The first round of lockdown measures to slow the spread of COVID-19 impacted industrial demand and LNG exports more than other sectors of US natural gas demand. With second wave lockdown measures expanding, it is time to examine any warning signals for impending natural gas demand destruction. Today’s Energy Market Insight will compare the magnitude of demand destruction from earlier lockdown measures on US industrial demand to a potential sequel lockdown wave.

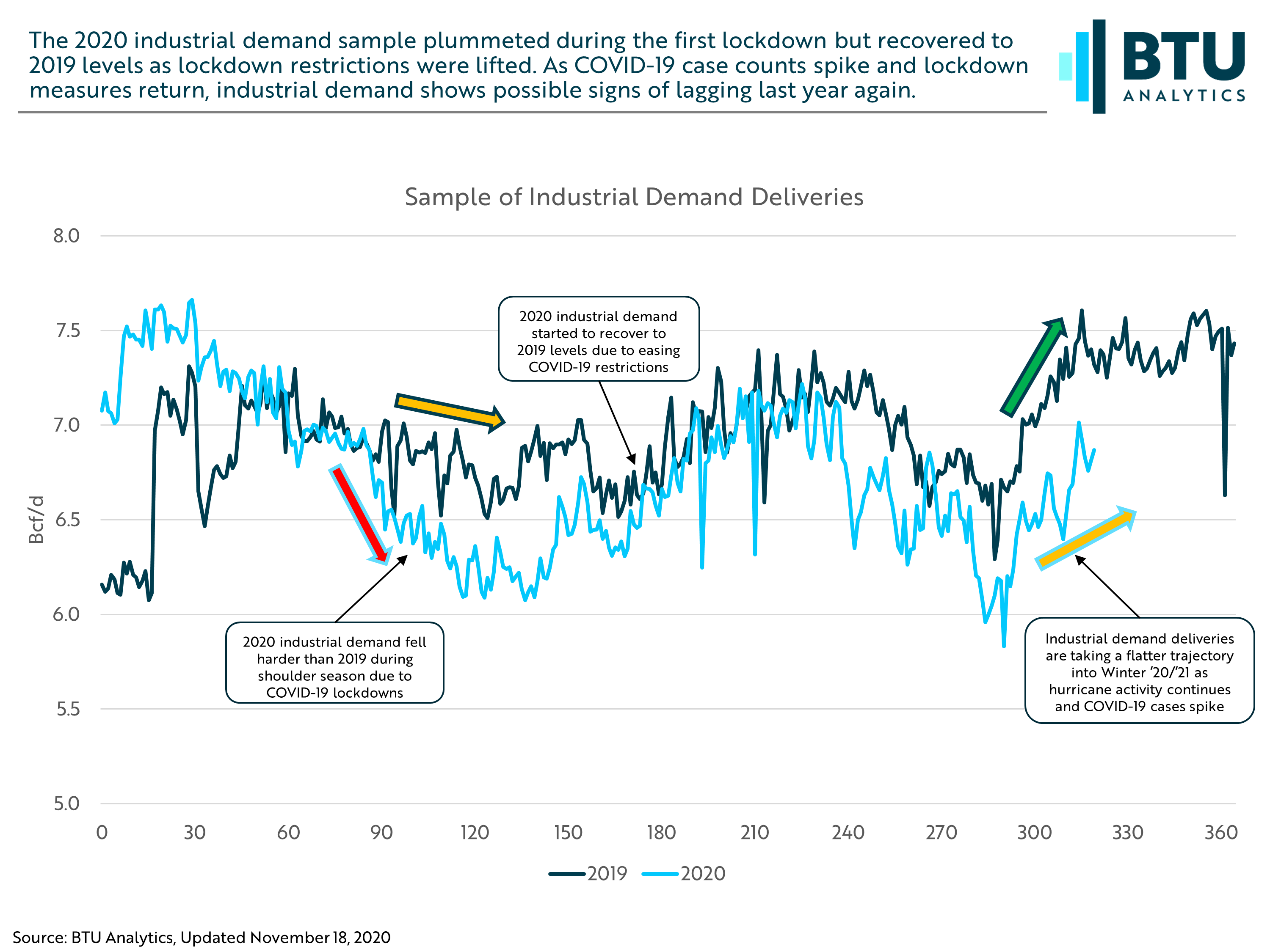

BTU Analytics discussed the early-stage impacts of lockdown measures on industrial demand back in May 2020. In May, a sharper than normal drop in the delivery sample on interstate natural gas pipelines indicated industrial demand was dropping. At the time, ethanol and methanol facilities were impacted by the lockdown-driven drop in motor gasoline demand. As travel restrictions eased over the summer, L48 industrial deliveries nearly recovered to 2019 levels. This industrial demand recovery faltered in late summer and early fall. An active hurricane season combined with increasing rates of COVID-19 transmission have disrupted demand again. With another round of measures to slow COVID-19’s spread pending in several US cities and states, it is possible the industrial sample’s slower seasonal ramping this fall could be driven by more than just an abnormally active hurricane season.

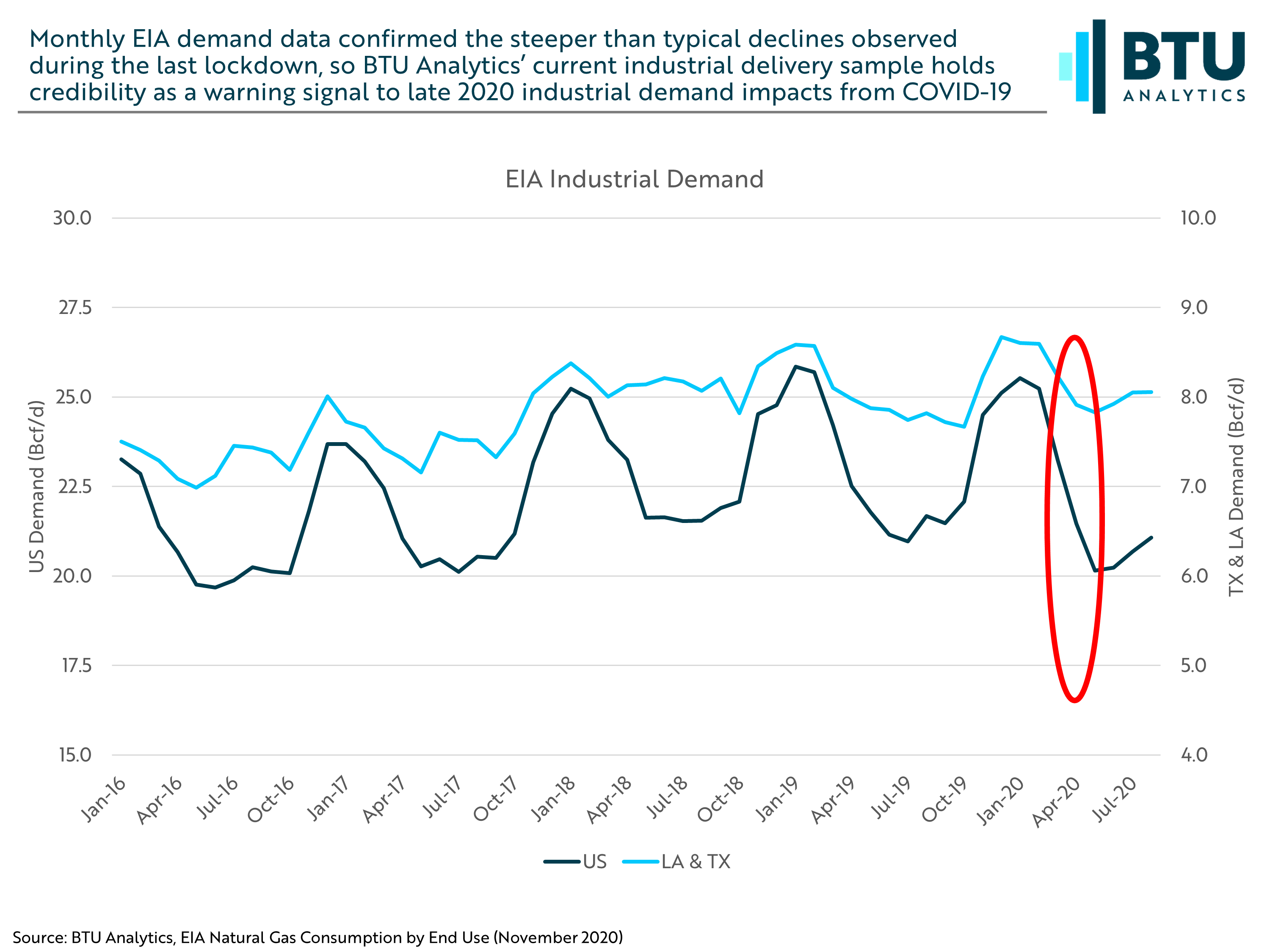

As BTU Analytics highlighted in our May 2020 industrial demand analysis, the abnormally fast drop in the spring sample was suspected to be overstated due to ethanol and methanol facilities’ robust connectivity with interstate pipes visible in the sample. Ethanol and methanol facilities show seasonal deliveries linked to refining throughput, which made the timing of initial lockdowns difficult to parse out from normal seasonal delivery declines. Industrial demand reported by the EIA eventually showed US industrial demand fell by 15% between February and April in 2020 compared to 12% in 2019. The deviation from 2019’s industrial demand seasonality was echoed in the Gulf Coast region, which is rife with refining and petrochemical facilities.

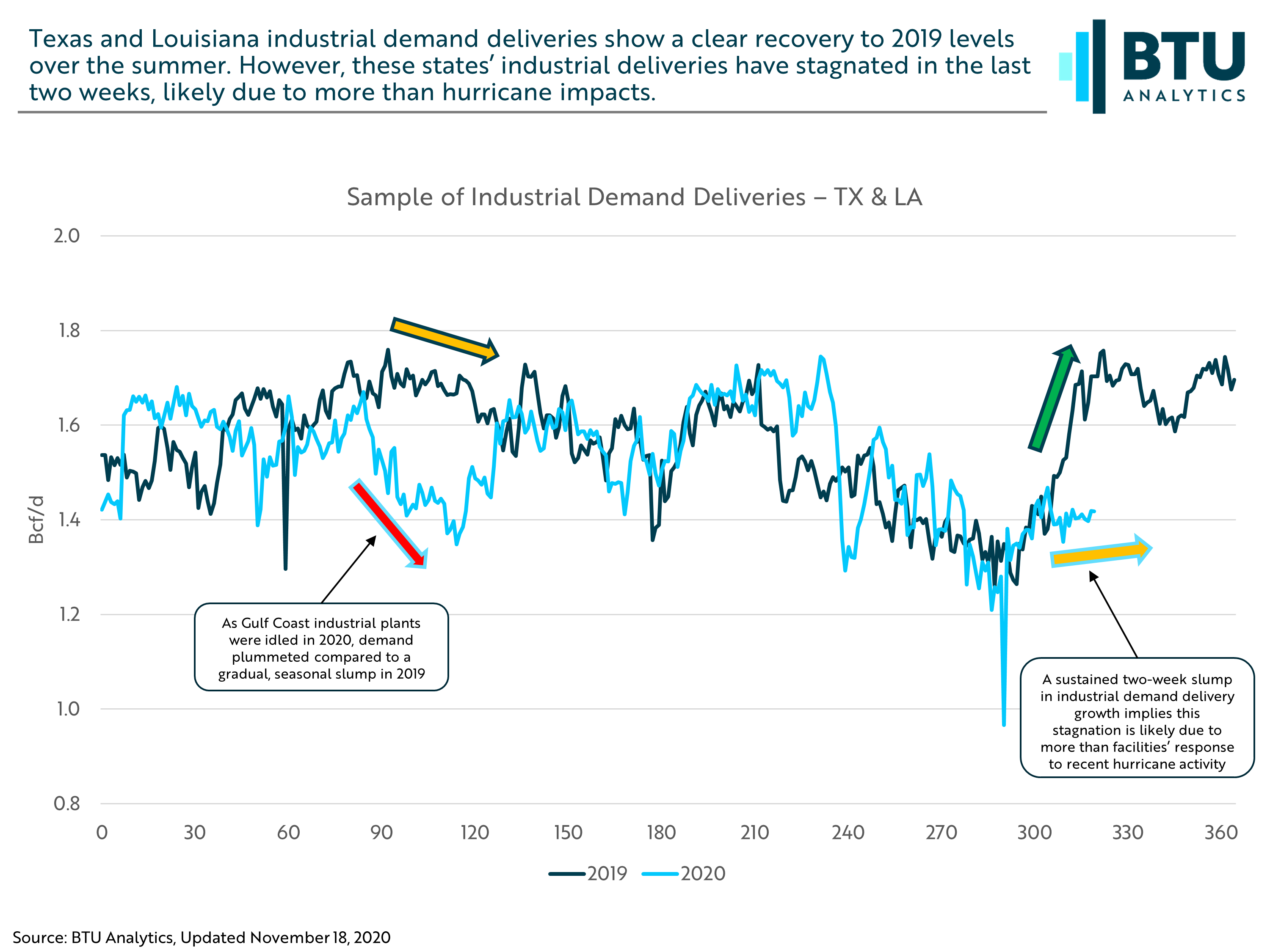

The Texas and Louisiana industrial demand sample accounted for an average of 23% of the L48 sample in 2019, making it a focal point for observing emerging trends in industrial gas demand. Like the L48 sample, the faster drop in deliveries in spring 2020 versus 2019 flows shows lockdown measures’ impact to the petrochemical-centric region. The Texas and Louisiana industrial demand sample dropped by 9% between average levels in March and April 2020, compared to a 2% growth over the same period in 2019. Industrial demand usually begins to climb as the winter months approach due to heating load and winter-blend gasoline production ramping up after refineries’ seasonal turnarounds. Deliveries to Texas and Louisiana industrial demand centers have remained flat in November 2020 despite LNG feedgas deliveries cresting 10 Bcf/d. This could mean that damage from recent hurricanes was highly discriminatory between petrochemical and LNG export facilities along the Gulf Coast, rising COVID-19 cases are beginning to slow domestic industrial activities, or some combination of the two.

BTU Analytics has revised its industrial demand forecast downward for the remainder of 2020, but how much of the recent stagnating momentum will carry forward into 2021? Our Henry Hub Outlook, which publishes today, addresses revisions to industrial demand and LNG exports. Changes to these sources of demand could drive changes to the end of season gas storage outlook if a mild winter fails to drive natural gas demand.