Rockies gas basis and flows could be on the precipice of a significant shakeup. Permian activity continues to heat up and large pipeline projects (i.e. Rover) connecting Northeast supply to the rest of the country are imminent.

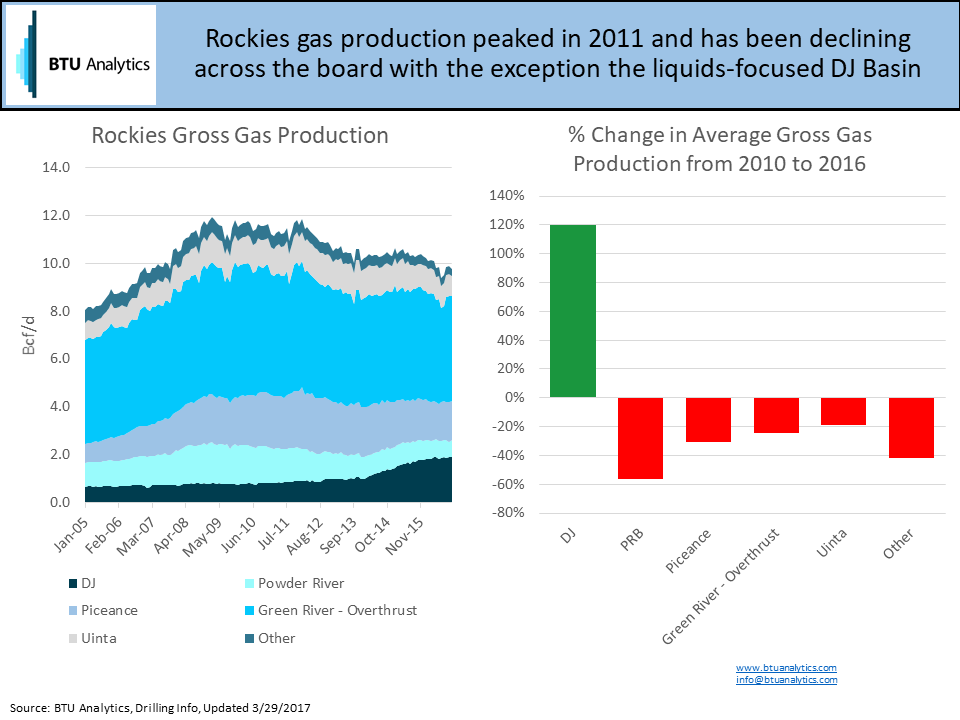

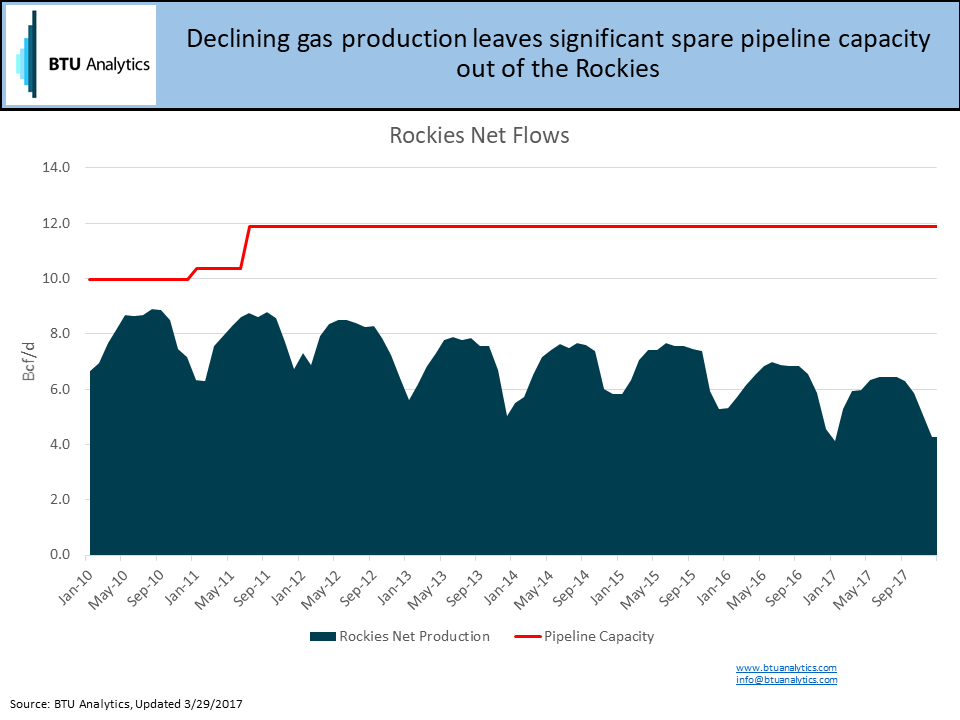

Between 2005 and 2008, Rockies gas production grew from 8 Bcf/d to almost 12 Bcf/d and rivaled other major natural gas plays of its time like the Barnett, the Granite Wash, and the Haynesville. Over this same period, average annual CIG basis was between -$1.37/MMbtu to -$2.42/MMbtu and Henry Hub’s annual average was between $6.72/MMbtu and $8.89/MMbtu. Strong Henry Hub prices, paired with wide Rockies differentials due to transportation constraints, incentivized the announcement and completion of three large greenfield projects, Rockies Express Pipeline (REX), Bison, and Ruby. However, natural gas prices had already started to decline in the summer of 2009 and have never recovered to the levels these projects were planned to support. REX was completed by Kinder Morgan in 2009 and provided relief for Rockies basis, but by the time Bison and Ruby were completed in the summer of 2011, production growth had stalled just below the 12 Bcf/d mark and has been in decline ever since, leaving significant spare capacity to a variety of downstream markets.

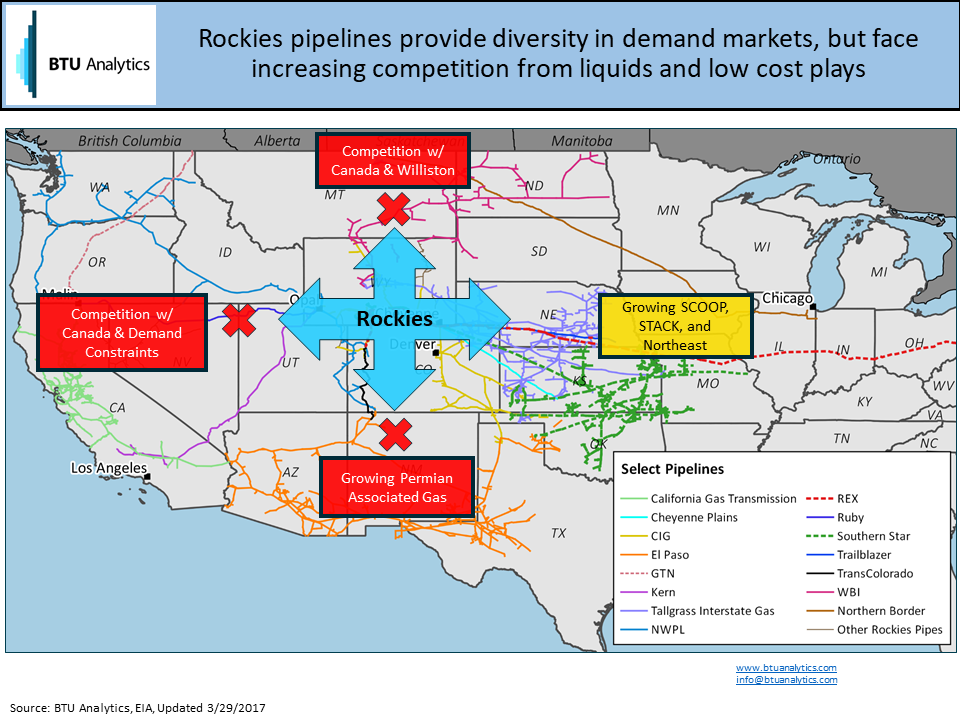

Currently, there are four main corridors out of the Rockies that allow natural gas to flow in all directions. On the surface, this seems like a significant benefit because it gives producers optionality to send gas to different markets based on premium pricing. However, in reality, shifting gas flow dynamics are increasingly boxing in Rockies gas.

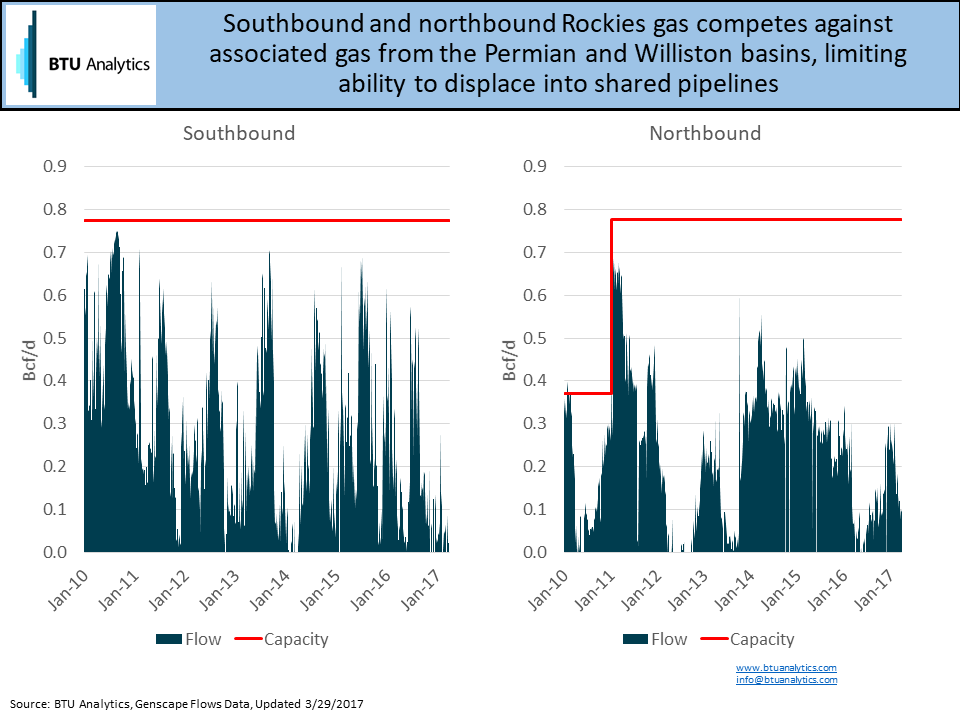

Starting with north- and southbound flows, these routes send Rockies gas into systems that also serve the Williston Basin and the Permian, respectively. Both plays are crude plays where oil economics rather than gas economics primarily drive activity, making producers in these plays largely insensitive to gas prices. Heading north out of the Rockies on Bison or WBI ultimately sends gas into the Northern Border pipeline which also serves the Williston Basin and Canada. Thus, flows north have been volatile and the volumes have been relatively small.

Looking to send volumes south, TransColorado and the southern leg of NWPL connect Rockies gas to the El Paso Pipeline system which is constrained due to limited California demand and extremely robust Permian growth. Additionally, the Permian Basin is an oil play with significant associated gas production. As a result, Rockies gas is competing against yet another play that produces gas as a byproduct and therefore can, and will, take large discounts to move gas as long as the oil economics remain attractive.

This leaves the routes west and east as the remaining options. The northern leg of NWPL, Ruby, and Kern are the three pipelines that connect the Rockies to the California and Pacific Northwest markets and have combined capacity of 4.85 Bcf/d. However, due to limited demand in California and competition against Canadian gas at Malin, OR, max daily flows since 2010 have never been above 4.5 Bcf/d.

From a capacity perspective, capacity east out of the Rockies is just under 5.5 Bcf/d between REX, CIG, Southern Star, Cheyenne Plains, Trailblazer, and Tallgrass Interstate Pipelines. Historically, much of the gas on these pipelines have been delivered to NNG, ANR-OK, NGPL-Amarillo, and PEPL to help serve Midwest demand which averaged 12.1 Bcf/d in 2016. Of the eastbound lines, REX reaches the farthest east with interconnects in Illinois, Indiana, and Ohio to PEPL, ANR-SEML, NGPL-Gulf Coast, Trunkline, Texas Gas, and as well as into Appalachia. Volume flowing east across all the lines out of the Rockies swings seasonally but has averaged nearly 2.9 Bcf/d over the last year with REX carrying about 1.2 Bcf/d of that volume.

While the Midwest market is a large demand center, new pipeline projects continue to grow the amount of low cost Appalachian gas that can access this market. Additionally, producers have increasingly been shifting capital to the SCOOP and STACK in Oklahoma which is expected to increase gas production in the area that will also compete with Rockies gas into the Midwest. That fact, combined with Canadian producers increasing firm capacity commitments on TransCanada, is providing a challenging outlook for Rockies natural gas basis. For deeper analysis on changing US gas market dynamics request a free sample of our Henry Hub Outlook report.