This commentary was contributed by Tom Abrams from FactSet where he is a Sector Content Expert with over 30 years experience in the investment business.

The International Energy Agency’s (IEA) annual global emissions report released Friday showed the expected uptick in emissions in 2021 due to the economic recovery of last year. The question was “how much?”. This article looks at their overall findings, looks at some of the interesting dynamics behind the top-line numbers, and offers some broad expectations for what to expect in 2022.

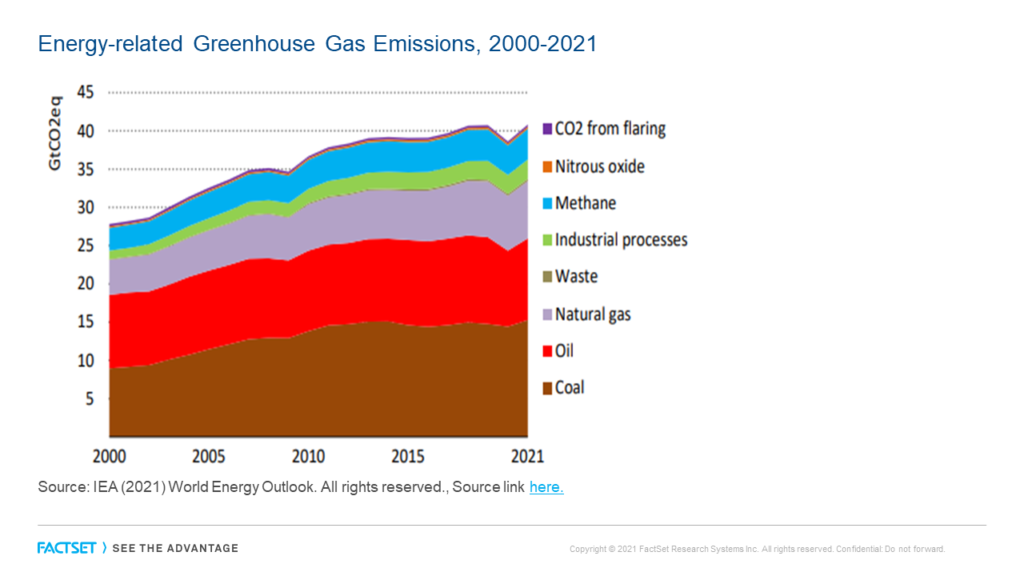

The Report The IEA’s 2021 global CO2 emissions report found that 2021’s economic recovery from pandemic-impacted 2020 was strong enough to lift CO2 emissions to a record 36.3 Gigatons (Gt) and total greenhouse gas emissions to a record 40.8 Gt. This conclusion was anticipated in direction and in magnitude by the market, in our view, though clearly supports ongoing concerns about our ability to reduce emissions enough to avoid significant climate impacts.

Why it’s important As gigatons of CO2 equivalents (including methane, nitrous oxide) or greenhouse gases (GHG) are added to the atmosphere, science suggests that the concentration will have a growing impact on global temperatures. The argument goes that if we can slow or even reverse the amount of CO2 added each year, we can push out or avoid reaching critical CO2 and hence temperature levels.

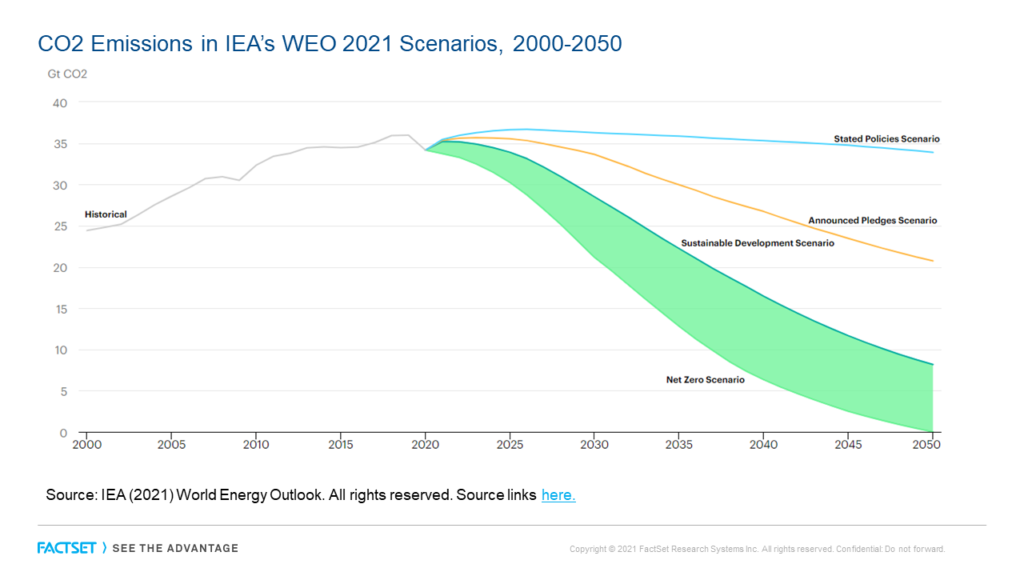

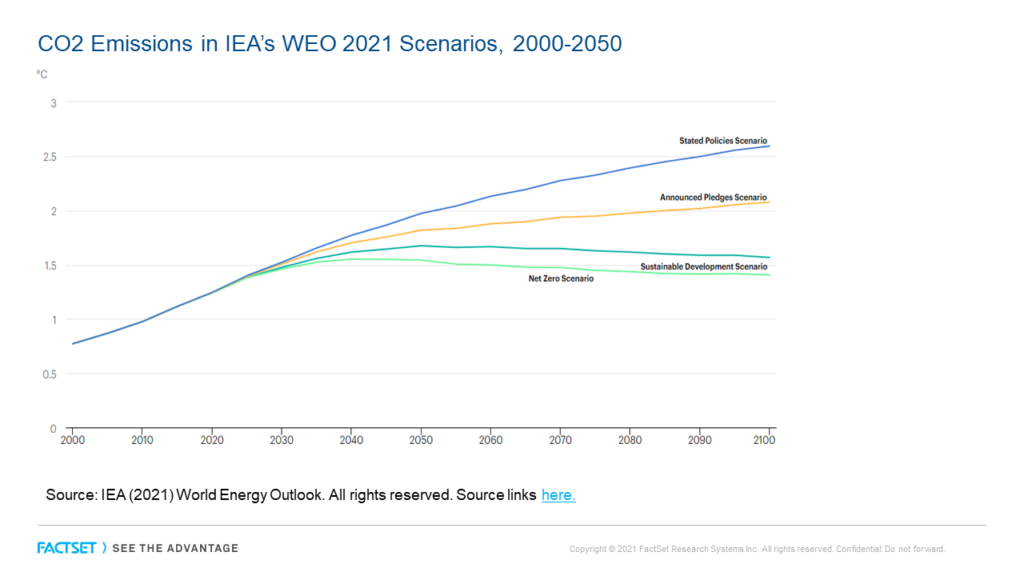

What the world has pledged to do is more than what we have actually planned to do but both are significantly less than what the IEA and other agencies calculate we need to do to achieve a sustainable or net zero scenario. An IEA outlook, based on policies as of October, 2021, shows aggregate fossil fuel demand slowing to a plateau in the 2030s and then falling slightly by 2050. In this scenario, the vast majority of the net growth in energy demand to 2030 is met by low emissions sources. Nonetheless, the global average temperature increases beyond the 1.5 degree Celsius target level around 2030 and would still be climbing as it reaches 2.6 °C in 2100.

Tracking the amount of CO2 added each year is in many ways a more tangible target for people to focus on in their day-to-day than amorphous temperature changes 20-30 years from now so we like to keep an eye on emissions. Emission reports, too, as a leading indicator of climate change, may also suggest heightened risk perceptions for hydrocarbons, which in turn could motivate policy and perhaps even demand behaviors thus changing long-term demand curves.

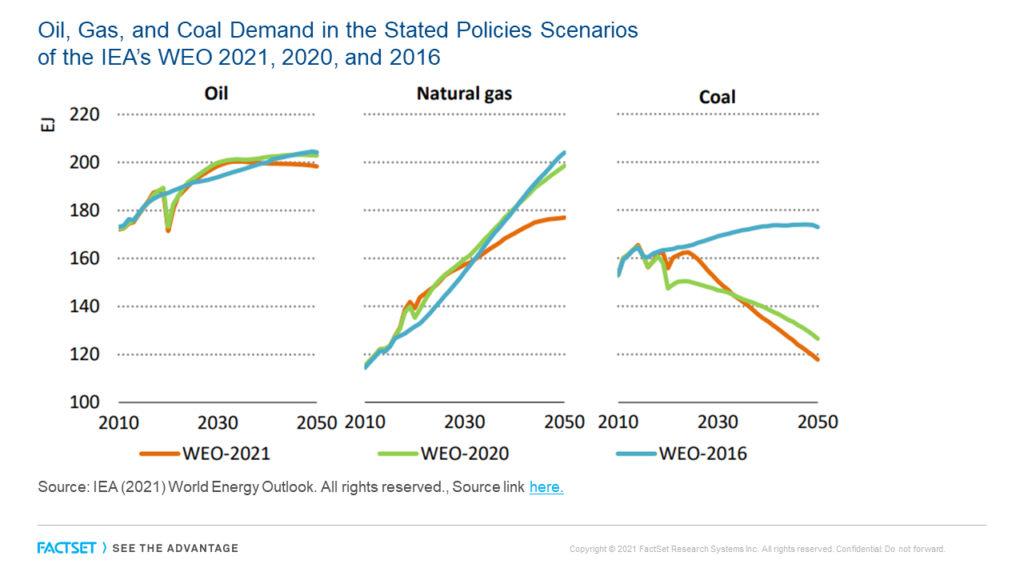

Forecasts of emissions have embedded forecasts of oil, gas, and coal demand. The future demand curves matter for long term producer volumes and the risk of both stranded assets and/or any hope for growth to be reflected in an equity multiple. For this reason we show the shift in the IEA’s oil, gas, and coal demand curves as of 2016, 2020, and late 2021.

Behind the Numbers There were severalmoving parts behind the IEa’s overall increase in 2021 emissions that were of note, some of which were positives and some of which were either negatives or spoke to issues that our energy systems face.

- Renewables growth. The amount of global electricity generated from low emission renewables and nuclear was higher in 2021 than from coal for the second year. The IEA put renewables-based global power generation at more than 8,000 TWh. The high growth of newly installed renewable power generation was able to offset the increase in coal generation but not enough to offset the increase in coal emissions, however. With expectations of additional renewables and fewer coal plants in time, emission growth from the coal/renewable tradeoff should diminish.

- Transportation lagged the recovery. In the 2021 economic recovery, coal and gas for power generation rebounded more rapidly than the transportation area where 20221 fuel use, primarily oil, remained below 2019’s pre-pandemic levels. An anticipated recovery in 2022 transportation markets at a catch-up rate perhaps faster than the power sector could mean a higher contribution to emissions this year from this sector.

- Negative now, better ahead. For several years, the global growth in SUV sales has more than offset the impact of rapidly growing electric vehicle (EV) sales and general efficiencies of the global light vehicle fleet. EVs in 2020 grew 50% to 3 million vehicles from 2019 despite the decline in overall auto sales and then more than doubled in 2021 to 6.6 million. Despite this EV growth, however, SUV sales also hit a new record in 2021 more than offsetting the emission ‘savings’ of the EV growth. With the e-SUV percent of new SUV sales increasing, there should be a lessening negative over the next few years.

- China an issue but an evolving one. China as a country emits the largest amount of CO2 in the world at a rate about 2.5x the US in total. China also accounted for the majority of the growth in global emissions in 2020-2021. This growth was in part because China is a large country, because it experienced economic growth in both 2020 and 2021, and also because it has a significant amount of coal-fired generation. Chinese electricity demand grew 10% in 2021 and, despite a record amount of renewable energy supply, coal was called on to meet that growing power demand. Though China is making some large moves to change its energy mix, CO2 emissions should continue to rise with growth for a few years. That said, China’s emissions per GDP did decline slightly in a continuation of a multi-year trend, though remain higher than most industrialized countries on a per $GDP basis.

Looking Ahead

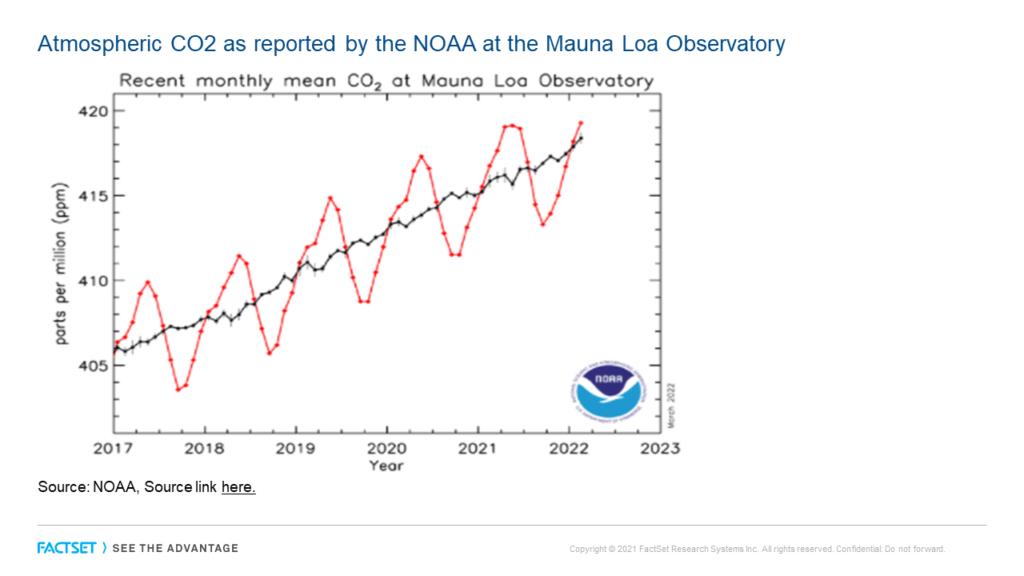

It is reasonable to expect emissions to rise again in 2022. In addition to the moving parts mentioned below, ongoing emission totals are lifted by both population growth and higher economic activity given our current energy systems. One can track CO2 in the atmosphere at the NOAA website.

Russian gas. The Russian invasion of Ukraine, by putting global natural gas markets in turmoil and lifting the price of that commodity, will leave coal at a favored cost position for many power generators. The result will be more coal burned for power generation in 2022. Many are suggesting that to avoid this situation – and to help enable reduced coal consumption in general – that the world needs more gas not less as we transition to more renewables. Assuming less Russian gas is supplied to the world for several years ahead would mean that natural gas supply will remain very tight and prices high continuing to motivate available generation capacity even if it is coal.

We are learning it’s not so simple. Higher gas and oil prices provide greater economic motivations for renewable power and EVs. That said, execution on renewables growth may be made more difficult by consumers because of economic pain and reduced cash flow after higher hydrocarbon prices. Renewable inputs, particularly metals, have also risen sharply in cost.

Experiences of the past year have highlighted that the transition path needs better management of the complexities, interactions, and need for global energy security. The IEA also hits on the need for consumption behavior changes, something that gets much less attention in the US and media or called out by climate hawks.

More climate efforts will be announced in the future. The IEA makes projections based on the worlds announced plans and finds that they are woefully inadequate to get us to a sustainable target. For example, by their estimation, we need to achieve a net reduction in energy consumption by 2050 compared to 2020 despite meaningful anticipated growth in economic activity given that renewables likely cannot grow fast enough nor can consumption patterns in buildings and industries adjust far enough.

In dollars, the IEA sees global planned spending on sustainable measures in the 2021-2023 period of around $400 billion per year. This level, however, is only 40% of what the IEA believes is needed to accomplish a trajectory to a net-zero 2050. We expect a continuing high level of new announcements on technology and mitigation capital spending – the IEA publishes on many available solutions – and these will impact forecasts in the future. Because spending will likely lag the IEA’s targeted levels, however, right now it looks like we still won’t meet the IEA’s more ambitious CO2 ceilings and hence not the 1.5 degree targeted limit either.