Master Limited Partnerships (MLPs) have boomed in popularity over the past decade as investors looked for investments that produced yield and seemed like a relatively safe way to participate in the North American energy boom. However, the relative safety of these investments is now being questioned as the pain being felt in the E&P sector due to weak pricing is spilling over into the MLP space as well. While many investors are focused on exposure to commodity prices, acreage dedications versus volume commitments and growth prospects, it’s also worth thinking about another significant risk that hasn’t been explored as much – counter party risk.

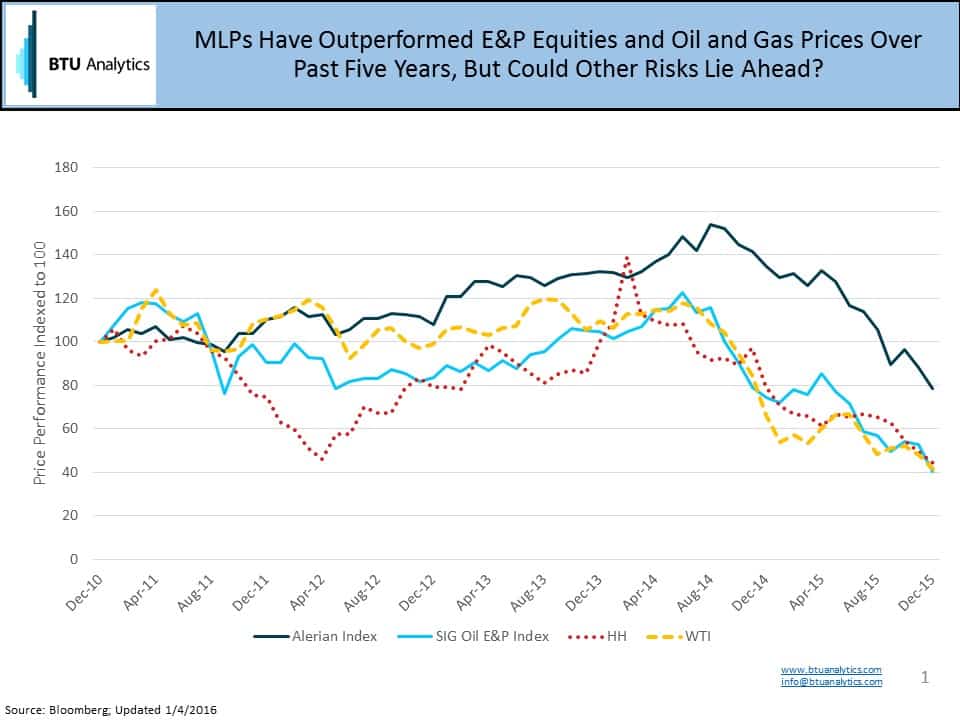

Before we go there, let’s look at how MLPs have performed versus E&Ps and commodity prices. The Alerian MLP Infrastructure Index: AMZI has outperformed E&Ps (represented by the SIG Oil Exploration & Production Index: EPX) as well as WTI and Henry Hub for the better part of the past five years. Major constituents of the AMZI include natural gas heavyweights Energy Transfer, Williams, ONEOK, Enbridge, Enlink, and Spectra Energy. The chart below shows that that MLPs were able to shrug off the gas price collapse in 2012 as the energy infrastructure boom shifted its focus to NGLs and crude oil.

However, as oil prices collapsed in 4Q 2014, and both oil and gas have remained weak through 2015, MLPs have, in some cases, been forced to start cutting distributions which has impacted their stock performance. But greater risks may lie ahead. MLPs can no longer say they are insulated from commodity prices due to take-or-pay contracts and firm commitments. Many pipeline projects announced and planned over the past few years have been backed by firm commitments from producers, and the risk of bankruptcy from counter parties looms as a very real threat to MLPs depending on contract structure.

In the Northeast, where over 20 Bcf/d of new pipeline projects are slated to be completed over the next few years, the majority of the new pipelines are backed by producers, and producers hold significant commitments on existing pipelines as well. If certain debt-laden Appalachian producers face bankruptcy, as Magnum Hunter did in December 2015, who might feel the midstream pain?

A cursory look at Northeast producers shows that the prolonged period of lower commodity prices are hurting some producers more than others. A simple chart that shows the ratio of Cash Flow from Operations to Total Interest Expense over the last twelve months for the most active producers in the Marcellus and Utica shows that for some, covering interest payments significantly impacts their ability to reinvest cash flow in drilling new wells. The chart below shows PDC Energy has the highest ratio at 9.5x (best) and Rex Energy has the lowest at less than 1x (worst). While this suggests that most producers do indeed have cash flow to cover interest payments on their debt, cash used to pay interest expense is cash that isn’t used in drilling programs to generate production to fill pipelines and meet contractual commitments made to MLPs.

Now, focusing on producers who are in the bottom third of the ratio analysis (ratio below 5x) and their existing and future commitments, Range, Antero, Rice, and Chesapeake have backed significant volumes on pipes like Texas Eastern (TETCO), Columbia Gas (TCO), Columbia Gulf (CGT), Tennessee Gas Pipeline (TGP), and Rockies Express (REX) historically. For example, Rice alone has 0.5 Bcf/d of commitments on TETCO and Range has an additional 1 Bcf/d of transport on TETCO as well (TETCO is a key asset of the Spectra Energy Partners MLP). Turning to future expansion projects, the expansion projects on these same pipelines are primarily backed by producers. Antero has almost 0.8 Bcf/d of commitments on TGP (roughly 25% of new capacity). TETCO has 0.5 Bcf/d of commitments from Chesapeake, which is almost one third of the new expansion capacity (some of this capacity may have been transferred to Southwestern in its acquisition of of Chesapeake’s acreage in the Southwest PA). This is compared to pipes like Dominion and Algonquin expansion projects which are largely back by LDCs.

So while many pipeline projects have take-or-pay contracts on their pipelines, which should limit downside risk from lower utilization rates, if producers enter bankruptcy or are left struggling, both historical and future commitments and the associated revenue are at risk potentially. Pipelines that do not have a diversified historical and future customer base are at the most risk, potentially putting MLPs in the line of fire. Counter party risk is a hidden peril that increases MLP exposure to commodity prices, and the longer this period of lower commodity prices lasts, the greater the risk grows.

For more detailed views on opportunities and risks in the 2016 energy market landscape, attend BTU Analytics’ What Lies Ahead conference in Houston, TX on Thursday, February 4, 2016.

{kind=link}