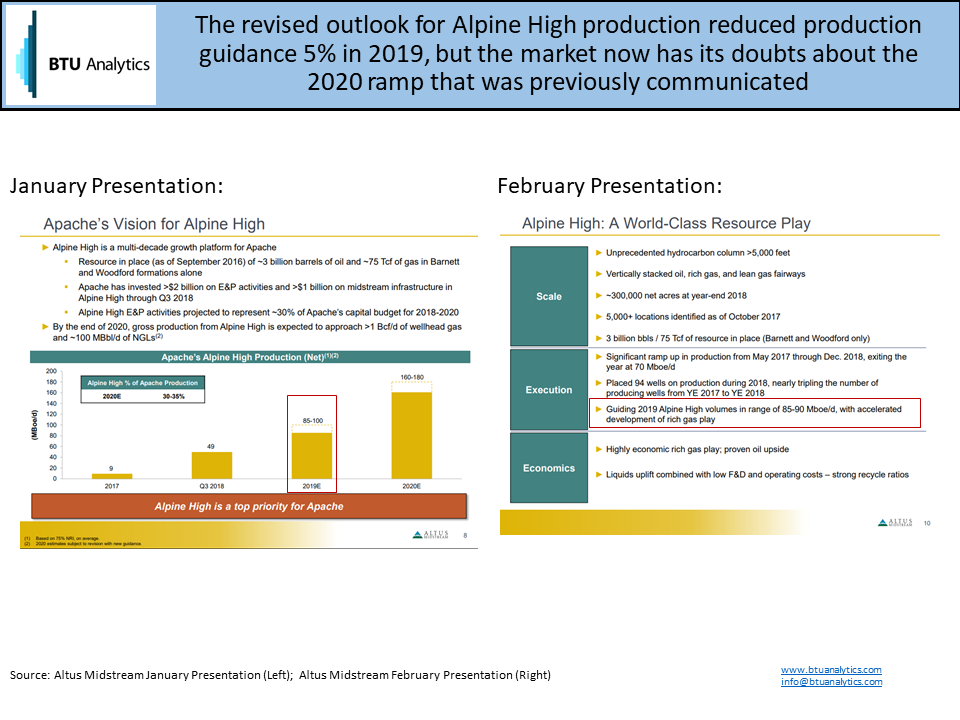

Last week, the market was caught off-guard when Apache (NYSE:APA) lowered the outlook for volume growth in the company’s Permian rich gas play, the Alpine High. Apache traded off just 1% following the disclosure, while Altus Midstream (NASDAQ: ALTM), the pure-play Permian Basin midstream company created to hold Apache’s Alpine High midstream assets, closed down 24%. The lower outlook came just three months after Apache had released a 2019 preview which featured a production guidance projection that had Alpine High production growing from 264 MMcfe/d in 2018 to 960-1,080 MMcfe/d by 2020. Apache management indicated during the company’s earnings call that the “world’s changed from where we were on the last earnings call and we’ve taken capex down, as you know, for 2019 and into 2020 and 2021.” It seems some in the market have had to learn the hard way that producer guidance is subject to change.

While Apache indicated that the company’s 2019 Alpine High production volume outlook is now 85-90 Mboe/d, down from the 85-100 Mboe/d announced in November, it’s the 2020 ramp that now appears to be in doubt. The graphic below compares slides from Altus Midstream both before and after the revised guidance from Apache.

The change in the Alpine High outlook doesn’t appear to be an immediate concern for Apache equity investors, as the company’s stock traded relatively flat following the announcement. However, the pace of development at Alpine High has significant implications for both Altus shareholders (APA owning 79%) and gassier producers in the Permian Basin.

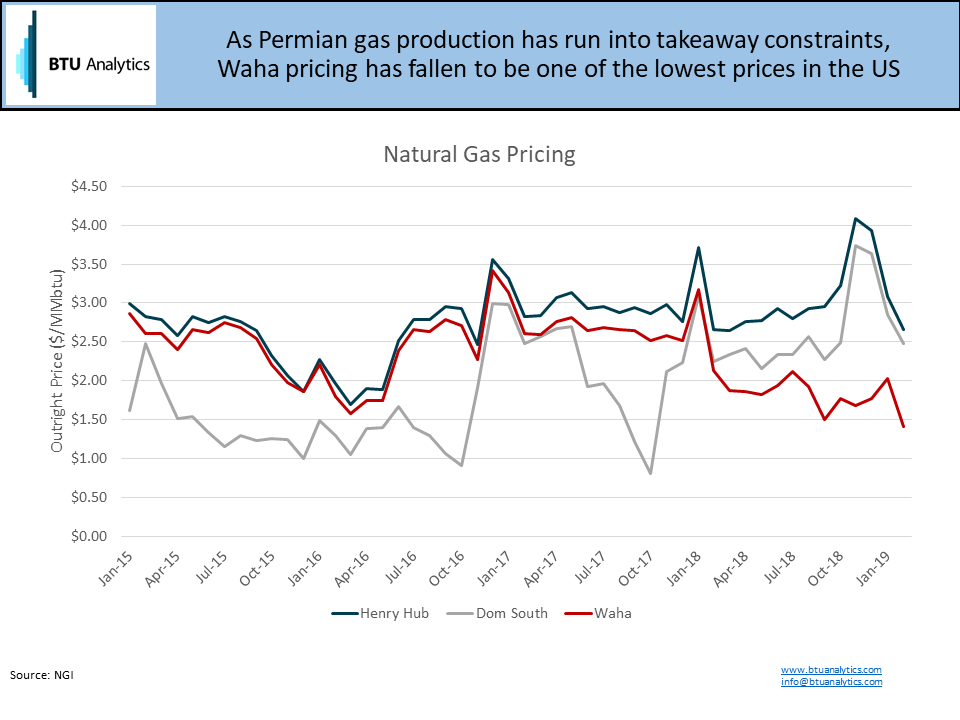

Dry gas from the Permian has grown from 5.5 Bcf/d in 2015 to approximately 10 Bcf/d today. BTU Analytics expects additional growth of 4 Bcf/d by the end of 2022, which will fill both Gulf Coast Express and Permian Highway, the first two greenfield projects to meet FID. Apache has contracted 1.05 Bcf/d, or over one quarter of the capacity on these first two pipes. Committing to gas transport to the Gulf Coast makes sense for Apache as the economics of the company’s Alpine High development is quite sensitive to natural gas prices and gas prices at Waha have been some of the lowest in the country. The chart below shows Waha natural gas price performance versus Henry Hub and Dominion South.

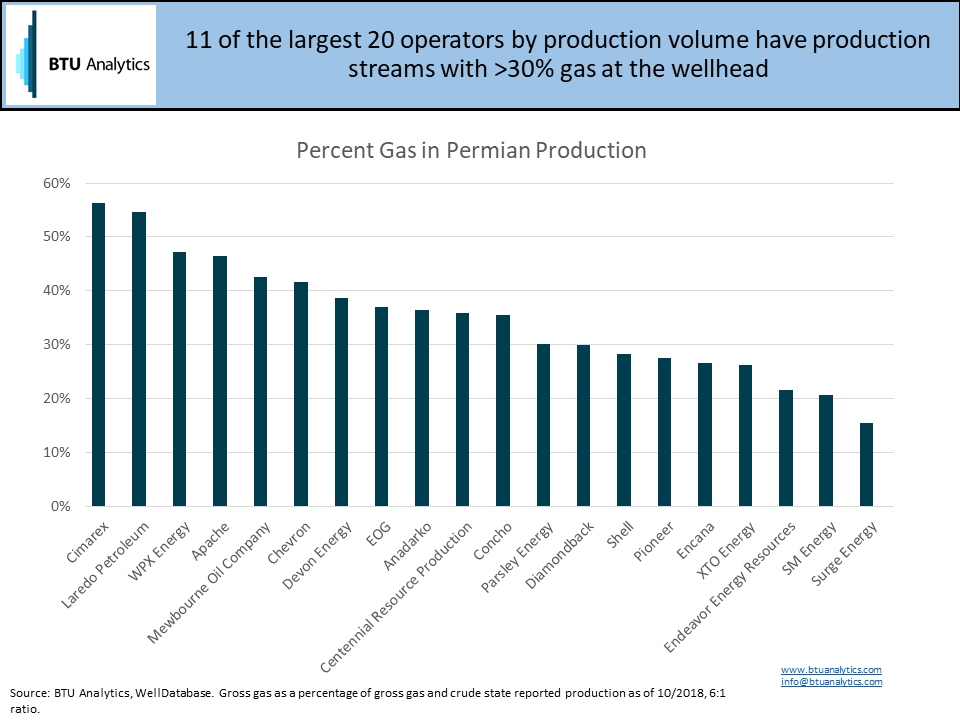

Who stands to gain or lose as the winds change on the outlook for the Alpine High? Gassier Permian producers should benefit from a slowdown in gas-focused development in the Alpine High. The lower outlook for gas production from Apache leaves more pipeline capacity available on new greenfield pipelines for other parties. Additionally, slower gas production growth should reduce the frequency and magnitude of Waha basis blowouts, improving price realizations for basin producers.

Unfortunately, the losers in slower Alpine High development are Altus Midstream shareholders and any end users who planned to benefit from (very) cheap Permian gas.

Where will Waha prices end up? How much Permian gas will end up in Gulf Coast and Mexico? Will Alpine High actually reach Apache’s stated potential? For more details on these questions and more, request information on BTU Analytics’ gas market services including the newly launched Gas Basis Outlook.