Historically, most US natural gas exports to Mexico have been exported through Texas, with smaller percentages delivered by Arizona and California. From January 2020 to May 2022, natural gas exports from Texas grew 3.5%, while Arizona’s and California’s dropped 0.8% and 2.7%, respectively. So far, in 2022, Texas has been responsible for over 91% of natural gas exports to Mexico, followed by Arizona at 6%, and California at 3%. Today’s Energy Market Insight will take a closer look at how the development of infrastructure in Mexico is affecting the flow of natural gas from Texas into Mexico, both now and in the future.

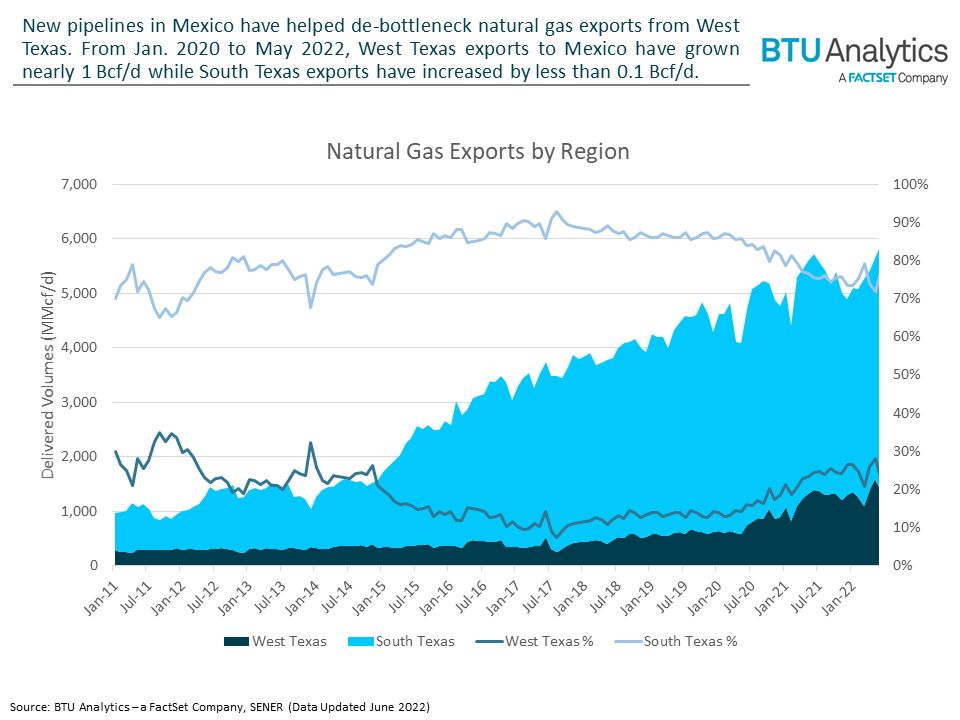

In January 2020, South Texas was responsible for nearly 86% of total natural gas exports from Texas, with West Texas exporting the remaining 14%. However, by 2022, the volume of natural gas exports from West Texas had increased by 0.95 Bcf/d, reaching a peak delivered volume of 1.6 Bcf/d in May, while South Texas exports increased by just 0.09 Bcf/d during the same period. This rapid rise in West Texas volumes has coincided with new pipelines coming online in Western Mexico, helping Permian supply reach new demand markets that were previously inaccessible.

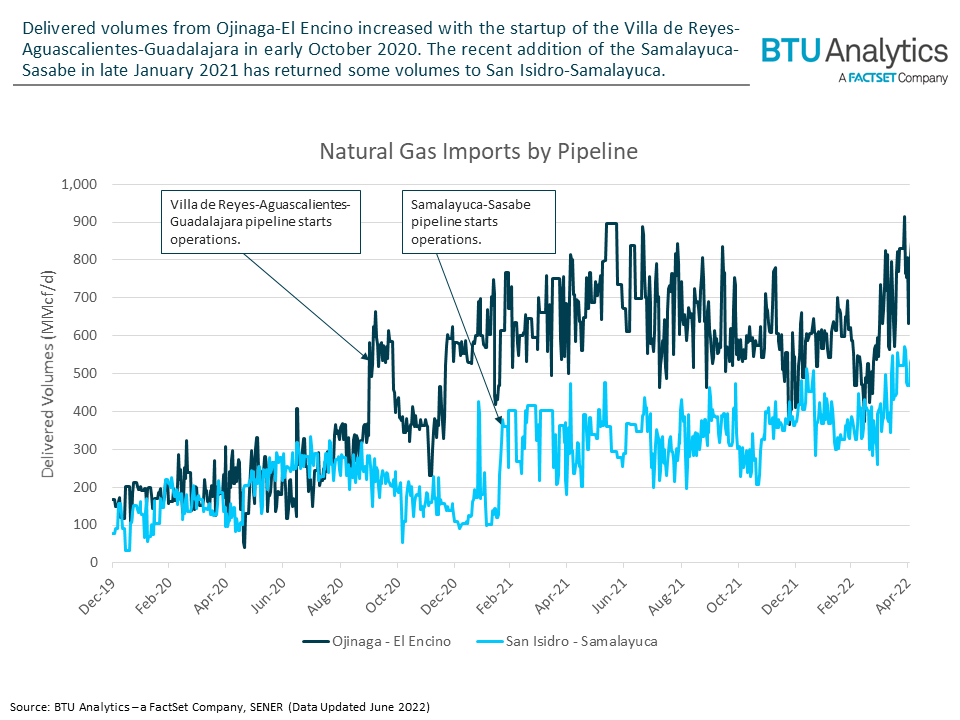

Over the past two years, the increase in natural gas flows from two Mexican pipelines, Ojinaga–El Encino and San Isidro-Samalayuca, have driven most of the increase in exports out of West Texas. In May 2022, Ojinaga-El Encino accounted for 47% of total natural gas exports from West Texas, while San Isidro-Samalayuca accounted for 33%. From December 2019 to September 2020, the two pipelines had similar delivered volumes, however, in early October 2020, Ojinaga-El Encino’s volumes experienced a drastic increase that was caused by the start of operations of the Villa de Reyes–Aguascalientes–Guadalajara (VAG) pipeline.

VAG was the final leg of the Wahalajara system that now consists of five pipelines, including the Ojinaga-El Encino pipeline, and allows natural gas from the Permian Basin to reach Guadalajara’s industrial center. After VAG became operational, natural gas flow from the Ojinaga-El Encino was increasing more compared to that of San Isidro-Samalayuca until, in February 2021, the Samalayuca-Sasabe pipeline started operations. When Samalayuca-Sasabe started operating, it connected San Isidro-Samalayuca with existing pipeline infrastructure in the northwestern region of Mexico and added incremental demand, resulting in increased flow in San Isidro-Samalayuca.

The growth in natural gas flow from both Ojinaga–El Encino and San Isidro-Samalayuca has exceeded the growth in supply in the West Texas corridor, indicating that these pipelines are driving the increase in exports from West Texas and could potentially be displacing flow coming out of other pipelines from the same region.

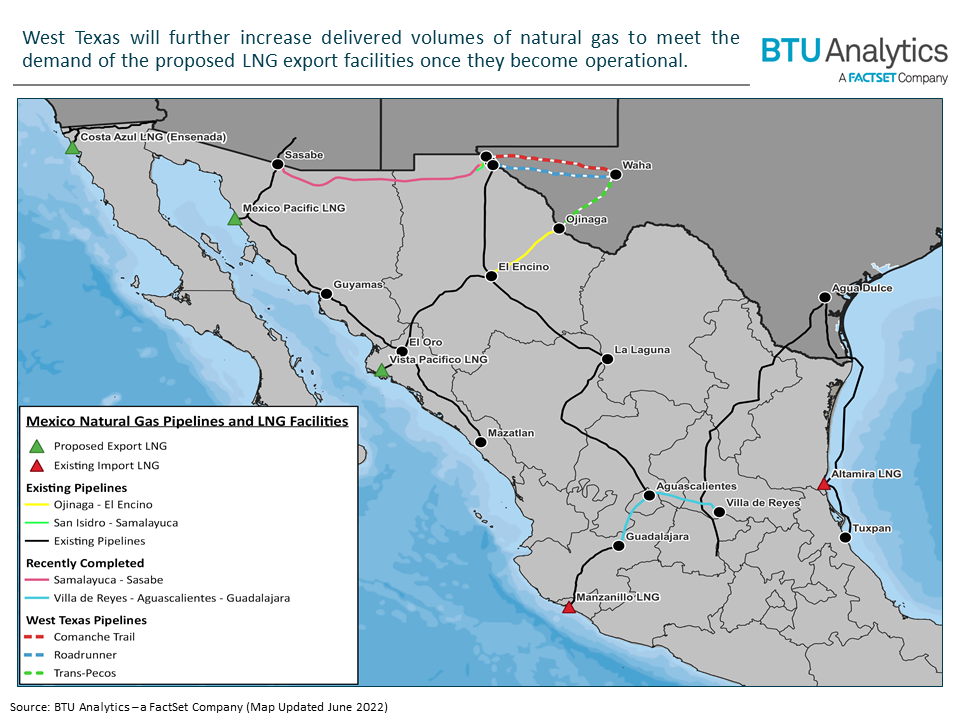

The increase in delivered volumes from the West Texas region is likely to continue in the coming years, as new LNG facilities start their operations in Mexico, including the Mexico Pacific Limited and Vista Pacifico LNG export facilities. If these two LNG facilities become operational in 2025, they will be connected to pipelines that source natural gas from the Waha hub in West Texas for export to the Asia-Pacific region. Given that the West Texas corridor is only using about 1.2 Bcf/d of cross border capacity out of the available 4.1 Bcf/d, there should be enough capacity to meet the total demand of 2.2 Bcf/d for the two proposed LNG export facilities.

Looking at historical and pipeline flow data across the US-Mexico border highlights the importance of understanding how recent changes to Mexican pipeline infrastructure have affected the dynamics of Texas exports to Mexico. It also reveals how West Texas will most likely continue to increase supply to Mexico to meet demand that is being created by the startup of LNG export facilities in the Western region of Mexico. With the continuous development of pipelines and LNG facilities in Mexico, Texas will continue to play a vital role in meeting Mexican demand for natural gas in the coming years. For more information on Mexican exports and their impacts on the US natural gas market, check out BTU Analytics’ Henry Hub Outlook.