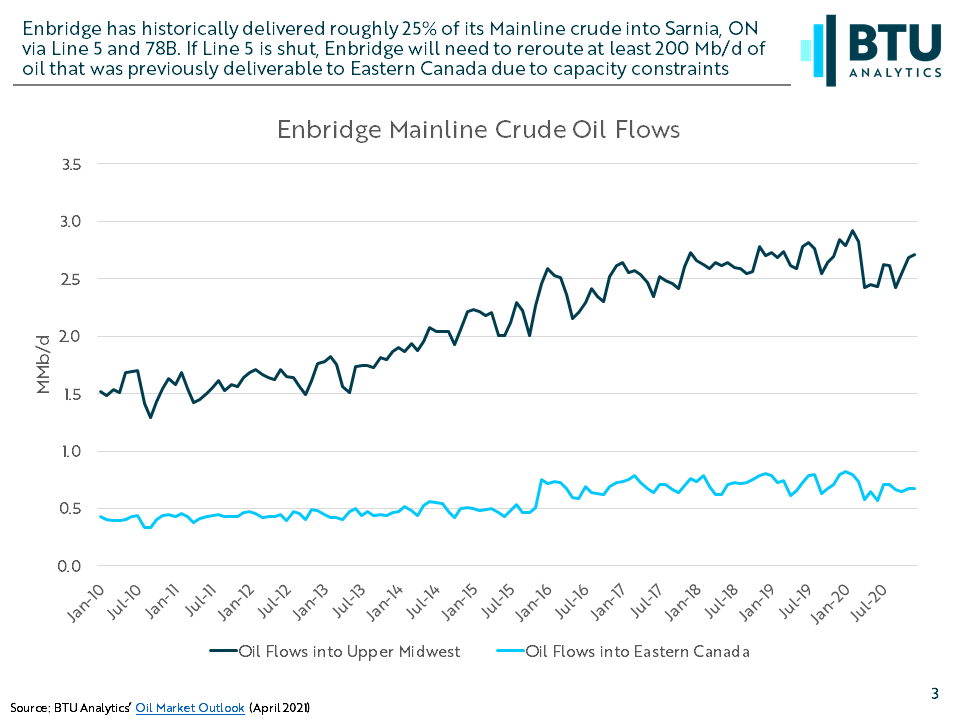

As highlighted in the chart above, Enbridge’s Mainline system serves as the largest source of crude into the Upper Midwest, specifically into Superior, WI, delivering an average 2.7 MMb/d in 2019 and 2.6 MMb/d in 2020. From there, crude can flow one of three general directions. First, crude can flow east through Northern Michigan on Line 5 to terminate in Eastern Canada. Second, crude can flow south towards Flanagan, Illinois and then Northeast on Line 78A & 78B to terminate in Eastern Canada. Third, crude flows further south from Flanagan on other Enbridge lines to Patoka, IL or Cushing, OK. Roughly 25% of Canadian mainline volumes are typically delivered to Eastern Canada via either Line 5 or Line 78B. The two lines have averaged 704 Mb/d of volume over the last two years on a combined capacity of 1,040 Mb/d. Should the 540 Mb/d Line 5 be shuttered, Eastern Canada will need to source at least 200 Mb/d of crude from non-Enbridge sources (most likely seaborne imports), not to mention the propane, gasoline, and other products that are delivered throughout Michigan.

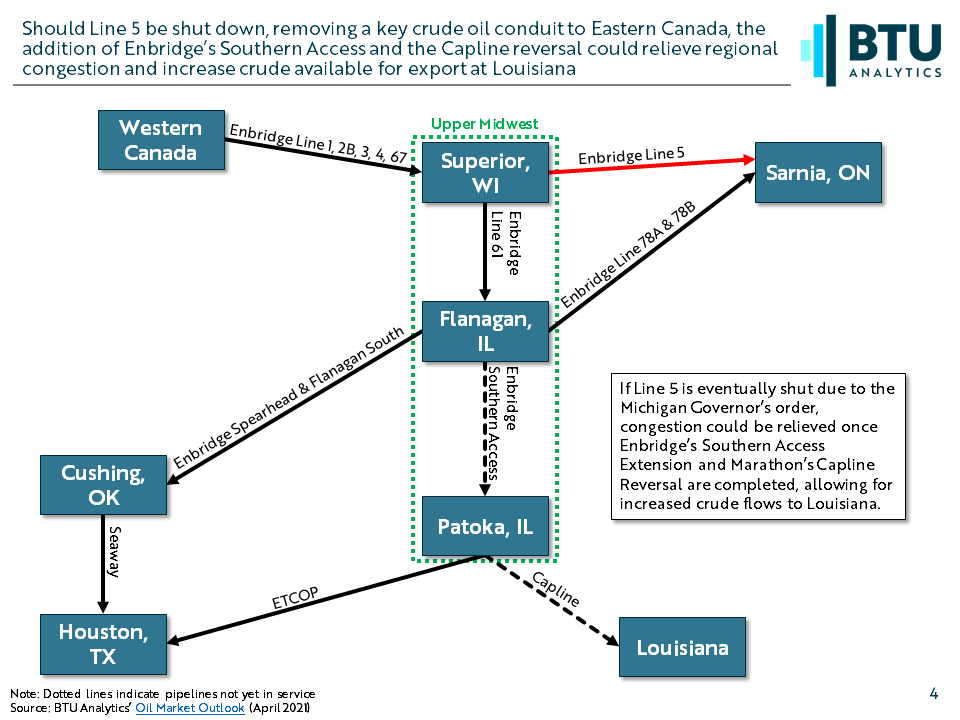

The 200 Mb/d of crude that can no longer flow into Eastern Canada will need to go somewhere. The most likely candidates are a combination of Enbridge’s existing and planned pipeline infrastructure. Enbridge’s Line 3 Replacement project is set to enter service by the end of 2021 and increase flows into the Upper Midwest. At the same time, its Southern Access Expansion project will enter service, adding another 300 Mb/d of delivery between Flanagan, IL and Patoka, IL. This is important, as the additional Patoka access could deliver increased volumes to Capline (not owned by Enbridge), which is expected to complete its reversal project early next year. Enbridge would also have access to ETCOP, which it has an ownership stake in, though the pipeline typically only flows Bakken barrels. Outside of Southern Access, Enbridge could also increase shipments to Cushing via Spearhead and Flanagan South, which have roughly 50 to 150 Mb/d of unused capacity at any given time. These could then be routed to the Gulf Coast via Seaway, which Enbridge also owns a stake in.

Thus, a Line 5 closure would likely result in more Canadian crude volumes ultimately reaching the US Gulf Coast at the expense of the Eastern Canadian crude market. Currently, a Line 5 closure at this juncture still faces many hurdles. Enbridge has vowed to defy the order while it participates in court-ordered mediation. Additionally, Canada could potentially invoke the never-before-used Transit Pipelines Treaty from 1977. The treaty is designed to discourage either government from impeding the flow of oil and gas across borders outside of an emergency. However, a shutdown would upend Midwest and Eastern Canadian refining markets while also creating opportunities to ship additional crude towards the Gulf Coast. To see how BTU Analytics models crude oil flows across the US and Canada, as well as regional price forecasts, request a copy of the Oil Market Outlook today.