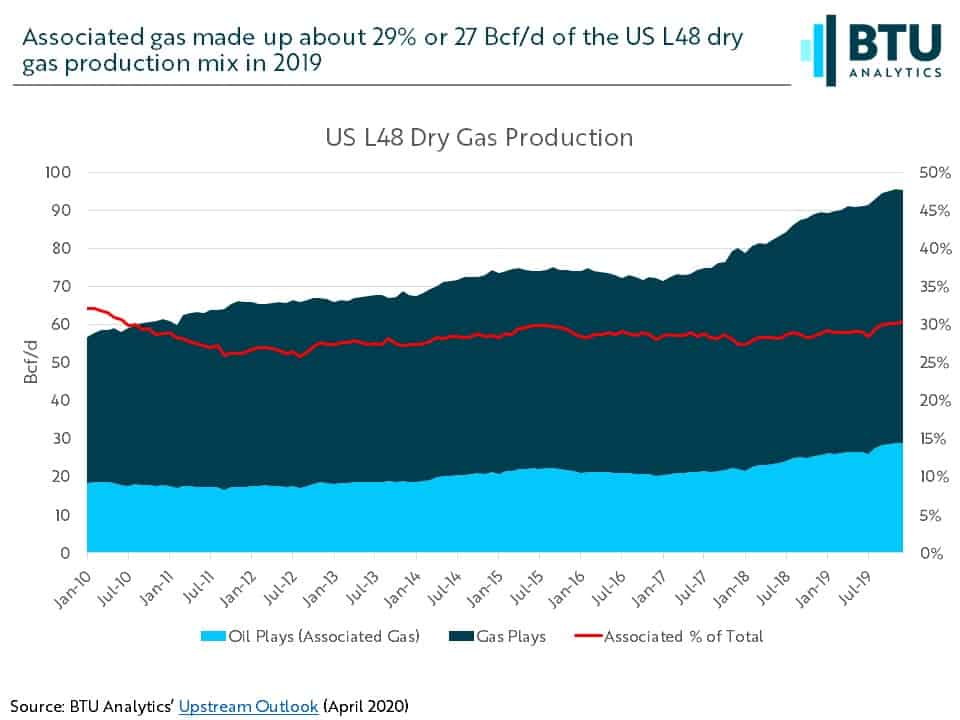

The impacts of COVID-19 on global oil demand are already tangible as many countries instituted shelter-in-place orders to slow the pandemic’s spread. Global liquids demand plummeted from pre-COVID levels as transportation came to a screeching halt around the world. If the result of the economic disruption is an extended global recession or slow oil demand recovery, the impacts could be felt beyond the five-year forecast window, and disruption impacts would not be limited to liquids balances alone. In 2019, associated gas production from oil-focused plays made up about 29% or 27 Bcf/d of the US Lower 48 dry gas production mix. If oil prices and demand languish for longer than expected and lead to declining associated gas production, the question becomes what is the long-term gas price needed to support sustained activity in gas-directed plays like the Haynesville, Appalachia, Western Rockies, Barnett or Fayetteville? Is there enough inventory remaining in these plays to support Wave 2 LNG? Or could oil prices rebound and bring associated gas production rushing back into the mix for gas prices?

Under a sustained weak oil price scenario, removing associated gas from the US Lower 48 supply stack could fundamentally alter the call on gas-directed production to replace lost associated gas production. While significant low-cost inventory remains in Appalachia, infrastructure constraints influence where and how much Appalachia can contribute. Additionally, low cost inventory is not infinite, and Appalachia has seen significant development for over a decade now. As such, looking at the potential outcomes for the impact of COVID-19 on long-term oil and gas prices could lead to significant low cost inventory depletion and require activity to return to gas plays that may have fallen out of favor with the rise of the Marcellus and rebirth of the Haynesville.

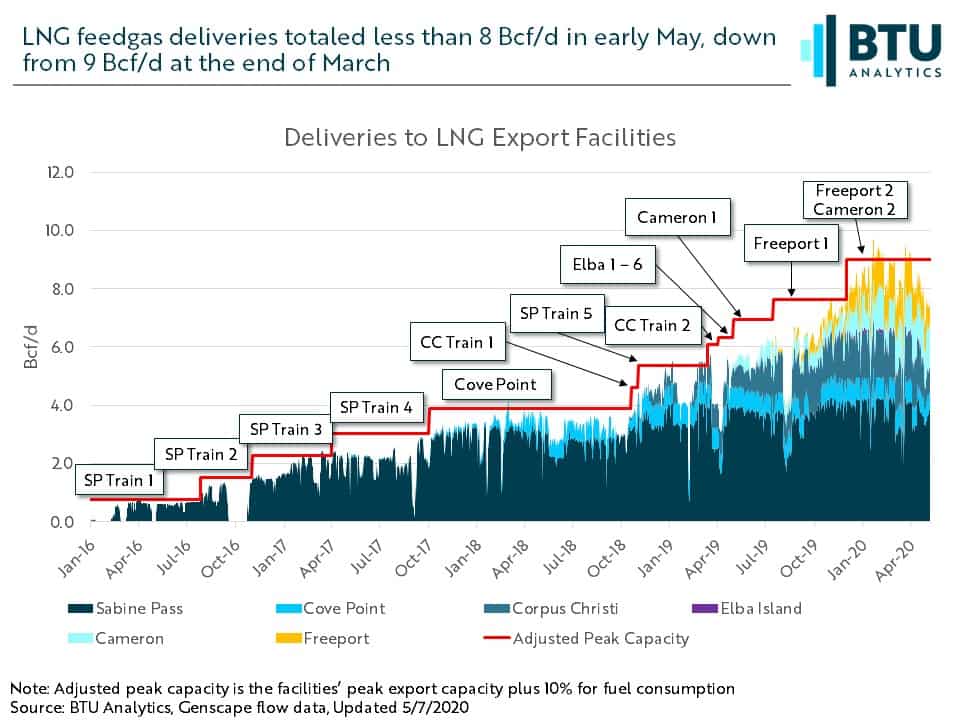

A second scenario is that an extended global recession has long-term impacts on both oil and gas prices. BTU Analytics recently compared today’s domestic natural gas demand to the 2008 recession and examined how 2020 might play out differently. One key departure from the 2008 demand mix is the addition of LNG exports. US LNG exports comprised about 9 Bcf/d of gas demand in March 2020. Utilization of US LNG facilities has historically run quite high, as shown below, but feedgas deliveries have already declined by over 10% in the last month. This calls into question not only near-term gas demand, but also the ability to make FID on LNG projects driving long-term demand.

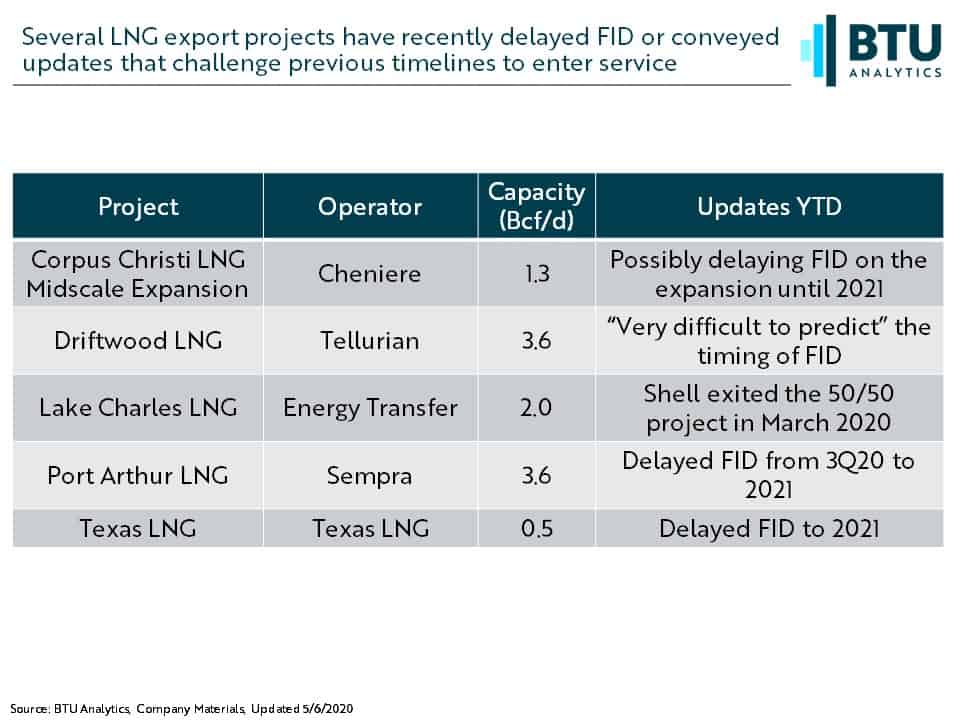

Unsurprisingly, several Wave 2 LNG export facilities have provided updates recently, summarized in the table below. These announcements highlight how difficult the current environment is for making FID on projects. Of the 37 Bcf/d of proposed Wave 2 LNG facilities, 11 Bcf/d has already announced delayed FIDs or even seen partners exit the project.

As the world begins the transition back to pre-lockdown status and allows travel to resume, there will be more questions raised about the timing and magnitude of oil and gas demand impacts over the long-term. If demand for either oil or gas fails to recover in 2020-2021, the impacts to natural gas pricing will propagate throughout the next several years, potentially exceeding BTU Analytics’ five-year forecast timeframe. For extended forecasts through 2050 for natural gas pricing and fundamental drivers, request information about BTU Analytics’ Long-Term Gas Outlook, which publishes on May 15, 2020.